Has the energy sector been reinvigorated? Judging by the XLE Energy ETF’s 6% rally over the last month, some investors think that this might just be the case.

That being said, the Street’s experienced pros remind investors that not all of the names in the space are clear winners. Given the industry’s resurgence, what’s the best way to scope out the energy stocks poised to outperform?

Upon first glance, it can be tempting to only look at a single factor like fundamentals to try and gauge the strength of an investment. However, this is just one piece of the puzzle. To see the bigger picture, we turned to TipRanks’ Best Stocks to Buy tool.

The tool helped us zero in on 3 energy stocks that have earned a “Perfect 10” Smart Score, a single number that combines 8 metrics measured by TipRanks’ algorithm, with 10 being the highest. This score is generated by weighing hedge fund activity, analyst consensus and price targets, insider trades, as well as several other key factors.

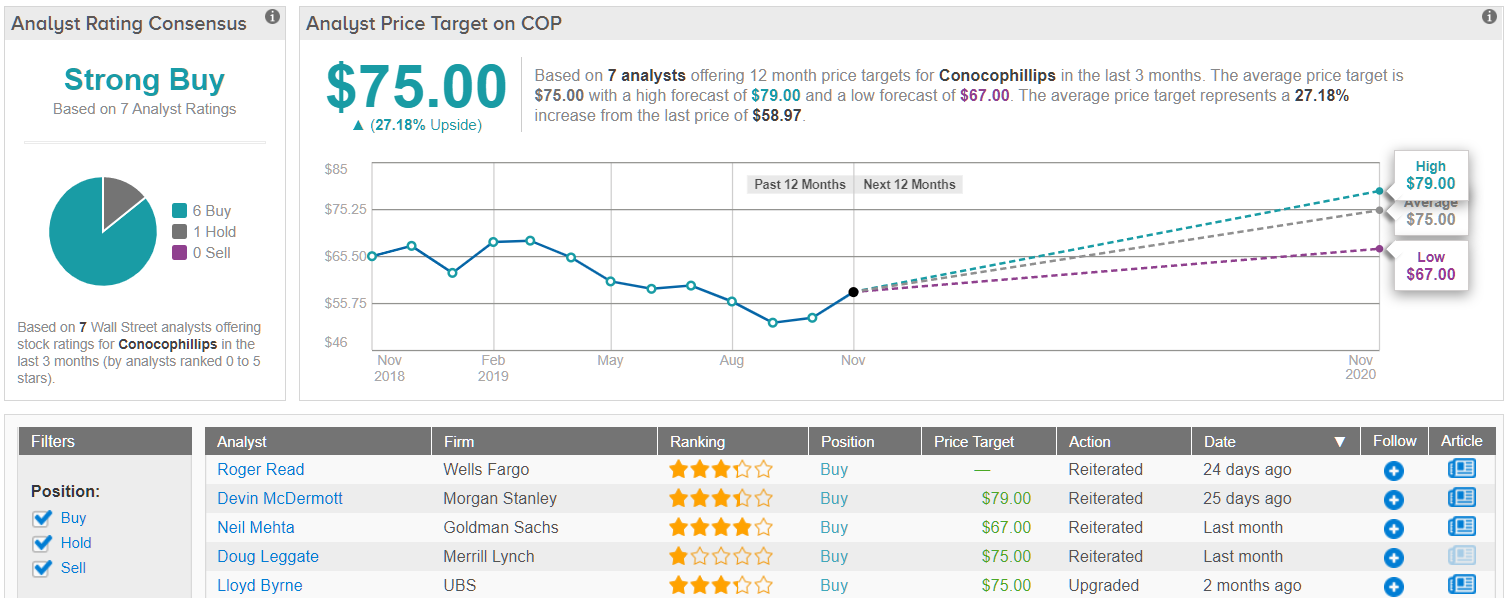

ConocoPhillips (COP)

Despite seeing its shares struggle year-to-date, the largest independent crude producer in the U.S. is staging a noteworthy turnaround.

According to the oil company’s Q3 earnings release, COP has a lot to brag about. While some had originally expressed concerns regarding the impact of lower crude prices and increased exploration costs, the company was able to post an earnings beat. Quarterly profits surpassed the consensus estimate thanks to strong shale production as well as asset sales gains.

Total production, before factoring in its Libyan assets, increased by 98,000 barrels of oil equivalent per day (boe/d) and U.S. shale basin output gained 21% in the quarter. The shale regions include Eagle Ford, Bakken and the Permian Basins.

The company has also made a significant effort to divest from assets in the U.K., with this move generating $2.2 billion.

Nonetheless, Mizuho analyst Paul Sankey’s key takeaway from COP’s earnings results is its ability to remain a high dividend payer. With the company upping the quarterly payout by 38%, the analyst believes that COP is “uniquely positioned to deliver on it right now.”

