Even for the fortunate ones not directly affected by the rapidly spreading coronavirus, try as you might, it is impossible to ignore the impact it is having on all facets of life across the globe right now; from the obvious and most pertinent health issues, to travel and across most industries, global supply chains and the world’s major economies have been negatively affected. The stock markets, of course, have been hit, too; Along with international markets tumbling over the past few days, all 3 major US indexes posted sharp losses this week.

The way the cookie crumbles, though, means that some will always be better positioned than others to cushion the blows. In what often feels like a macabre twist of fate, some companies actually stand to gain from the disruption, while others will lose share.

Taking this into account, 5-star Needham analyst Laura Martin recently assessed 2 names under the firm’s coverage on which the recent outbreak could, or is having a positive effect. After using TipRanks’ Stock Screener tool, we found out each boasts a substantial upside potential from the current share price. We’re talking more than 25% here. Let’s take a closer look.

Roku (ROKU)

Is Roku the new Amazon? Or maybe Netflix? These are the sort of questions that have been bandied about recently, following what can only be described as a market trouncing performance. The streaming player leader was one of 2019’s star performers, with its share price appreciating by almost 350% over the year. Roku stock, though, is currently trading at 30% less than last summer’s all-time high. Is now the right time to pull the trigger on the streaming stalwart?

It is, according to Martin. The 5-star analyst counts a number of reasons why she believes “Roku has the best strategic position in AVOD.”

Roku currently takes share of 45% of US streaming homes, which amounts to 37 million users. As the Roku Channel sells 100% of content it gets from nearly every AVOD app on its platform, it implies “Roku has better data than any single app.” Take this one step further, and as data points increase, ad targeting gets more finely tuned. “Any competitor with fewer or lower quality data points than Roku quickly falls behind making it nearly impossible to catch up with Roku over time,” Martin states. Secondly, Martin argues, integrated hardware (such as Roku TVs and sticks) and software (i.e., advertising revenue) “creates a stronger barrier to entry than just owning software (ie, an AVOD app) alone.”

Martin argues her bullish case for Roku could further be bolstered by, ironically, the coronavirus. The 5-star analyst states that should the virus spread any further in the US, folks will stay in, watch more TV and therefore, raise “the number of hours viewed and ad units available for Roku to sell above our current revenue and profit projections.”

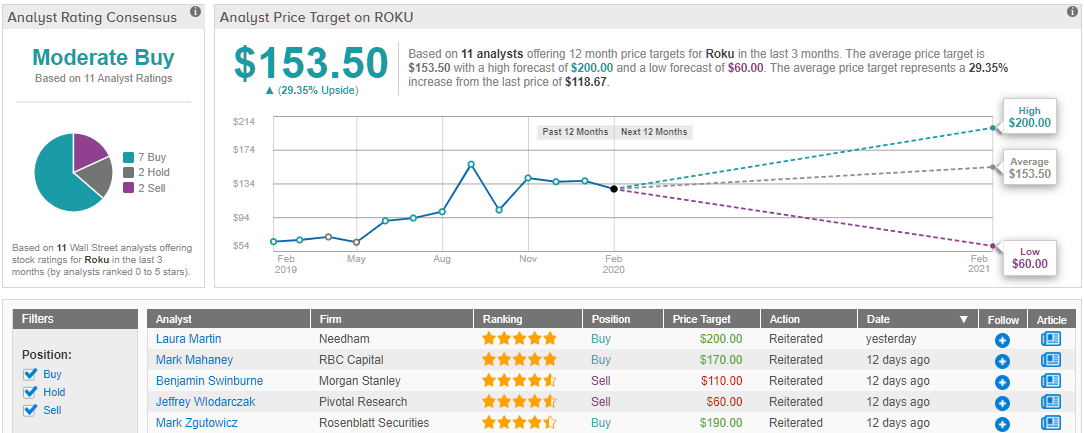

As a result, Martin reiterates a Buy rating on Roku stock along with her price target of $200. Should the target be met, possible gains of 68.5% could be in the cards. (To watch Martin’s track record, click here)

Looking at the consensus breakdown, Roku’s 7 Buys, 2 Holds and 2 Sells coalesce into a Moderate Buy consensus rating. At $153.5, the average price target could present possible upside of 29% over the next 12 months. (See Roku stock analysis on TipRanks)

Peloton Interactive (PTON)

Following a disastrous entry to the market last year, in which Peloton posted one of the worse trading debuts of the decade, the stationary bicycle company has been taking big strides forward. Despite a very healthy growth curve, though, at $27.11, Peloton stock is still trading below its IPO price of $29. According to Martin, though, this won’t be the case for long.

The company is growing in popularity as its latest earnings report can attest. Growth of 77% year-over-year and a 94% customer retention rate are impressive figures in anyone’s book. Total memberships have now hit 2 million accounts, while over the past year, the number of connected fitness subscribers paying monthly premiums has nearly doubled.

The case for Peloton using the coronavirus to its advantage is a simple one, according to Martin: “with new COVID-19 hotspots in South Korea, Italy and Iran, we believe certain US consumers will be less comfortable over time going to their gym and more likely to order a PTON bike to stay home. This may drive higher unit sales and subscription revenue in 2020 than are currently in our estimates.”

Martin argues her bullish thesis further by noting, “Each of PTON’s Active Accounts has about 2.8 users, so PTON screens will reach more than 2mm unique users each month by the end of FY20. PTON’s long engagement lengths drive low churn at under 1% per month, despite PTON’s new free Home Trial for 30 days. So far there have been minimal returns, which drives faster adoption and subscription revenue growth. We assume that hardware adoption continues to grow and that the digital SVOD service creates a low-risk onramp into the PTON ecosystem.”

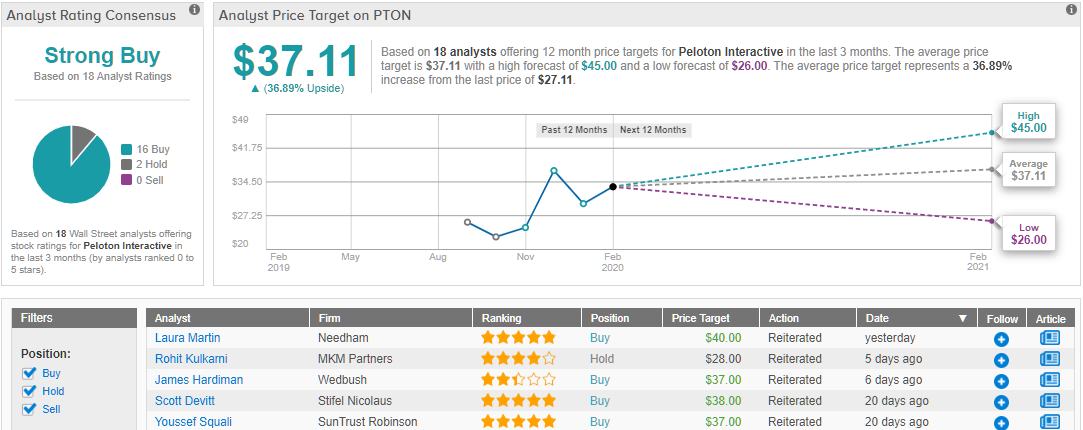

All the above means Martin keeps her Buy rating and $40 price target as is. The figure presents possible upside of 47.5%.

The Street pauses its workout and nods in agreement. PTON’s Strong Buy consensus rating breaks down into 16 Buys and 2 Holds. The average price target is $37.11 and implies an additional 37% could be added to the share price over the coming months. (See Peloton stock analysis on TipRanks)