The psychology of investing presents an interesting conundrum. When a stock soars, the natural tendency is to want to get in on the action, as the FOMO kicks in and the allure of further gains is hard to resist. This is often the wrong choice as the stock will likely be sold off at a premium to latecomers.

Conversely, a beaten-down stock induces tremors of fear. The inevitable concern about the stock’s low valuation and negative market sentiment can cause potential investors to avoid backing what appears to be a losing horse. This is sometimes the case, but other times share price weakness represents the best time to get in before a stock sets off on its upward trajectory.

So how can you tell the losers from the winners? While nothing is certain, the experts on Wall Street can lend a helping hand. In a recent note to clients, B. Riley FBR analyst Andrew D’Silva highlights stocks in the healthcare sector which he thinks are set to make headway in 2020.

“Each company either exited 2019 on a strong footing, where momentum is poised to carry over into 2020, or has fallen out of favor, but execution will result in a reversal,” the analyst commented.

Using TipRanks’ Stock Comparison tool, we were able to zoom in on 2 of D’Silva’s choices. Whether beaten-down or flying high, all have plenty of room for upside, and all currently have a Strong Buy consensus rating from the Street. Let’s take a closer look:

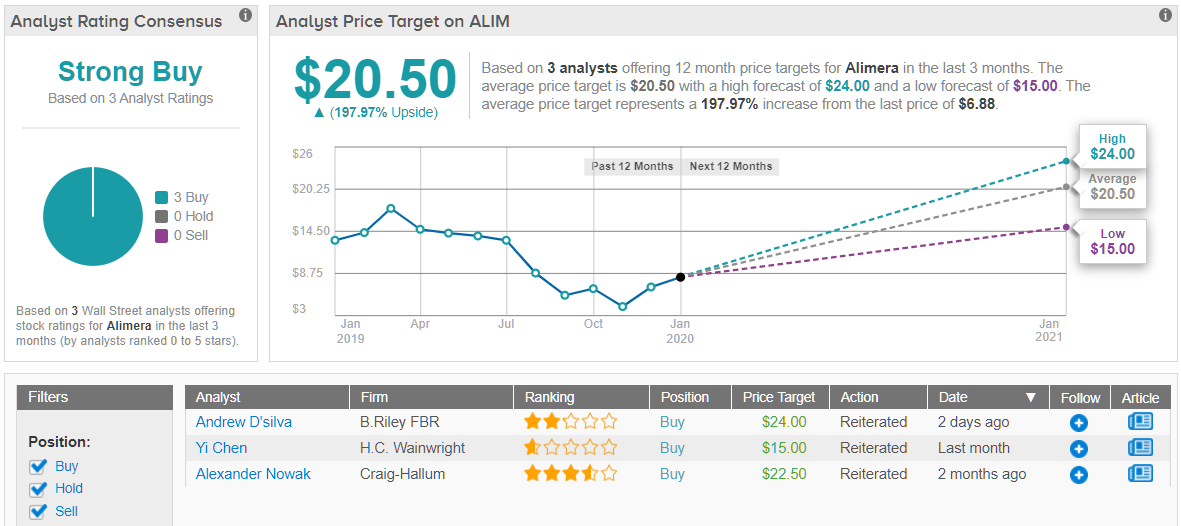

Alimera Sciences (ALIM)

Alimera Sciences had a miserable 2019. The retinal disease focused company lost 30% of its share price over the year. So far, 2020 has not been kinder, either. The share price is down by almost 10% year-to-date.

So, should investors stay away? Absolutely not, says D’Silva. Now is the time to reassess the biopharma’s potential.

The drop, he says, was instigated by the significant impact of 2Q19 results missing expectations, which were mostly attributed to a significant loss of domestic sales force. During 1H19, “several companies launched ophthalmic offerings and established/expanded their sales teams.” The numerous employment opportunities contributed to a depletion of Alimera’s own sales team.

“We believe this compounded investor working capital concerns, as ALIM’s $40 million term loan’s interest-only period was scheduled to end within a year’s time,” D’Silva noted.

However, the analyst expects a “significant reversal this year.” He cited a resolution to the company’s sales force turnover issues, an expanding international footprint, and the “significant milestone” of management’s positive 2020 adjusted EBITDA guidance as reasons for the anticipated turnaround. Furthermore, a new debt refinancing arrangement “cleared a significant working capital overhang.”

