The market gyrations leave traders looking to get out, which reinforces the bear trends and deepens the drops, or looking for discount stocks that may offer solid returns for a low cost of entry. Which, when you think about it, brings penny stocks to mind.

These are low-cost shares, usually in low-cap companies. Historically, these stocks were valued at less than a dollar, although today penny stocks are defined as selling for less than five dollars. The main attraction here is a consequence of the low share price: even a modest-seeming dollar gain per share can translate into a high-percentage return.

We’ve used the TipRanks Stock Screener to find three penny stocks with Strong Buy consensus ratings and over 100% upside potential – in other words, stocks that are cheap to buy and are tapped to double – at least – in the coming year. Let’s take a closer look.

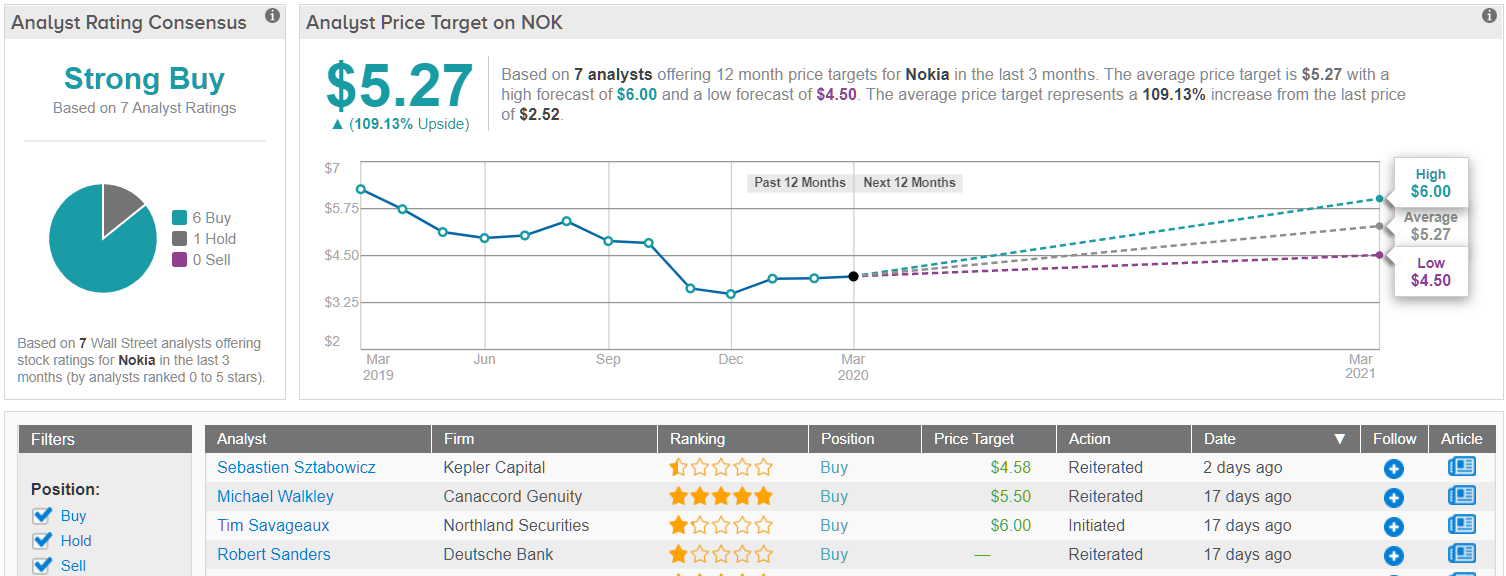

Nokia Corporation (NOK)

The Nokia name is familiar; the company has been a well-known maker of cellular handsets for decades, and is famous in part for its 3310 ‘dumb phone,’ which even today boasts strong sales.

As Nokia heads into the new year, it is also preparing for a changeover in management. CEO Rajeev Suri will step down this coming August, to be replaced by Pekka Lundmark of Fortum. While at Fortum, a Finnish energy company, Lundmark oversaw a 35% increase in share value. Suri will remain as an advisor to the Board until the end of the year.

