After a tumultuous 2022, impacted by multiple negative developments culminating in the FTX debacle that sent the crypto space into further meltdown, 2023 has started with a bang for the industry.

As ever, leading the charge, bitcoin has put in an excellent rally, up by 38% since the turn of the year. And as is customary, other tokens have mimicked BTC’s behavior and have surged ahead too. Of course, the rally has also bled over to the stock market, with crypto-focused stocks benefiting from the shift in sentiment.

In fact, Josh Siegler, the crypto specialist at Cantor, expects the shares of a couple of BTC miners to deliver further upside over the coming months – in the order of 60% or more.

We ran these tickers through the TipRanks database to see what the rest of the Street makes of Siegler’s choices. As it turns out, Siegler is not the only one taking the bullish view here; both boast Strong Buy consensus ratings from the rest of the Street. Let’s take a closer look.

Riot Platforms, Inc. (RIOT)

Cantor’s first crypto pick is Riot Platforms, one of North America’s largest cryptocurrency mining firms. The company is focused on broadening its operations via increasing its bitcoin mining hash rate and increasing its infrastructure capacity.

The company had only 3.1 EH/s self-mining capacity at the end of 2021 but that has seriously accelerated over the past months, and Riot saw out 2022 with 9.7 EH/s, boosted by the deployment of recent miner purchases that brought its total deployed fleet to 88,556 miners. With further expansion, the company is targeting a hash rate of 12.5 EH/s by the end of Q1 as the Rockdale, Texas, facility adds a new building and the company installs more miners. Riot is also in the process of putting together 200 MW of immersion-cooling infrastructure. Additionally, the company hosts approximately 200 MW of institutional Bitcoin mining clients. Riot recently went through a rebranding, changing its name from Riot Blockchain to Riot Platforms.

In addition to quarterly results, the company provides monthly updates of its operations. The latest, for December, showed Riot mined 659 BTC, amounting to a 55% uptick compared to December 2021. The company sold 600 BTC, netting roughly $10.2 million.

Riot shares got absolutely decimated last year, but have rallied by 88% since the December lows. That said, Cantor’s Josh Siegler thinks they have more room to run.

Making RIOT his “Crypto Top Pick,” Siegler lays out the bull case. He writes, “With scale being paramount in this industry, we are positive on RIOT’s ability to mine more Bitcoin than others and reinvest those proceeds to further increase scale. Gross margin remains best-in-class at ~65%, largely due to unique energy agreements it has entered into… Unlike other miners, RIOT does not need to raise additional debt or equity to achieve its guidance.”

Siegler doesn’t just write up an optimistic outlook; he backs it with an Overweight (i.e., Buy) rating on RIOT shares and a $12 price target that implies a one-year upside potential of 61% from current levels. (To watch Siegler’s track record, click here)

Overall, it’s clear that Wall Street agrees with Siegler on the forward prospects for RIOT. The stock’s 8 recent analyst reviews include 7 Buys and 1 Hold, for a Strong Buy consensus indicative of a bullish outlook. The shares are priced at $6.20 and their $10.06 average price target implies a 12-month upside of 62%. (See RIOT stock forecast)

CleanSpark, Inc. (CLSK)

The next Cantor-endorsed crypto stock is CleanSpark, another bitcoin miner. That wasn’t always the case with this company, however. CleanSpark was once just a provider of microgrid solutions and only kicked off its mining operations at the end of 2020. Since then, though, the mining activities have become the main concern, with the company now a fully-fledged bitcoin miner.

The company operates its own bitcoin mining facilities in Atlanta, Georgia and co-locates miners in Massena, NY. Although bitcoin mining is known to be extremely energy intensive, CleanSpark touts itself as a sustainable mining firm and mines mostly with renewable or low-carbon sources of energy. The company’s capital management policy involves selling a big chunk of the BTC mined, the proceeds of which go towards funding further growth. This has enabled CleanSpark to boost its hashrate from 2.1 EH/s in January 2022 to 6.2 EH/s, in December, even in the face of the industry’s difficulties.

Per the company’s recent update, its fleet of 63,700 latest-gen bitcoin miners mined 464 bitcoin in December, resulting in annual production of 4,621 – representing growth of more than 200%. The company sold 517 bitcoins in December at an average of ~$17,000/BTC, with the sales generating proceeds of ~$8.7 million.

At the same time, the company said it is reducing its CY23E hash rate outlook from 22.4 EH/s to 16.0 EH/s, due to delays in the infrastructure expansion at Lancium, where CleanSpark has signed an agreement to deploy some of its mining gear.

While the result will be less hash rate by the end of the year, Siegler views the development as a “clearing event” for the stock.

“A 16.0 EH/s target would still solidify CLSK as one of the largest, vertically-integrated, self-miners in the industry,” the analyst said. “However, we believe the company has better foresight and control over the development of its self-mining sites than the co-location infrastructure. Further, the company disclosed that its new hash rate guidance requires just ~95,000 rigs and ~$70MM of CapEx spending. Assuming rigs can be acquired at ~$15/TH, this would imply the new cost for reaching its target hash rate is ~ $212.5MM. This compares favorably to our current conservative assumption of ~$350MM and will likely result in less equity dilution.”

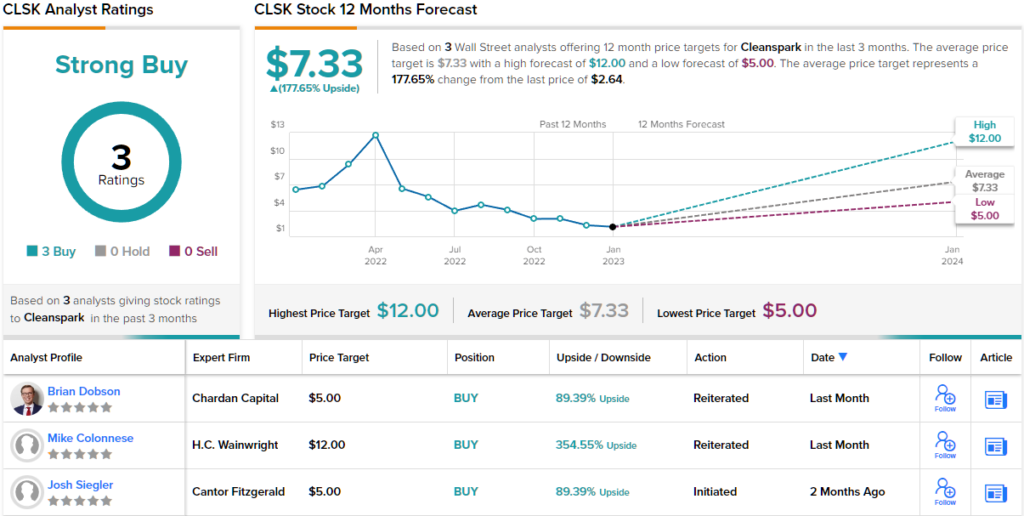

CleanSpark shares might be up by 48% since December’s trough, but Siegler thinks they have plenty more room to run. The analyst rates the stock an Overweight (i.e. Buy) along with a $5 price target. The figure makes room for one-year returns of 89%.

Two other analysts have recently waded in with CLSK reviews, and both are also positive, making the consensus view here a Strong Buy. At $7.33, the average target implies the shares will appreciate by a hefty 178% in the year ahead. (See CleanSpark stock forecast)

Subscribe today to the Smart Investor newsletter and never miss a Top Analyst Pick again.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.