The coronavirus outbreak has been taking up its fair share of headline space, and rightly so. The virus first appeared in Wuhan, China, but large-scale outbreaks are now appearing in South Korea, Iran and Italy. While healthcare companies are working around the clock to develop a vaccine, the reality for now is harsh: a rapidly spreading virus is causing major disruptions to international travel and trade. China’s economy has already taken a serious hit, and even Apple has announced that its Q1 2020 results will suffer badly from the economic impact of the coronavirus. As a result, the S&P 500 is down 12% from its February 19 peak.

Investors don’t want much, really: just a guaranteed return on a stock that pays back a steady income stream, even when markets tumble. It’s not too much to ask for. It can be hard to find, however. Strong returns – based on gains in share price – typically don’t go hand-in-hand with a steady income stream – based on dividends. The two forms of investment returns are based on different marketing and business strategies by the companies involved.

A careful look into the TipRanks database, however, can bring up intriguing choices for income-minded investors to study. The Stock Screener tool has filters to sort more than 6,200 stocks, making it a breeze to find the right one for your investment profile. Setting the filters to scan for tickers with over 5% dividend yields and “Strong Buy” consensus ratings, the search is narrowed to 41 companies. Here are three with a clear path forward and proven returns. Let’s take a closer look.

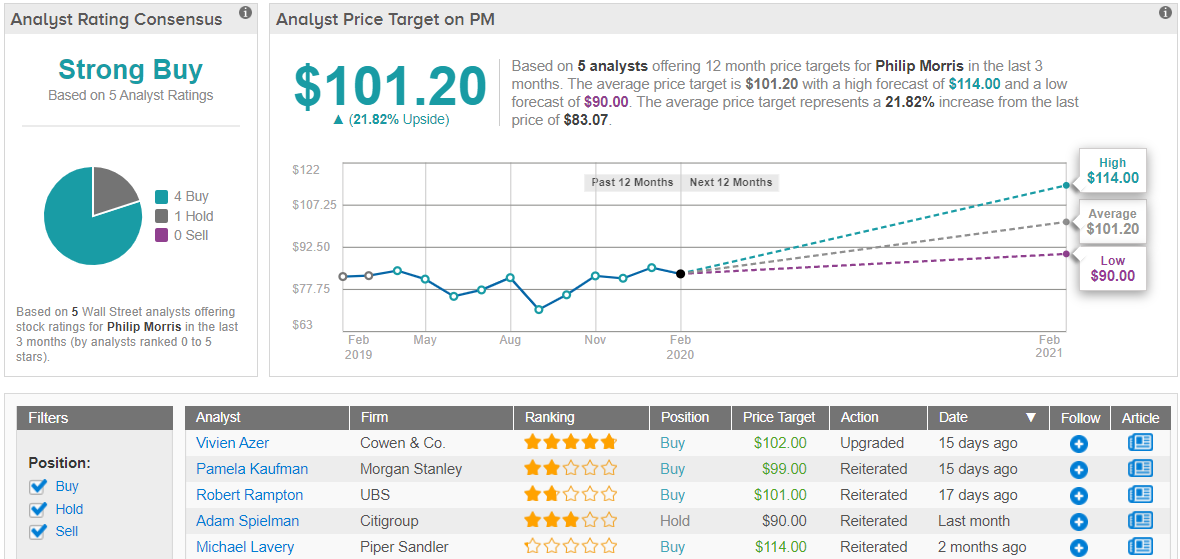

Philip Morris International (PM)

Sin stocks are a classic choice for dividend hunters. Most of us can agree that cigarettes and alcohol are just plain bad for you, and that they are addictive, but those very attributes help guarantee a high sales floor. Philip Morris has been riding that wave for decades.

There has been some interesting news about PM in recent months. In 2H19, the company entered into talks with Altria, its former parent, regarding a ‘merger of equals’ deal. Those talks were called off in September, much to investors’ pleasure. The companies will, instead, pursue a joint venture in iQOS, a heated smokeless tobacco product, in the US market. PM has already put some $6 billion dollars into iQOS, while Altria’s tobacco alternatives – in vaping – are facing serious regulatory and public relations challenges.

That being said, investors did get some good news after the company reported a Q4 earnings beat earlier this month. EPS beat the estimate by 1 cent, coming in at $1.22, and the $7.71 billion in revenue edged out the forecast by half a percent.