Nokia’s strong sales are clear from the Q4 2019 report. The company showed a 563 million Euro ($604 million US) profit, coming out to 10 Euro cents per share (or 10.7 cents US). This was triple the year-ago profit, and highlighted the company’s turnaround from 2018’s steep full-year loss of 549 million Euro ($589 million US). Full-year profit in 2019 came out at 18 million Euro ($19.34 million US).

The company’s Networks segment drove the profit gains, for the quarter and the year. Nokia is a major player in developing 5G networks, as well as producing 5G capable handsets. The rollout of the new digital network tech is expected to bring a boon to the company as customers upgrade their mobile devices.

Wall Street’s analysts are taking a positive stance on Nokia. In a report earlier this month, Deutsche Bank analyst Robert Sanders sees a clear path for Nokia to build its 5G future: “After the mis-steps of 2018 and 2019, we believe mid-band 5G deployments using C-band in the US starting at the end of 2021 will be an important feature of Nokia’s turnaround. The news over the weekend that the C-band spectrum auction should happen at the end of 2020 provides a target to focus minds at Nokia: be ready with a leading 5G hardware solution in Q1 2021 to recover lost confidence with tier-1 operators…”

Sanders’ Buy rating on Nokia is support by his €4.50 ($4.85) price target, which suggests an upside of 91%. (To watch Sanders’ track record, click here)

Echoing Sanders’ view, UBS analyst David Mulholland is also bullish on NOK shares, placing a Buy rating alongside a €4.50 ($4.85) price target.

In his comments on the stock, Mulholland says, “At this point we believe many of the initiatives underway at Nokia are necessary to help drive the business and we do expect to see progress this year however we also believe that a new CEO will help the investor / stock market discussion start focusing on the future driving Nokia forward instead of focusing on how the current challenges arose.” (To watch Mulholland’s track record, click here)

Over the past three months, Nokia stock has received a 6 Buy ratings and just 1 Hold. As a result, the stock has a ‘Strong Buy’ analyst consensus rating. These analysts believe (on average) that Nokia has big upside potential of over 100% from the current share price. This would take the telecom equipment maker from $2.53 all the way to $5.27. (See Nokia stock analysis on TipRanks)

