With the holiday season kicking off, investors are shopping the Street for growth stocks. Stocks of this kind have a clear runway for growth, capable of delivering massive returns in the years to come. No wonder they are topping wish lists.

However, in a year that has seen the market reach record highs, tracking down these names is becoming harder and harder to do. But don’t sound the alarm bells just yet. Wall Street pros remind investors that stocks with outsized growth prospects are still out there.

In an attempt to lock down these compelling investment opportunities, we turned to TipRanks. The platform’s Stock Screener tool was able to scan the Street for the crème-de-la-crème. We mean the tickers offering up serious upside potential from current levels.

Let’s get started.

GDS Holdings Ltd (GDS)

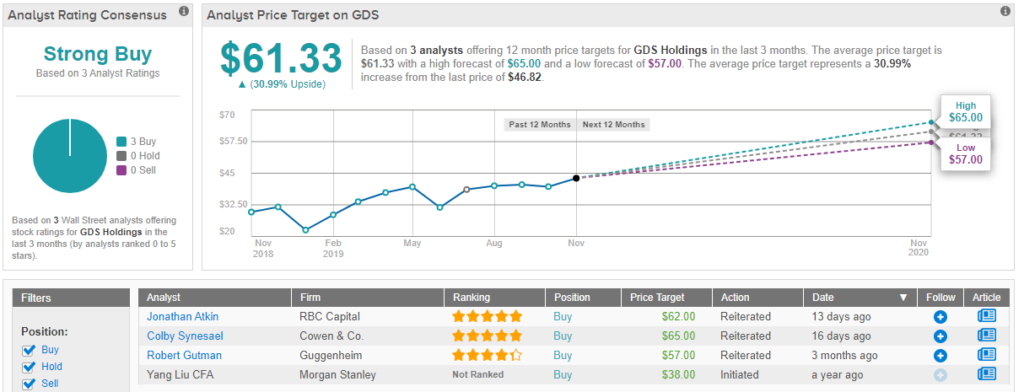

At a 103% year-to-date gain, all eyes are on GDS Holdings. This combined with a solid Q3 performance and strong long-term growth narrative has made the Chinese data center developer and operator a must-have name among several analysts.

During the third quarter, the company saw revenue of RMB1,066 million, inching past the consensus estimate by about a percent. On top of this, service revenue increased 41% year-over-year and net loss narrowed from the prior-year quarter.

That being said, Cowen & Co. analyst Colby Synesael points to its positioning in terms of demand as a key takeaway. “We believe the company continues to be well positioned in what is arguably the strongest data center market in the world and is taking the right steps to secure significantly more supply in its major markets as it prepares for even stronger demand in 2020,” he commented. Despite the five-star analyst’s prediction of continued macro and trade-driven volatility, he believes shares are set to climb higher in 2020. Taking this into consideration, Synesael reiterated his Outperform rating and bumped up the price target from $53 to $65. This bolstered target lends itself to a 39% potential twelve-month gain. (To watch Synesael’s track record, click here)

Meanwhile, RBC Capital’s Jonathan Atkin cites the development pipeline as placing GDS on an upward trajectory. With GDS recently getting the go-ahead for 13,000 square meters of downtown capacity in Shanghai and its potential purchase of a second site in Hong Kong, total capacity lands at 230,000 square meters. “We believe, based on our discussions with industry contacts, that there is significant progress yet to come for additional edge-of-town deployments as well as new Tier 1 markets,” he noted. As a result, Atkin is staying with the bulls. Not to mention he lifted the price target by 40% to $62, indicating 32% upside potential. (To watch Atkin’s track record, click here)

Similarly, the rest of the Street has been impressed by GDA. 100% Street support implies a clear message: the stock is a Strong Buy. In addition, the $61 average price target puts the upside potential at 31%.(See GDS Holdings stock analysis on TipRanks)

ACADIA Pharmaceuticals, Inc. (ACAD)

ACADIA Pharmaceuticals wants to help patients battling central nervous system (CNS) disorders. When we say this name has soared year-to-date, we aren’t kidding. We’re talking 180% here. Still, analysts think that this is just the beginning.

On November 25, ACAD released topline results from the ADVANCE Phase 2 trial of its pimavanserin drug in schizophrenia patients. According to the data, patients given the treatment witnessed a great improvement in Negative Symptom Assessment-16 (NSA-16) total score compared to the placebo. However, the results were somewhat of a mixed bag as it failed to demonstrate a superior performance vs the placebo in terms of the Personal and Social Performance (PSP) scale.

Nonetheless, Cowen’s Ritu Baral maintains a bullish thesis. “Overall, we view these results to have little impact on ACAD shares due to the earlier stage of this program and the smaller market size of schizophrenia patients with predominant negative symptoms relative to pimavanserin’s new opportunity in Dementia-related psychosis (DRP),” she explained. The five-star analyst goes on to cite the Phase 3 HARMONY study in DRP patients as an upcoming catalyst.

If this wasn’t promising enough, its trofinetide drug to treat patients with Rett Syndrome could also drive substantial gains. Rett Syndrome is a primarily female congenital neuro-developmental CNS disorder affecting cognition and sensorimotor function. Given that the drug demonstrated statistically significant results in a Phase 2 study as well as its potential to treat Fragile X Syndrome or traumatic brain injuries, Baral kept the recommendation as Outperform. Based on the $66 price target, she sees 46% upside potential in store. (To watch Baral’s track record, click here)

In general, Wall Street likes what it’s seeing. 11 Buys and 2 Holds received in the last three months add up to a Strong Buy analyst consensus. At the $56 average price target, shares could surge 23% in the next twelve months. (See ACADIA Pharmaceuticals stock analysis on TipRanks)

Pegasystems Inc. (PEGA)

Pegasystems offers cloud-based software for customer engagement and other operational needs, with its low-code application development platform allowing organizations to quickly build apps to meet their customer and employee requirements. Considering the noteworthy 62% jump year-to-date, one analyst is betting that PEGA will come out on top in the long-run.

Wedbush analyst Steven Koenig was impressed by PEGA’s third quarter results. Despite the fact that investments in cloud infrastructure and government certifications weighed on EPS, annual contract value growth of 20% year-over-year and a 7% revenue gain landed right in-line with consensus estimates. While PEGA may be impacted by the shift to a cloud-first model, the analyst expects this change to pay off long-term, deeming the software company a “Wedbush Best Idea”.

“Investments in sales talent and capacity should drive better penetration of large accounts, perhaps the key to lifting underlying growth rates beyond the 20% level. With shares trading at 5.6x EV/FY20E revenue and key metrics inflecting positively, we see PEGA as a top pick into FY20 for GARP-oriented software investors,” he wrote in a note to clients.

Bearing this in mind, Koenig tells investors his conclusion that PEGA will ultimately outperform remains unchanged. Along with the recommendation, the five-star analyst kept the price target at $95. This conveys his confidence in PEGA’s ability to rise 22% in the coming twelve months. (To watch Koenig’s track record, click here)

Looking at the consensus breakdown, it has been relatively quiet in terms of analyst activity. In the previous three months, PEGA racked up 1 Buy rating, giving it a Moderate Buy consensus. Additionally, the average price target of $95 implies 22% upside potential. (See Pegasystems stock analysis on TipRanks)