Investors will be pleased with PM’s dividend, too. The payment, $1.17 quarterly, annualizes to $4.68 and gives a yield of 5.51%. The company has a 12-year history of reliably maintaining the payment, and has raised it three times in the past three years. The yield compares favorably to the average among S&P listed companies, which is only 2%.

Piper Sandler analyst Michael Lavery reviewed this stock last week, and wrote, “We remain bullish on PM’s strong underlying core earnings growth and incremental iQOS earnings to be attractive, and it is our top pick in the space… We believe its 2020 guidance is appropriately conservative, though we believe it can exceed its minimum expectations. Buybacks may also be in play for 2021.”

Lavery maintained his $114 price target, implying room for a strong 32% upside potential, and reiterated his Buy rating. (To watch Lavery’s track record, click here)

Philip Morris’ Strong Buy consensus rating is based on 4 Buys against a single Hold, all set in recent weeks. The stock is selling for $83.07, and the $101.20 average price target suggests it has room to grow another 22%. (See Philip Morris price targets and analyst ratings on TipRanks)

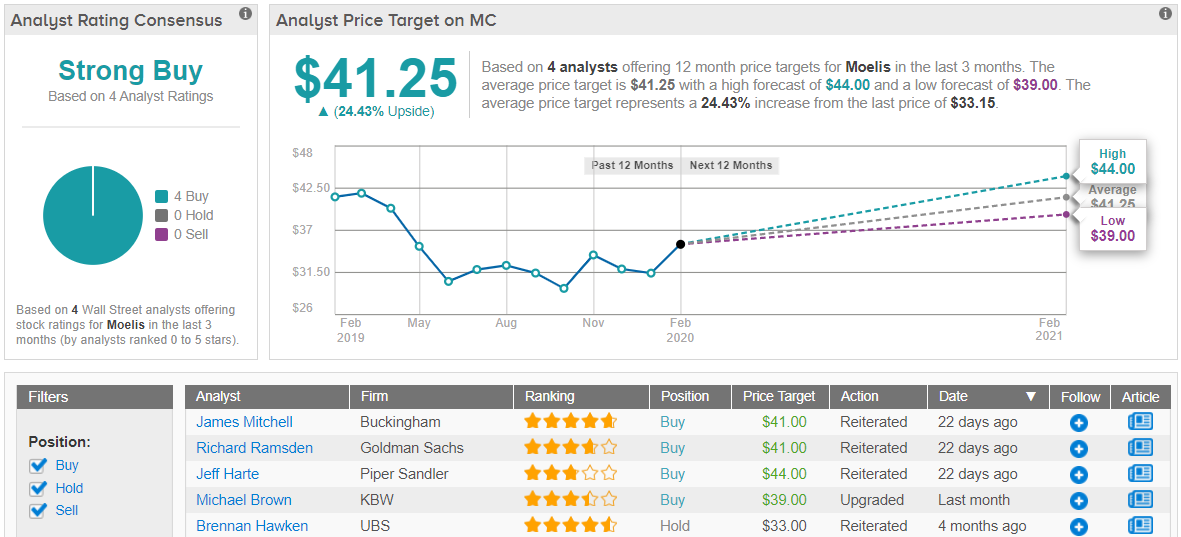

Moelis & Company (MC)

The next stock on today’s list, Moelis, is an investment banking company. The firm is an independent operator, offering advisory services to corporations, financial sponsors, and governments. Advisory services include recapitalizations and restructurings as well as mergers and acquisitions.

The financial industry’s services are always in demand, a fact which has supported this stock over the years, and shows in the quarterly reports. Even though Q4 revenues were down 6% year-over-year, at $223.5 million, and EPS slipped 51% year-over-year to 38 cents, both figures were well above Wall Street’s forecasts. It was the fifth quarter in a row that beat the forecasts.

A company that consistently beats earnings forecasts will surely attract attention – but so will a company that keeps up its dividend. MC announced a $1.26 per share payment this month, to be paid at the end of March. This is a jump from the usual quarterly divided of 51 cents – but it is consistent with company practice for February dividends. The annualized regular payment, at $2.04 per share, gives a yield of 5.96%, or nearly triple the S&P average.

Ken Worthington, reviewing MC for J.P. Morgan, likes what he sees. He writes, “Moelis continues to see a rather favorable macro environment lining up for a robust client activity outlook going forward, pointing especially to the private sector, where Moelis sees its strong relationship with sponsors paving the way for more sponsor-related deals.”

