Let’s talk about dividends. For investors interested in quick returns or steady income, these profit-sharing payments to stockholders have always been an inducement to enter equity markets. In today’s financial environment, with bond yields depressed and the Federal Reserve’s key interest rate set at just 1.75%, dividends are a natural place to look if you want to grow your money.

And why not? Even at the low end, dividends offer at least the same return as bonds – but with higher potential for increase. The average dividend yield among companies listed in the S&P 500 is just about 2%, meaning a significant number offer far better returns. We’ve opened up the Stock Screener tool from TipRanks, a company that tracks and measures the performance of analysts, to find a few of these high-yielding stocks.

Setting the screener filters to show us small to large-cap companies with a very high dividend yields exceeding 5% gave us a manageable list of stocks. We’ve picked three to focus on.

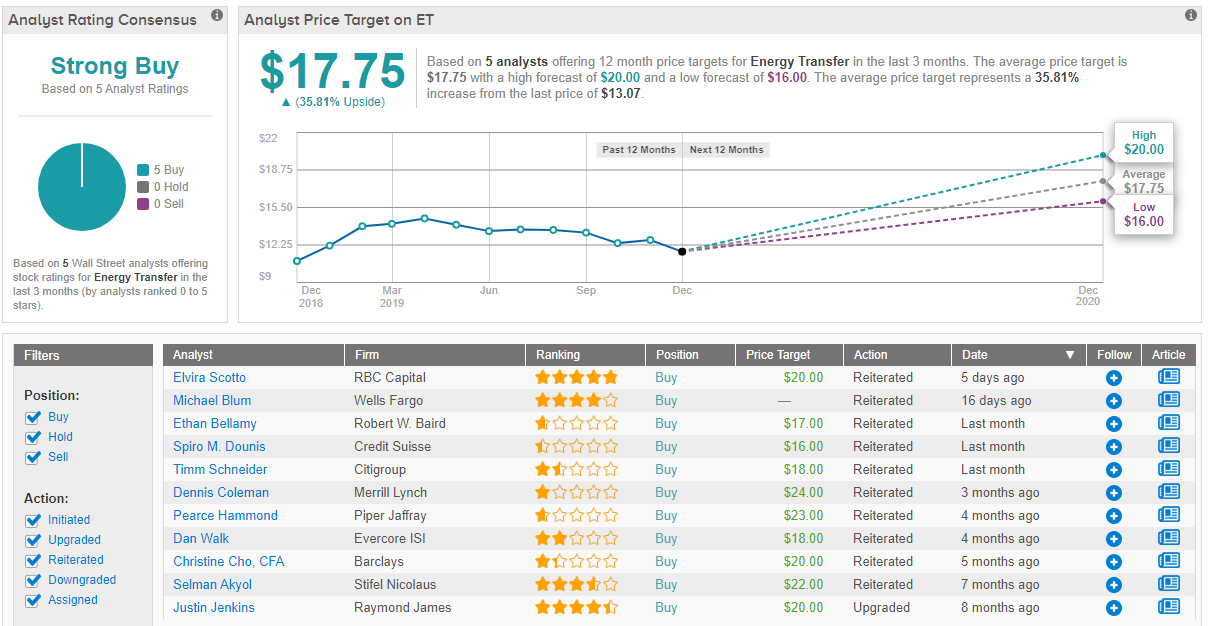

Energy Transfer LP (ET)

When you picture the oil and gas industry, the giant wellheads are probably the first thing that come to mind. But those are only a small part of the larger reality. Energy Transfer is midstream company – one of the many entities that works at moving the oil and gas products from the well to the users. Energy Transfer has operations in 38 states, with most of its assets in the Texas-Oklahoma-Louisiana and Midwest-Appalachia-Delaware regions.

Anything connected to the oil industry tends to drip money, and ET is no exception. The company saw $54 billion in total sales last year. The Q3 numbers show that it is on track for a similar performance this year. The most recently reported quarter showed $13.5 billion in revenue, with a 32-cent EPS based on net profits of $832 million. While revenues were short of the forecasts, EPS met the estimates.

