Income-minded investors are naturally drawn to dividends. These payouts from companies to shareholders are a natural way to share income with full ownership of the company, as well as a way to induce more investors to become shareholders. A strong dividend – one that is reliable, with a high yield – is steady source of return on a stock investment.

We’ve used TipRanks’ Stock Screener tool to search the market for Buy-rated investments with reliable high-yield dividend payouts. All three companies are in the energy sector, exploiting the rich oil and gas reserves which the American fracking boom has unlocked. We’ll look at each of them to see how their dividends measure up, and if the payout appears sustainable.

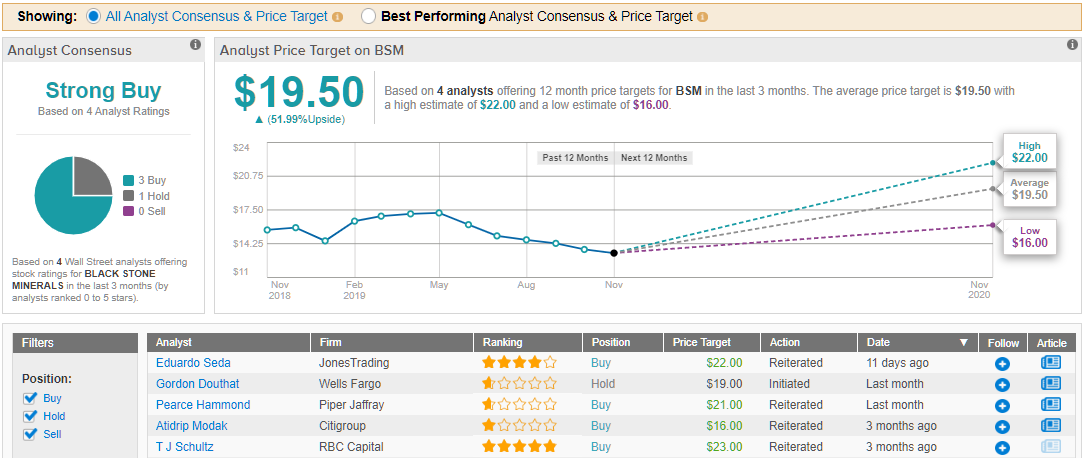

Black Stone Minerals (BSM)

With Black Stone, we get into Texas. Everything about Texas is big, including the oil industry. Houston-based Black Stone operates in the oil- and gas-rich Eagle Ford Shale, as well as across the Southeast, in the Dakota’s Bakken formation, and in the gas regions of Appalachia. Overall, the company controls production sites in 60 basins in 40 states.

BSM reported Q3 earnings after market on November 4, and showed an EPS of 32 cents, a 10% beat of the 29-cent estimate. Revenues just missed expectations, however, coming in at $137.4 million against the forecast of $139.5 million. Investors didn’t seem worried by the revenue miss, however, as shares gained 1.68% that same day.

While the earnings beat was welcome news, investors are also interested in the dividend. BSM pays out a yield of 11.3%, and has been growing that dividend for the last three years. The current quarterly payment is 37 cents.

A careful reader will note that the current dividend payment is higher than the EPS, and correctly point out that this implies an unsustainable payout ratio. However, as Piper Jaffray analyst Pearce Hammond points out, “BSM remains very disciplined on acquiring minerals. The higher distribution yield and resulting higher cost of capital make it more challenging on getting deals done relative to peers with a lower distribution yield… BSM has a solid balance sheet with a leverage ratio of 1.1x.”

Strong acquisition and low leverage lead Hammond to give a $21 price target, indicating confidence in a 57% upside – that would easily make the dividend sustainable. (To watch Hammond’s track record, click here)

4-star analyst Eduardo Seda, of Jones Trading, agrees that BSM has a rosy mid- to long-term outlook for growth. He writes, “BSM is One of the Largest Owners and Managers of Crude Oil and Natural Gas Mineral and Royalty Interests in the U.S… We note that BSM had recently raised its production guidance for full-year 2019 to a range of 47.5 MBoe/d to 50.5 MBoe/d, a 5% increase midpoint to midpoint from prior guidance…” Seda’s $22 price target suggests a 65% upside potential.