Taking this into consideration, Sankey maintains his bullish approach. Additionally, his $80 price target indicates 39% upside potential. (To watch Sankey’s track record, click here)

Similarly, the rest of the Street likes what it’s seeing. With 6 Buy recommendations and 1 Hold issued in the last three months, COP is a ‘Strong Buy.’ Share prices could also surge 27% based on the $75 average price target. (See ConocoPhillips stock analysis on TipRanks)

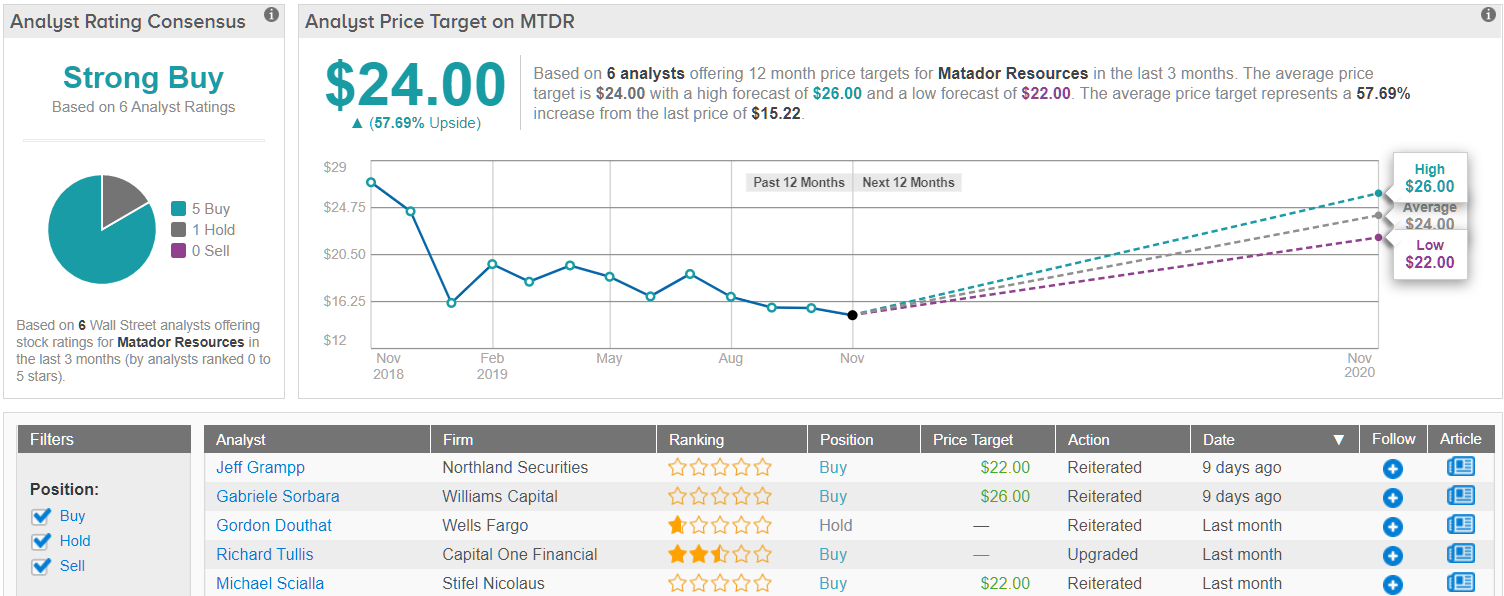

Matador Resources (MTDR)

Matador Resources is an independent energy company focusing on oil and natural gas exploration in the Delaware Basin as well as the Eagle Ford, Cotton Valley and Haynesville shale plays. With shares climbing 8% higher following a solid third quarter performance, it’s easy to see why MTDR is on the Street’s radar.

The company reported on October 30 that average daily oil equivalent production reached an all-time quarterly high. We’re talking 69,600 boe/d or a 14% sequential increase. This accomplishment comes as a result of strong initial performance from certain wells in the Antelope Ridge and Rustler Breaks regions as well as the completion of several new wells. If that wasn’t promising enough, average daily natural gas production also broke MTDR’s record.

Not to mention MTDR is right on track to meet its free cash flow targets thanks to its operations, E&P and midstream segments, according to Stephens analyst Gail Nicholson. He adds that Matador is a compelling investment due to its exposure to the Delaware Basin and “compelling rate of change story.”