ET’s earnings number is important as it shows that the company can easily meet its dividend obligation. Energy Transfer pays out $1.22 per year, or 30.5 cents quarterly, for a yield of 9.42%. This is almost 10 times the S&P average, and a strong return for investors. Combined with a low share price, the dividend makes ET an attractive proposition.

RBC Capital’s 5-star analyst Elvira Scotto agrees that ET is a stock to buy. She wrote of the company last month, “ET recently reported strong 3Q19 results, increased its 2019 EBITDA guidance, lowered its 2019 growth capex and expects flat growth capex in 2020, which we view positively. We expect leverage to decline in the coming years as projects ramp.” Her price target, $20, suggests a 53% upside. (To watch Scotto’s track record, click here)

With 5 recent Buy ratings, ET shares get a unanimous Strong Buy from the analyst consensus. The stock sells for just $13.07, a low cost of entry for shares with a 36% return potential based on an average target price of $17.75. (See Energy Transfer’s stock analysis at TipRanks)

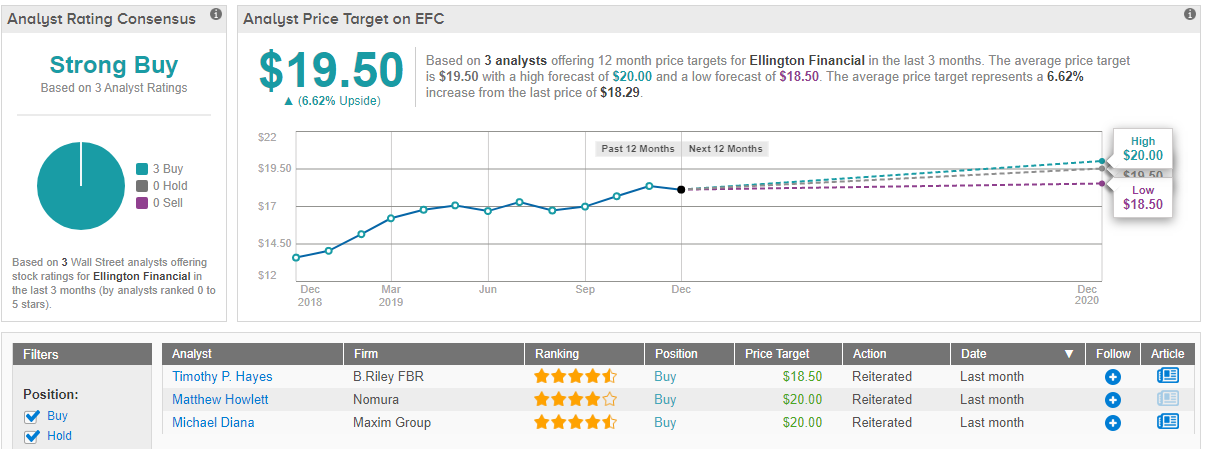

Ellington Financial, Inc. (EFC)

Ellington is a financial services company focused on mortgage-backed securities, mortgage loans in the residential and commercial segments, collateralized loan assets, and consumer loans. In short, it is similar to a real estate investment trust, but gets its hands into a wider array of assets and loan-backed asset packages.

That Ellington’s financial asset investments are profitable is clear from November’s Q3 report. The company showed 53 cents EPS, based on $17.3 million in net income. A stock offering during the quarter brought in over $69 million, showing that financial market watchers are willing to invest in this company.

One attractive feature of the stock is the dividend, which offers a yield of 9.22%. At current share prices, this comes out to an annualized payout of $1.68 per share, or 42 cents quarterly.