Worthington gives the stock a Buy rating and increased the price target from $44 to $49, implying robust upside potential of nearly 50%. (To watch Worthington’s track record, click here)

Also bullish is Jeff Harte from Piper Sandler. Harte was impressed by the company’s earnings, especially that EPS beat the forecasts. In line with this development, Harte says, “We are increasing our 2020 EPS estimates from $2.98 to $3.00 and initiating a 2021 EPS estimate of $3.14.”

Harte puts a Buy rating on this stock along with a price target of $44. His target indicates a 33% potential upside to the shares. (To watch Harte’s track record, click here)

Overall, Moelis has a unanimous Strong Buy consensus rating, based on 4 recent Buy-side reviews. The average price target is $41.25, suggesting an upside potential of 17%. (See Moelis stock analysis on TipRanks)

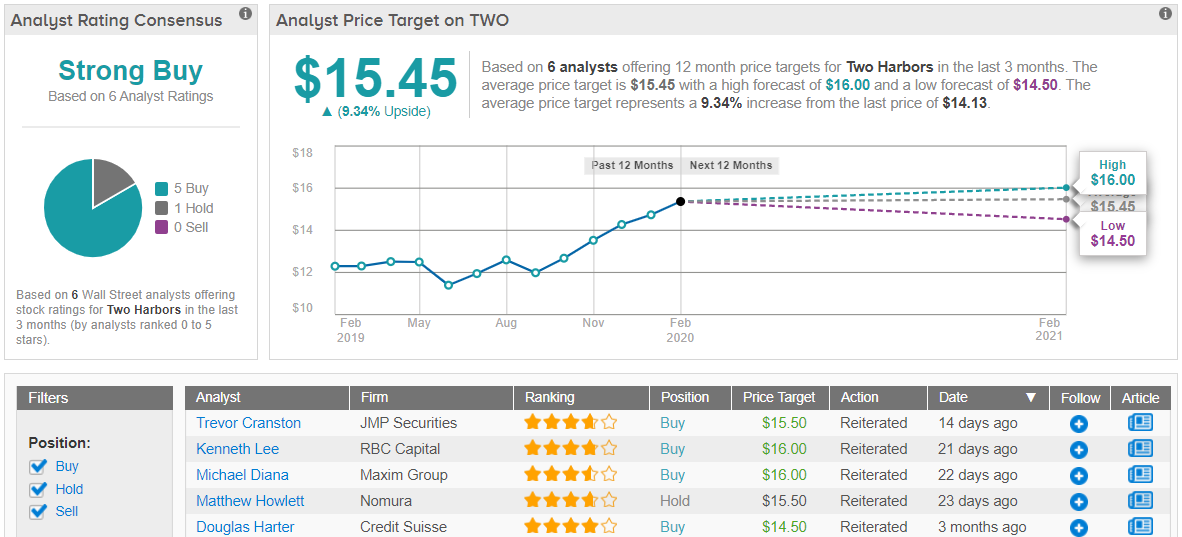

Two Harbors Investment (TWO)

Last on our list today is a Real Estate Investment Trust (REIT), another classic dividend choice. And no wonder why – required by tax code to return most of their profits to investors and shareholders, these companies have some of the highest dividend yields among publicly traded stocks.

TWO is no exception. This company, which owns both real properties and mortgage-backed securities, with a focus on residential properties, pays out 40 cents per share quarterly, or $1.60 annualized. This equates to a dividend yield of 10.86%, more than 5 times the average – and more than 6 times the yield of Treasury bonds.

The company did have a disappointing Q4, though. TWO reported EPS of just 25 cents, 11 cents below estimates, and shares slipped after the news. Revenues, however, beat the forecast handily by $8.7 million, coming in at $71.2 million.

Writing on the stock after the earnings report, JMP Securities analyst Trevor Cranston said, “We currently expect the $0.40 dividend to be sustained for the foreseeable future, as management indicated that it views the underlying return profile of the portfolio as continuing to support that figure. This dividend level provides a yield of 10.86% on the current share price.”

Cranston’s optimism on the dividend prompted his Buy rating on the stock. He gives TWO shares a $15.50 price target, suggesting room for 10% upside potential. The real attraction for investors here is the powerful dividend return. (To watch Cranston’s track record, click here)

All in all, with 5 Buy ratings and only 1 Hold, Two Harbors gets a Strong Buy rating from the analyst consensus view. Shares are priced at $14.13 and the upside potential stands at 9%, based on an average price target of $15.45. (See Two Harbors stock analysis on TipRanks)