All of the above factors prompted Nicholson to give the company a ratings boost. Along with the upgrade, his $24 price target conveys his confidence in MTDR’s ability to soar 60% over the next twelve months. (To watch Nicholson’s track record, click here)

In general, other Wall Street analysts are optimistic when it comes to MTDR. The stock has a ‘Strong Buy’ Street consensus due to the 5 Buy ratings and 1 Hold it racked up over the last three months. Its $24 average price target implies upside potential of 58%. (See Matador Resources stock analysis on TipRanks)

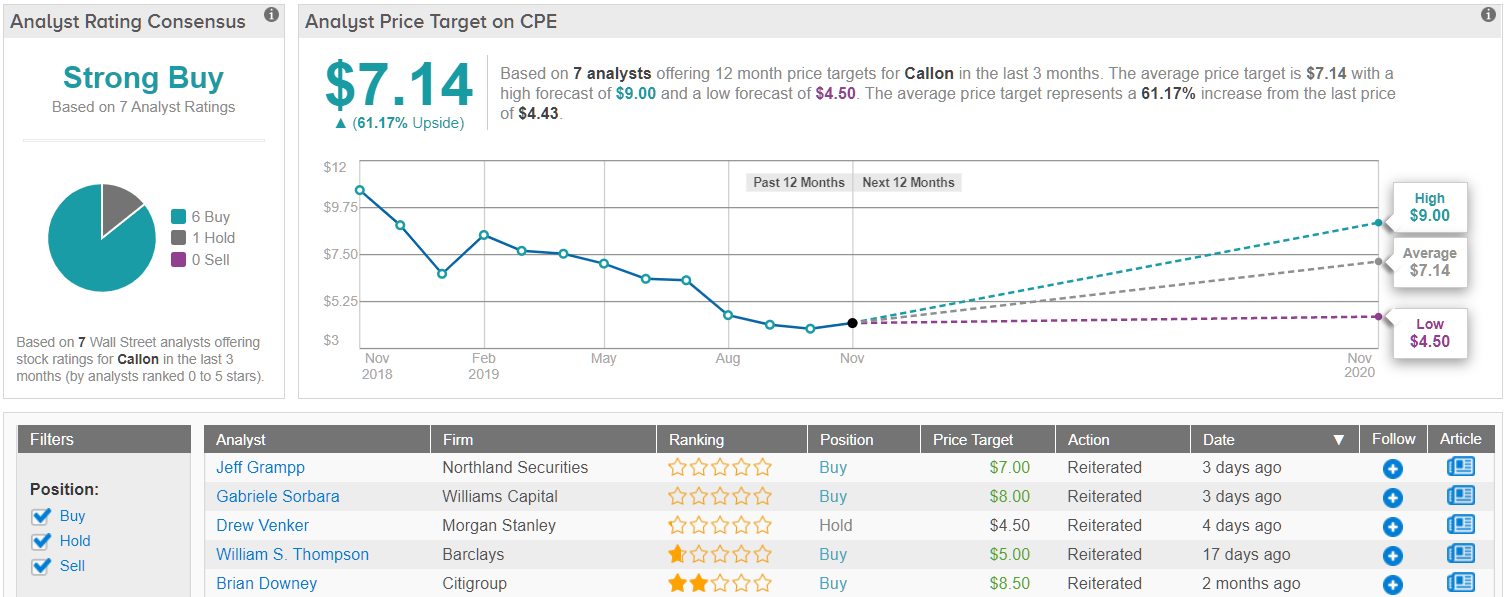

Callon Petroleum (CPE)

Callon Petroleum specializes in the exploration and development of sites in the Permian Basin. Coming on the heels of its third quarter earnings release, several Wall Street analysts think a recovery is on the horizon.

Even though CPE has struggled year-to-date, its efforts in its most recent quarter to drive a turnaround haven’t gone unnoticed by investors. Overall production came in at 37.8 Mboe/d, up 8% year-over-year. In addition, the company saw an operating margin of $35.58 per Boe.

It doesn’t hurt that CPE was able to cut operational capital spending by 13%, with this figure landing at $116.4 million. This allowed it to maintain full year capital targets even though management had originally lowered the guidance range.

“Our successful mega-pad development projects are not only generating significant and durable cost savings but have exhibited solid productivity. In addition, the continued efforts to optimize previously acquired assets have resulted in incremental value to shareholders as our team has made noteworthy progress on well productivity and operational costs across our expanded asset base,” CEO Joe Gatto stated.

These developments have led Citigroup analyst Brian Downey to believe that CPE looks like a long-term winner. Despite reducing the price target from $10 to $8.50, he still sees a potential twelve month gain of 101%. (To watch Downey’s track record, click here)

Looking at the consensus breakdown, Wall Street takes a bullish stance on CPE. 6 Buys and 1 Hold issued over the previous three months make the stock a ‘Strong Buy.’ It should also be noted that its $7.14 average stock-price forecast suggests 61% upside from the current share price. (See Callon stock analysis on TipRanks)