Overall, BSM holds a Strong Buy from the analyst consensus. In the last three months, 3 analysts have given the stock Buy ratings, against 1 who has set a Hold. Shares are currently trading for $12.69, so the $19.50 average price target implies an upside of 52%. (See Black Stone stock analysis on TipRanks)

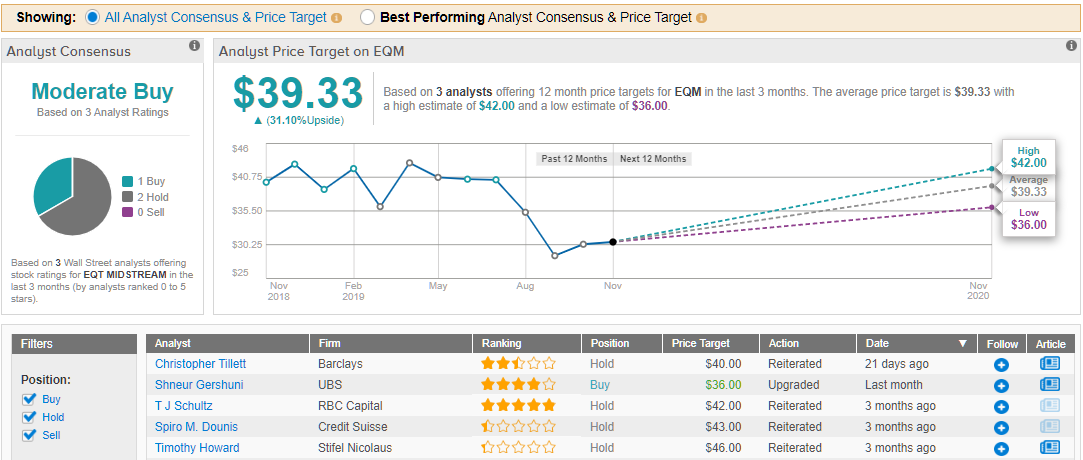

EQM Midstream Partners (EQM)

EQM bills itself as the low-cost service provider to the natural gas industry in the Appalachian basin, one of the richest natural gas regions in the United States. The company owns and operates natural gas pipeline and storage facilities across the basin, in western Pennsylvania, West Virginia, and Ohio. In addition, EQM operates water services, providing water supply and waste-water disposal for the fracking industry.

An essential niche in a profitable industry should equal a cash-flush company, but EQM has been facing serious headwinds. Earnings are forecast to drop this quarter on a year-over-year basis as capital expenditures shown a heavy increase in the last 15 months. In addition, the company’s major project, the MVP pipeline, is not yet complete and faces delays from legal and regulatory issues. Management has not been forthcoming on a timeline for resolution. Finally, EQM is heavily leveraged – long-term debt has increased 41% over the past hear, to $4.88 billion, and the company has $1 billion outstanding on its short-term credit facility of $3 billion.

All of this points to a company that is using debt to finance current projects on faith in future profits. While this is not unusual, 2020 is an election year, and most of the Democratic candidates are promising to shut down the fracking industry and curtail fossil fuels generally. With both the business and political fronts growing cloudy, what will bring in investors?

Income. EQM pays out a 15% dividend yield, and even after the shares’ recent depreciation, the quarterly payment is still $1.16. Compare this to the S&P average yield of just 2%, and you immediately see the appeal. The company has been increasing the dividend steadily for the last seven years; in November 2012, the quarterly payment stood at 35 cents. Finding reliable payments and steady increase are the keys to successful dividend-based income investing.

There is a cloudy spot – the payout ratio, the comparison of the dividend payout to the earnings per share – is 103%. Normally, this would not be sustainable, but the number is based on previous earnings, not forward estimates. A look at EQM’s most recent Buy rating, from UBS 4-star analyst Shneur Gershuni, shows why the high payout ratio may not be a deciding factor.