4-star analyst Matthew Howlett, of Nomura, is bullish on EFC’s prospects. He writes, “The good news is, with the stock now above book value, future capital raising is poised to be accretive to book value and should enhance EFC’s economic return,” and of the company’s short-term prospect, he adds, “Our investment thesis remains EFC is still on track to raise its dividend in 2020 as its core EPS ramps.” Howlett gives EFC a Buy rating with a $20 price target, suggesting a 9.4% upside. (To watch Howlett’s track record, click here)

EFC is another stock with unanimous support behind its Strong Buy consensus rating, this one based on 3 recent Buys. The $19.50 average price target indicates a 6.6% upside from the share price of $18.29. (See Ellington’s stock analysis at TipRanks)

See Also: 3 “Perfect 10” Tech Stocks Primed for Gains in 2020

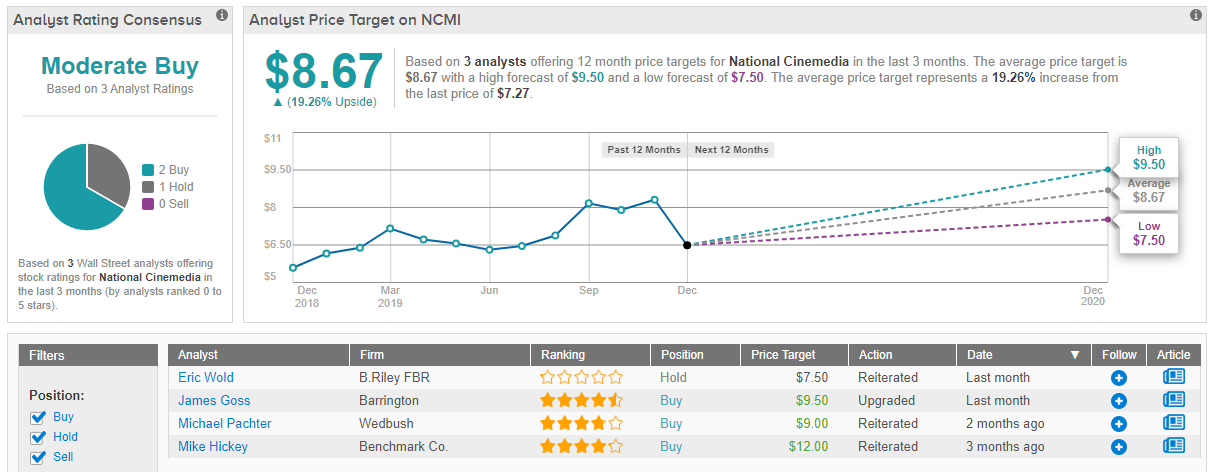

National CineMedia, Inc. (NCMI)

Hollywood and the theater companies aren’t the only ones making money from the movies. Those ads at the beginning of the show? Someone has to produce and distribute them as well as sell access to the advertisers. That’s NCMI’s niche. Apparently, captive audiences are a good one, because the company’s stock is up a modest 12% this year.

NCMI has had a hard time meeting quarterly expectations, however. The company showed 12 cents EPS in the last report, for Q3, against a 13-cent forecast. Revenues were also below the estimates, at $110.5 million, but slightly above the year-ago number.

For dividend-minded investors, those quarterly numbers bring a warning. The payout ratio is 159%, meaning the current payment is substantially higher than the earnings that support it. It is not sustainable – unless the company’s shares increase in value, but more on that below. For now, the dividend is 17 cents per quarter, annualized at 68 cents and showing a yield of 9.5%. That payment has been stable for two years.

Writing for Barrington, analyst James Goss sees a benefit for investors in the disappointing Q3 results, upgrading the rating from Market Perform to Outperform. He points out, “The post-earnings selloff in the shares has created an opportunity with the stock now yielding 9.5%. National CineMedia’s stable business model creates a situation in which the company can pay out roughly 80% of its free cash flow in dividends and distributions.” In line with Goss’ Buy stance, and his view that the stock price is at a discount, he gives a price target of $9.50, suggesting a 31% upside. (To watch Goss’ track record, click here)

NCMI has three recent reviews, including 2 Buys and 1 Hold, giving the stock a Moderate Buy consensus rating. Shares sell for just $7.27, but the average price target of $8.67 suggests an upside potential of 19%. If the stock realizes that potential, the high dividend yield will be easily sustainable. (See National CineMedia’s stock-price forecast and analyst ratings)