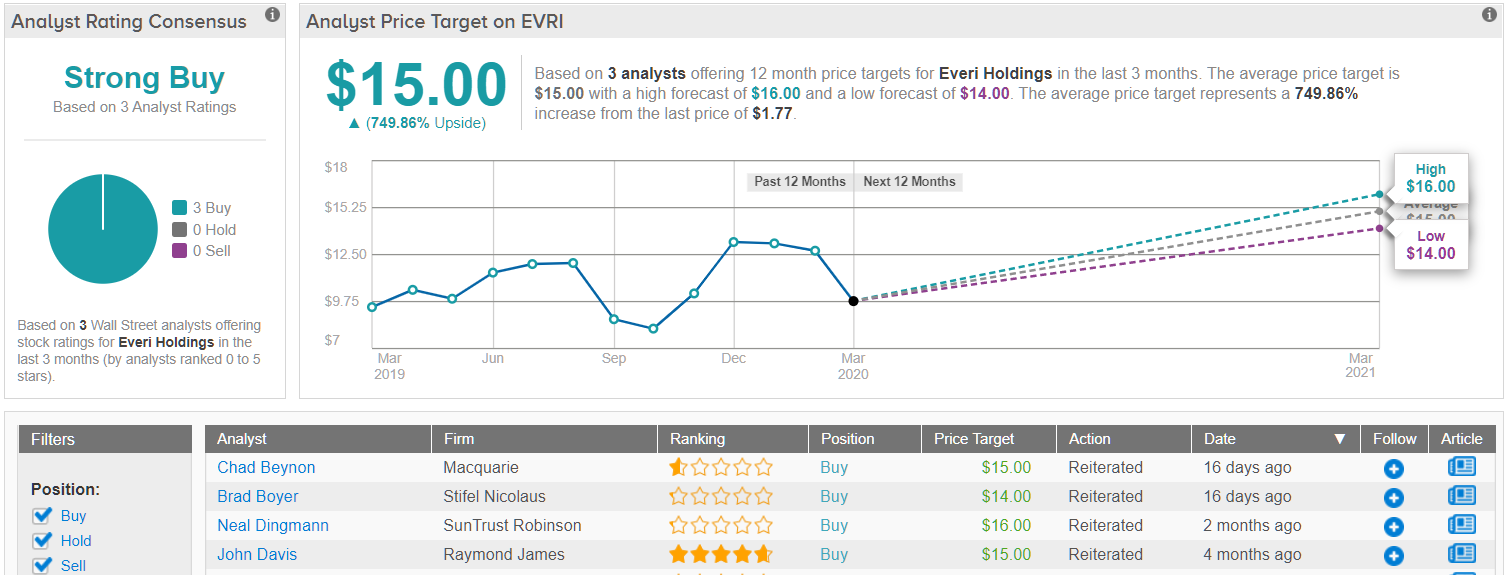

Everi Holdings (EVRI)

And now we move to a niche that usually drips money – casino gaming. Nevada-based Everi controls subsidiary companies that design, develop, and manufacture casino games for brick-and-mortar operations. The social distancing restrictions being put in place have hurt casino traffic and forced shutdowns, which in turn is weighing heavily on Everi stock.

But there are signs that this stock has resources that may not be immediately visible. In recent months, the insider sentiment has skewed sharply positive, as company officers have been buying shares but not selling. Two notable purchases came earlier this week: Board of Directors members Eileen Raney and Maureen Mullarkey bought 20,000 and 10,000 shares respectively, for $120,000 and $60,000 dollars. Raney’s purchase was the largest single insider buy in the company’s history. More importantly, the two Directors were willing to pay $6 or more per share, while the stock is currently trading below $2.

A look at Everi’s Q4 report, released earlier this month, may shed some light. EPS was slightly disappointing – it came in at just 2 cents per share compared to the forecast of 8 cents. At the same time, earnings were up significantly from one year ago, when the company lost 4 cents per share. Revenue was just strong. It grew 21% year-over-year, coming in at $145.18 million, and beat the forecast by 9%.

Growing revenues provide Everi with a solid base to weather the current market storms. As for future prospects, the current restrictions will last forever – and when they are lifted, there will likely be strong pent-up demand for services and leisure. And Everi is well-placed to make additional gains should that occur.

Wall Street in bullish on Everi. Writing for Craig-Hallum, 5-star analyst George Sutton says, “[T]he 35% pullback over the past few weeks appears to be quite opportunistic to us. Fundamentally, the company continues to see very strong premium games growth, nicely outpacing the industry and with a splurge of new products coming we see no signs of a slowdown… as we look further forward, the increased investment being made in the “integrated gaming neighborhood” area, including a mobile wallet, positions the company even better for the next leg of industry growth.”

Sutton placed a Buy rating on EVRI shares, and his $16 price target, indicating a whopping 809% upside, shows the extent of his confidence. (To watch Sutton’s track record, click here)

Barry Jonas, of SunTrust Robinson, noted of Everi, “…management did caution they believe operators will likely be cautious in the near-term as they allocate capital given the macro uncertainty. That said, 1) early year caution is consistent with purchasing patterns over the past several years, and 2) EVRI does benefit from strong diversification across the US should the Strip/certain regional markets experience a more pronounced decline in casino visitation related to the outbreak.”

Jonas remains bullish, with his Buy rating also supported by a $16 price target. (To watch Jonas’ track record, click here)

EVRI shares have a Strong Buy consensus rating, based on 3 unanimous Buy-side reviews. Shares are priced low, at just $1.65, while the $15 average price target suggests room for an impressive 750% upside potential. (See Everi stock analysis on TipRanks)