D’Silva noted, “While we expected that the company would refinance its term loan, we believe this should remove a significant trading overhang related to investor fears that ALIM would need to raise capital through a highly dilutive equity financing to fund operations and meet its debt obligation.”

D’Silva, therefore, reiterated a Buy rating on Alimera along with a price target of $24. With ALIM currently trading at $6.91, the upside potential comes in at a massive 243%. (To watch D’Silva’s track record, click here)

All in all, three analysts are currently keeping track of the eye disease specialist and all three see better days ahead too, rating the stock a Buy. With an average price target of $20.50, the figure suggests potential upside of nearly 200%. (See Alimera price targets and analyst ratings on TipRanks)

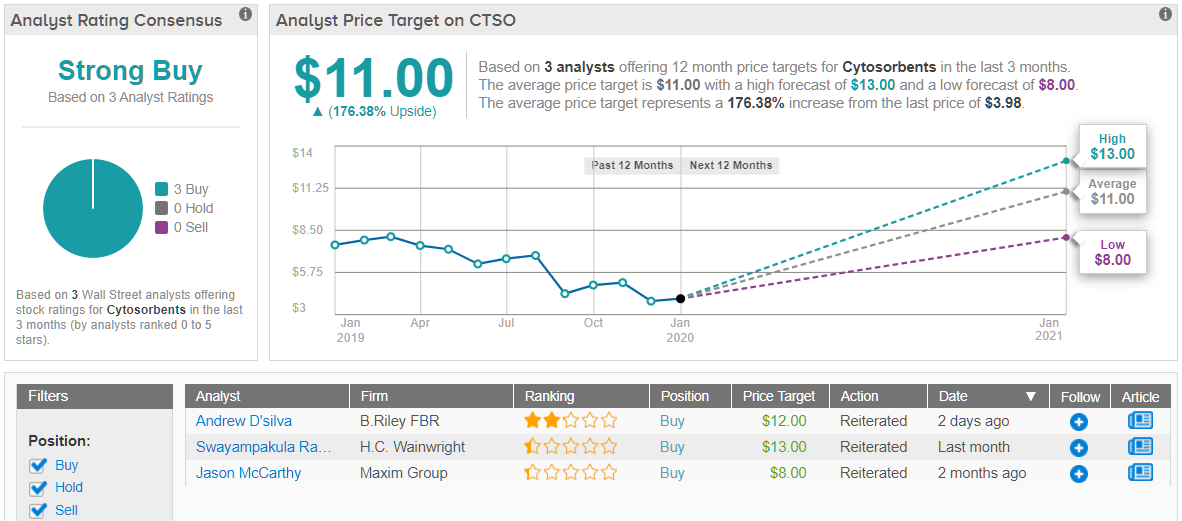

CytoSorbents Corporation (CTSO)

In a similar vein to Alimera, CytoSorbents is a beaten-down stock, displaying even further wreckage. It lost 52% of its share price during last year’s bull run.

CTSO’s blood purification technologies are used to control deadly inflammation in critically-ill and cardiac surgery patients. After exhibiting revenue growth of 51% in 2018, the growth curve slowed down to 9% year-over-year in the first three quarters of 2019.

D’Silva explained, “While the slower top-line growth could be concerning at first glance, the two primary reasons for the slowdown were related to two CS distributors and Fresenius Medical Care—which, together, accounted for ~15%-20% of the CTSO top line in 2018—entering 2019 with excess inventory, as well as CTSO running into sales-force bandwidth issues in its largest market, Germany.”

With CTSO commencing sales in Poland, Sweden, Denmark, Norway, and the Netherlands, D’Silva foresees a turnaround in the months ahead.

“While we don’t anticipate CTSO realized significant benefits from new direct sales regions in 4Q19, as most new sales hires were onboarded in 2H19, we do expect CTSO’s expanded footprint to provide a significant benefit this year… Meanwhile, We believe there are numerous clinical and regulatory catalysts are on the horizon that should be significant value drivers for the stock if successful,” said the analyst.

As a result, D’Silva kept his Buy rating and supports it with an ambitious $12 price target. Attaining this number will provide a very healthy 210% gain in the next twelve months.

Does the Street agree? Those who are taking notice certainly do. 3 Buy ratings and no Holds or Sells add up to a unanimous Strong Buy consensus rating. The recommendation comes alongside an average price target of $11 and implies upside potential of 176%. (See CytoSorbents stock-price forecast and analyst ratings)