In Kenny Rogers’ iconic song “The Gambler,” he sang, “Every hand’s a winner and every hand’s a loser…” These words hold valuable wisdom that every investor should remember. Regardless of your chosen strategy, successful stock investing ultimately boils down to mastering the art of balancing risk and reward.

There are few stock segments that offer a higher return potential for the risk involved than the penny stocks, those equities priced at $5 or less. These are stocks with a truly rock-bottom cost of entry.

The low cost of entry brings with it the potential for enormous gains, as even a small increase in the absolute share value can quickly translate into a high-percentage return. When it comes to penny stocks, it is not unheard of to find upside potentials of 200%, 300%, or even better. Of course, the flip-side is also true; with the high reward comes increased risk.

Given the nature of these investments, Wall Street analysts recommend doing some due diligence before pulling the trigger, noting that not all penny stocks are bound for greatness.

Taking this into account, we used TipRanks’ database to identify two penny stocks that have earned a “Strong Buy” consensus rating from the analyst community. There’s good reason for that approval – the analysts see upside potential here starting at 400%, giving investors a chance to quintuple their money. Let’s take a closer look.

Viracta Therapeutics (VIRX)

We’ll start with Viracta Therapeutics, a clinical-stage biopharma firm focused on developing new precision medicines for the treatment of cancer. Specifically, Viracta is working on drugs to treat cancers related to the Epstein-Barr virus. This is a common pathogen frequently found in humans, and it’s part of the herpes family of viruses. Estimates suggest that some 90% of the world’s population carries the EB virus, which has been linked to several forms of cancer, including lymphomas, gastric tumors, and nasopharyngeal cancer.

Following this path, Viracta has brought a promising drug candidate into the human trial clinic. This candidate, a proprietary investigational drug, is called nanatinostat and it is administered in conjunction with the anti-viral drug valganciclovir. The combined agent has been dubbed Nana-val, and it is currently undergoing several concurrent trial studies. The two leading studies are evaluating Nana-val as treatment for lymphomas and metastatic solid tumors.

Viracta’s Nana-val has been granted the FDA’s Fast Track designation in the treatment of relapsed and/or refractory EBV-positive lymphoid malignancies and has also been given Orphan Drug designation for the treatment of T-cell lymphoma, plasmablastic lymphoma, post-transplant lymphoproliferative disorder, and EBV-positive diffuse large B-cell lymphoma.

In its recent quarterly update, Viracta stated that its ongoing pivotal trial of Nana-val for the treatment of EBV-positive lymphoma is proceeding rapidly. An update on this trial, NAVAL-1, is expected in 2Q23, and the company anticipates advancing the trial from Stage 1 to Stage 2.

In addition, Viracta has also stated that it is enrolling patients into the fifth dose level of its Phase 1b/2 trial of Nana-val in the treatment of advanced Epstein-Barr positive solid tumors. This represents the dose escalation portion of the study, and data from this stage is expected in 2H23. Viracta also anticipates initiating the recommended Phase 2 dose (RP2D) expansion cohorts in various solid tumors during 2H23.

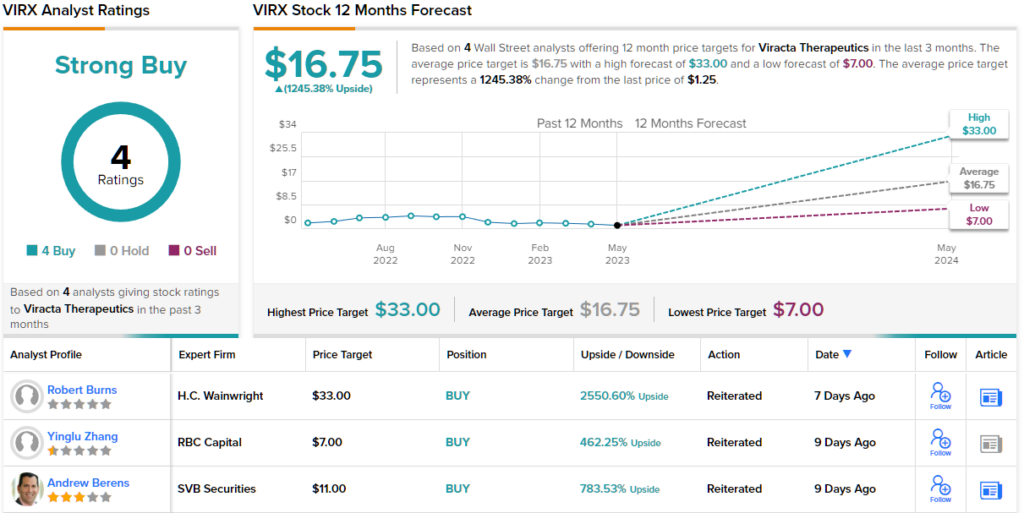

All of this has captured the attention of RBC analyst Yinglu Zhang, who gives an upbeat take on Viracta’s near-term prospects.