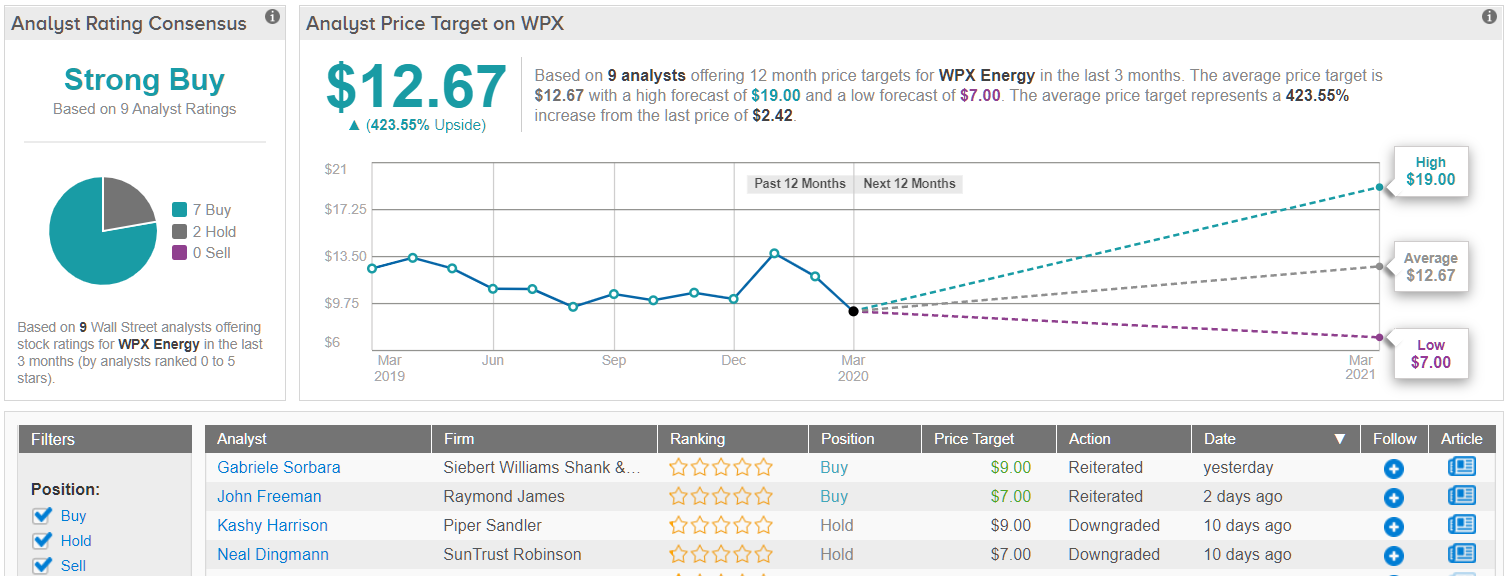

WPX Energy (WPX)

From casino games, we shift gears to the energy industry. WPX holds oil exploration and production assets in two of the richest petroleum formations in North America: the Williston Basin of North Dakota and the Permian Basin of West Texas. The company operates over 700 wells, which tap into proven reserves exceeding 480 million barrels of oil equivalent. And with a share price of just $2.11, the black gold has never been more affordable.

Low oil prices have weighed on WPX’s earnings in recent months, and the company reported an EPS miss in Q4. The 10-cents per share reported was 16% below expectation. Revenues also disappointed, as the $443 million figure missed the forecast by 30% and slipped 18% yoy.

In a move to balance the long-term view that oil will remain low, WPX announced earlier this week that it will reduce its capex in 2020 by almost 25%. In dollar terms, the company expects capital expenditures in the $1,275 to $1,400 million range, down from the previous guidance of $1,675 to $1,800 range. With WTI down to just $22 per barrel, and Brent at $25, there was really no way for the company to avoid cuts in expenditures – production simply cannot be ramped up enough to compensate for current prices.

In a report for Wells Fargo, analyst Nitin Kumar writes, “With the stock trading at a significant discount to peers… we see a favorable risk-reward profile. There are some near term headwinds… but long term … WPX [should] deliver on its 5 year vision to deliver return metrics that are competitive with the broader market…” Kumar’s $12 price target implies a hefty upside of 468%, and back up his Buy rating.

WPX has an average price target of $12.67, indicating room for a 423% upside potential. The stock’s Strong Buy consensus rating is based on 9 reviews, including 7 Buy-side and just 2 Holds. (See WPX stock analysis on TipRanks)