Gershuni says, “Given EQM’s 10% decline since early August, we are upgrading EQM to Buy from Neutral. We believe the scenario of MVP being cancelled is adequately reflected at these levels and believe the base business is priced at a discount with MVP in-service providing upside to our current price target. In the current volatile market conditions within energy, we favour midstream companies … that connect well-head to end markets.” In other words, all the headwinds mentioned above are baked into the stock price, which has bottomed out.

Gershuni sees EQM rising in the mid-term, and his $36 price target, implying 17% upside, reflects that. (To watch Gershuni’s track record, click here)

Overall, EQM gets a Moderate Buy from the analyst consensus. Shares are selling for $30, and the average price target of $39 suggests an upside of 31%. (See EQM stock analysis on TipRanks)

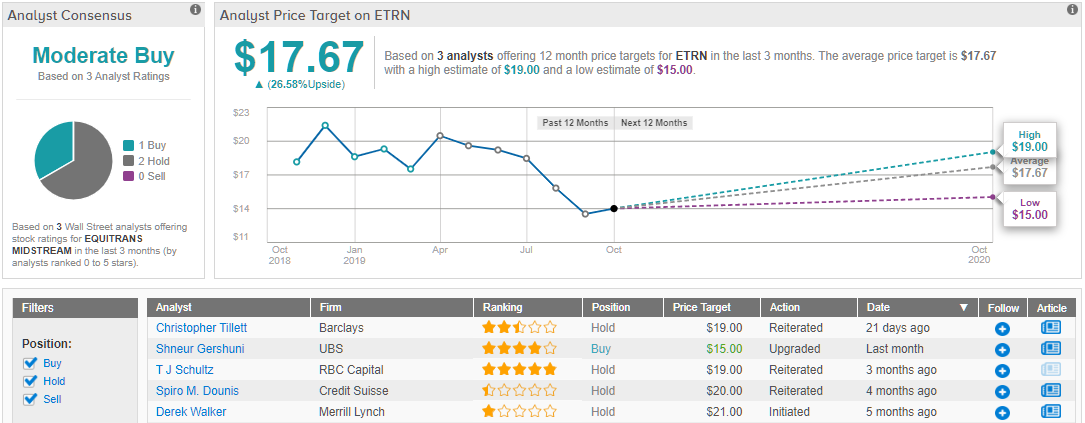

Equitrans Midstream (ETRN)

A spin-off of the natural gas producer EQT, Equitrans Midstream took on the parent company’s pipeline and services operations. As the name implies, Equitrans now handles the midstream operations while parent EQT focuses on drilling. ETRN has been operating independently since mid-2018. It has beaten earnings estimates, substantially, in two of the three quarters it has reported so far.

Equitrans operates natural gas gathering and transmission services in the Appalachian basin, as well as water services. In this respect, it is much like EQM above. In fact, like EQM, Equitrans is also a partner in the MVP pipeline project, and faces similar regulatory headwinds and delays – issues that have pushed the stock price down in recent weeks.

These are not the only similarities between the two companies. ETRN is another high-yield dividend payer, offering 12.7% annualized, for a quarterly payment of 45 cents per share. And again, the payout ratio of 117%, at first glance, shows cause for concern.

That concern, however, may be short lived. ETRN is to release earnings November 5, and predictions now are for an EPS of 35 cents – up 34% from previous estimates. In the last quarter, ETRN beat the forecast by 50%.

UBS’ Shneur Gershuni, linked above, sees this stock as another buying proposition, and for similar reasons to EQM. He writes of ETRN, “Given ETRN’s 12% decline since early August, we are upgrading ETRN to Buy from Neutral… Our upside scenario reflects full MVP in-service, 10% gathering volume growth, and no negative restructuring of gathering contracts implying a valuation of $25.”

Gershuni sets a $15 price target, which is conservative given his comments. It suggests a modest upside of 3.5% for the stock.

ETRN has a Moderate Buy consensus rating, and a 21% upside potential, based on an average price target of $17 and a current share price of $14.50. (See ETRN stock analysis on TipRanks)