“With NAVAL-1 first subtype update regarding stage advancement upcoming in 2Q2023, we are encouraged by the consistent progress of the Nana-val programs and remain optimistic going into the update which could potentially drive upside. Solid tumors on track for RP2D selection, data updates, and expansion cohort initiation in 2H2023, to provide further de-risking and optionality, in our view… We continue to see 2023 as an appreciation opportunity for shares,” Zhang opined.

Zhang backs up his bullish stance with an Outperform (i.e. Buy) rating on VIRX stock, while his $7 price target suggests a robust 462% upside for the coming year. (To watch Zhang’s track record, click here)

The RBC view may turn out to be conservative when it comes to VIRX. The stock’s Strong Buy consensus rating is based on unanimous reviews from 4 analysts, and the average price target of $16.75 implies a sky-high upside potential of 1,245% from the current share price of $1.25. (See VIRX stock forecast)

Rani Therapeutics Holdings (RANI)

The next penny stock we’ll look at is Rani Therapeutics, a clinical-stage biopharmaceutical firm working on a potentially disruptive medical technology that will enable the oral delivery of biologic medications. Biologics are a class of medicines used to treat serious metabolic, autoimmune, and inflammatory conditions. However, they are typically broken down by the stomach, necessitating intravenous dosing. Rani Therapeutics has developed a robotic pill called the RaniPill, which can transport the drug through the stomach and into the small intestine. Once there, it injects the medication into the intestinal wall.

The company is testing its oral dosing method ‘in the clinic’ and currently has eight research tracks in various stages of preclinical and clinical testing. Five of these tracks are described as ‘core’ product candidate programs, and out of those, three deserve a closer look.

The most advanced of these is RT-102, a potential treatment for osteoporosis. Rani recently received feedback from the FDA regarding the company’s development plans for RT-102, including agency guidance on the Phase 2 clinical trial. Rani plans to initiate the Phase 2 trial of RT-102 during 2H23.

Also on the path to initiation is drug candidate RT-105. The company is planning a Phase 1 clinical trial of this candidate, described as an adalimumab biosimilar, for the treatment of psoriatic arthritis. The trial is planned to begin later this year.

Finally, Rani is gearing up to initiate a Phase 1 clinical trial of RT-111, a ustekinumab biosimilar drug under investigation for the treatment of psoriasis. Rani announced during Q1 that it has entered into a partnership with Celltrion, a South Korean biopharma, to develop RT-111. The drug candidate is optimized for use with the RaniPill capsule system, and Rani holds an exclusive license from Celltrion to develop the drug candidate in this application and to commercialize it post-clinical trials. In return, Celltrion will acquire worldwide rights to the drug after the Phase 1 trial, which is planned to begin this year.

BTIG analyst Julian Harrison, who holds a 5-star rating from TipRanks, covers Rani, and he is impressed with the large number of catalysts on deck for the next several months. Writing of the company and its pipeline, Harrison says, “We view the remainder of 2023 as largely being an execution year for Rani, with initiation of a Phase 2 trial of RT-102 in osteoporosis is expected in 2H23 along with Phase 1 initiations of RT-111, RT-105, and RT-110 expected later in the year. We recognize that upside could be realized through additional potential partnerships, following a highly validating deal with Celltrion for RT-111… We see billion dollar peak revenue potential for RT-102, RT-105, and RT-111, as well as lesser, but material potential for the other programs.”

Harrison backs up his bullish stance with a Buy rating on the stock, while his $24 price target suggests a strong upside potential of 488%. (To watch Harrison’s track record, click here)

Overall, all three of the recent analyst reviews on RANI are positive, making the stock’s Strong Buy consensus rating unanimous. The shares are trading for $4.08 and the average price target is $22, suggesting a one-year gain of 439%. (See RANI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.