After a stock takes a tumble, wait just a minute before you count it out. While falling share prices could be a sign that a company is under duress, it doesn’t always mean that its growth story has come to an end. After all, a tried and true strategy to turn a profit in the market is to buy low and sell high.

Wall Street pros remind investors to take this into consideration when gauging the strength of investments in the healthcare space. As these names rely on only a few key catalysts, all it takes is a single piece of bad news to send shares spiraling downwards. However, the opposite is also true, so one favorable outcome can put a stock right back on track.

With this in mind, we used TipRanks’ Stock Screener tool to pinpoint 3 Buy-rated healthcare names that the analysts believe are on the mend after recent nose dives. Here’s the scoop straight from the analysts.

BioMarin Pharmaceutical (BMRN)

BioMarin has established itself as a key player in the biopharma space, with seven therapies already on the market and several other candidates in development. Despite falling 21% in the first nine months of 2019, SunTrust Robinson analyst Robyn Karnauskas believes that important upcoming catalysts could drive a rebound.

The four-star analyst points out that the drop came largely as a result of declining investor confidence in the market potential of its Hemophilia therapy. ValRox, its Hemophilia A candidate progressing through Phase 2, has seen factor levels drop since the first year. However, Karnauskas remains convinced that BMRN can deliver.

After conducting a survey to determine if the concerns related to commercialization were valid, the analyst concluded that ValRox could drive significant growth. “Our survey indicates high level of confidence in approval of ValRox, with 100% of doctors expecting approval and steady uptake in severe Hemophilia A patients… Our survey also indicated that doctors are likely to prescribe based on label and do not expect all severe patients to qualify,” she commented.

As a result, the analyst believes, “At current values, the stock is trading with little credit to late stage pipeline assets with potential launches in late 2020/2021.” At the peak, Karnauskas estimates the Hemophilia A opportunity to be $1.48 billion.

On top of this, its vosoritide therapy for achondroplasia could be a major component of the company’s next leg of growth, with it reporting positive Phase 3 data in December.

Based on all of the above, Karnauskas tells investors that she’s siding with the bulls, reiterating a Buy rating on BMRN alongside a $110 price target. Should the target be met, shares will be in for a 24% twelve-month gain. (To watch Karnauskas’ track record, click here)

Turning now to the rest of the Street, it appears that other analysts are generally on the same page. With 13 Buys and 3 Holds assigned in the last three months, the consensus rating comes in as a Strong Buy. In addition, the $111.71 average price target puts the upside potential just above Karnauskas’ forecast at 25%. (See BioMarin stock analysis on TipRanks)

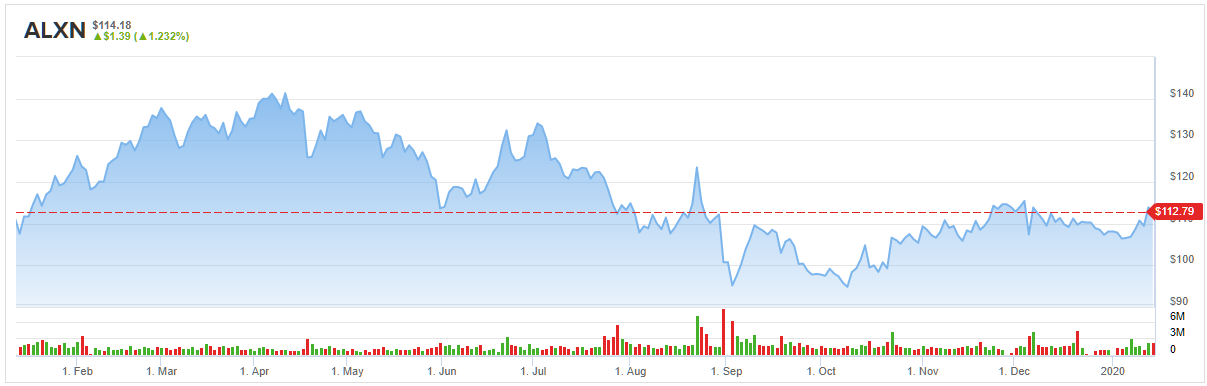

Alexion Pharmaceuticals (ALXN)

Fighting rare diseases like generalized myasthenia gravis (gMG), neuromyelitis optica spectrum disorder (NMOSD) and ALS, Alexion Pharmaceuticals wants to meet the large unmet medical needs of patients globally. Even though the company took a beating in 2019, the Street isn’t giving up on ALXN just yet.

While recent data for its candidate to treat PNH, a severe and ultra-rare blood disorder, raised some questions, Wedbush analyst Laura Chico believes its growth prospects are still strong. According to its most recent 8-K filing, total revenue growth is expected to beat the consensus estimate, and Ultomiris is poised to meet its conversion goals. As a result, Chico commented, “we continue to see ALXN as holding a strong competitive position in the complement markets.”

It also doesn’t hurt that its neurology franchise is continuing to grow at a steady rate. Over the previous quarter, neurology patients on treatment (gMG/NMOSD) increased 23% to 1,885 patients. Despite the fact that growth slowed by about 5% compared to September/June, management told investors that they are hoping to quadruple their US neurology patient volume by FY25.

All of this prompted Chico to conclude, “Overall, we see multiple encouraging updates from ALXN in their upcoming presentation not only on the commercial front, but with several pipeline updates as well. We continue to hold a positive bias on ALXN shares.”

To this end, Chico decided to leave the Outperform rating and $149 price target unchanged. At this target, a 32% gain could be in the cards for ALXN over the next twelve months. (To watch Chico’s track record, click here)

Like Chico, a majority of the analysts covering ALXN take a bullish approach. With 12 Buys and 3 Holds, the word on the Street is that ALXN is a Strong Buy. The healthcare stock boasts 29% upside potential based on the $145 average price target. (See Alexion stock analysis on TipRanks)

Mylan N.V. (MYL)

Mylan, one of the largest generic drug makers, has had a rough going, to say the least. Back in May, shares shed 24% of their value in a single day after the company failed to provide an update on the strategic review that had already lasted ten months. More recently, the stock has been range-bound thanks to investor concern regarding a possible cut to Viatris, the combination of Mylan and Pfizer’s Upjohn, as well as its proforma numbers. That being said, some members of the Street still have high hopes for MYL.

RBC Capital’s Randall Stanicky thinks that several key factors suggest that MYL has more fuel left in the tank. “We believe buyside expectations are already low with Street proforma models stale while synergies provide support into 2022 stabilization; even on our lowered EBITDA, Newco trades at only 6.6x 2021E EBITDA (<7x even if further cutting EBITDA to $7 billion) while able to support a new dividend yielding about 4%,” he explained.

Additionally, the analyst highlights improving corporate governance as well as argues that Viatris’ U.S. generic revenue and limited opioid exposure could help the company “de-couple from generic peers.” He added, “The announced combination of MYL and PFE’s Upjohn off-patent business will further grow and diversify MYL’s revenue base beyond US generics.”

Given that it still boasts “one of the best generic/ biosimilar pipelines in the industry”, Stanicky’s bullish thesis remains firmly intact. With this in mind, the analyst maintained an Outperform call. Not to mention, he bumped up the price target from $25 to $27. The price target conveys the analyst’s confidence in MYL’s ability to surge 27% in the next twelve months. (To watch Stanicky’s track record, click here)

Looking at the consensus breakdown, we have an almost even split. 4 Buys and 5 Holds received in the last three months add up to a Moderate Buy consensus rating. With a $24.50 average price target, the upside potential is 16%. (See Mylan price targets and analyst ratings on TipRanks)