10 is a majestic number. Used to bestow a quality of unmatched excellence, be it as a score in a gymnastics routine, or as a number on the back of a sportsman/woman’s shirt, indicating leadership and guru-like status.

TipRanks makes good use of the aspirational number too. The Smart Score tool combines 8 key metrics that can indicate a stock’s long-term growth potential. The data is analyzed, and the stock is given a score accordingly. The highest score, naturally, is a “Perfect 10”.

Setting out on our quest for perfection, with the Smart Score’s assistance, we homed in on 3 Perfect 10 Stocks with plenty of room for growth ahead. Let’s take a look.

Yeti Holdings (YETI)

Unicorn brands are a rare sight; hence they’re called – you guessed it – unicorn brands. The title refers to a privately held company that reaches a value of $1 billion. One such brand making quite a splash since going public is Yeti Holdings.

The outdoor product manufacturer held its IPO in October 2018 and has mostly been on a cool upward trend ever since. It has made excellent progress in building its brand identity, seducing lovers of the outdoor lifestyle with its varied line of products. As a result, it now boasts 1.3 million followers on Instagram.

Following previous strong quarters, 3Q continued the trend. Sales came in at $229M beating the $222M estimate, alongside increasing sales growth. Yeti delivered on EPS too – at $0.30 it beat the Street’s estimate of $0.26.

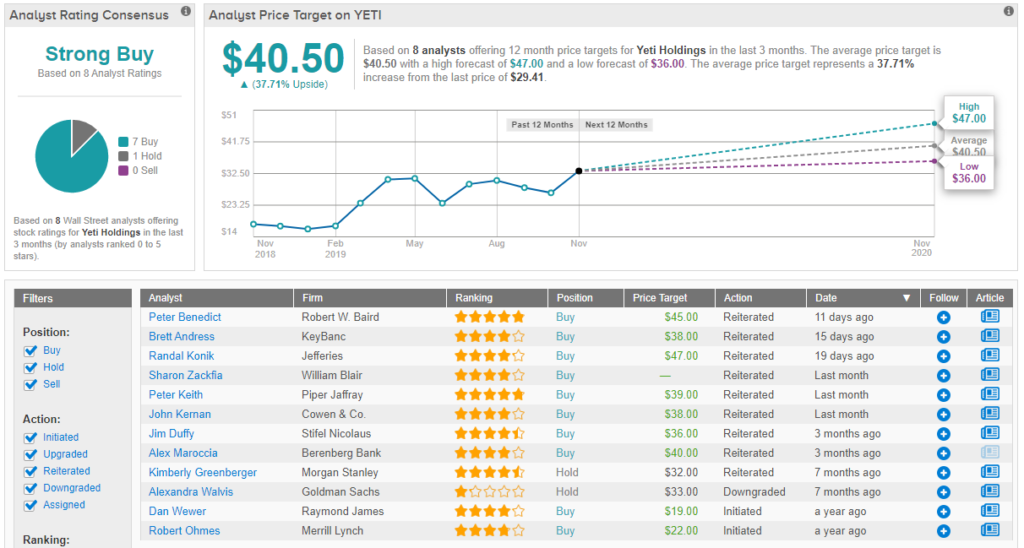

Looking ahead, Jefferies’ 4-star analyst Randal Konik thinks the growth is set to continue, noting, “YETI is a brand that consumers (Pros/ Joes) love & also see as a gifting destination.” He adds, “We see significant opportunity for YETI to expand its TAM as it broadens its exposure to non-heritage markets in the US and international over the long-term. With continuous innovation in new and existing product categories, and a quickly growing margin-enhancing DTC channel, we believe top-line and margin opportunities are significant.”

On the back of his analysis, Konik reiterated a Buy rating on Yeti, with a price target of $47.00, providing potential upside of almost 60%. (To watch Konik’s track record, click here)

Another analyst singing YETI’s praises is Piper Jaffrey’s Peter Keith, who said, “Business momentum remains strong and we see upside to implied Q4 guidance. Importantly, we believe YETI is demonstrating longer-term growth potential, considering success with new product launches, steady/consistent gross margin expansion, intriguing store expansion opportunity both w/ Wholesale and DTC, and engaging marketing.” Like Konik, Keith reiterated a Buy on the stock, with a price target of $39.00. (To watch Keith’s track record, click here)

The analysts’ positive sentiment is shared by the Street, as Yeti currently ranks as a Strong Buy. The cooler manufacturer has a consensus of 7 Buys and 1 Hold with an average price target of $40.50. This implies handsome potential upside of over 37% from its current price of $29.41. (See Yeti stock analysis on TipRanks)

CryoPort (CYRX)

With a motto of “Science. Logistics. Certainty.” CryoPort, which provides cold chain logistics solutions to the life sciences industry, presents itself boldly.

In layman’s terms, it is a frozen shipping container company moving biological specimens around the world in sub-zero temperatures. Its clients include biopharmaceutical, IVF and surrogacy as well as animal health organizations across the globe.

The company recently posted strong 3Q19 results, with revenue up 81% year-over-year, and positive adj. EBITDA for the second consecutive quarter. Among the highlights in the report were increased market share in the regenerative medicine clinical trial sector and a strategic partnership with Lonza. Lonza provides product development services to the pharmaceutical and biologic industries and is considered one of the largest players in the field.

Needham’s 4-star analyst Stephen Unger thinks the partnership is good news for CryoPort, noting, “The goal of the partnership is to provide customers developing cell and gene therapies with a fully integrated solution for outsourced manufacturing and cold-chain logistics, which we see increasing customer visibility of CYRX’s best-in-class logistics solutions earlier in the therapy development process.” Following the quarterly report and positive developments, Unger maintained his Buy rating on CYRX. His price target is $24.00. (To watch Unger’s track record, click here)

B.Riley FBR’s Andrew D’Silva is also impressed with the partnership. The analyst said, “We believe Lonza has positioned itself as one of the cell and gene therapy industry’s leading contract development and manufacturing organizations (CDMOs). As a result, we believe CYRX being selected as Lonza’s preferred partner is another substantial validation for the company and should help further increase CYRX’s logistics volumes.”

To this end, D’Silva reiterated his Buy rating on CYRX stock, along with a price target of $26.00, providing potential upside of 70%. (To watch D’Silva’s track record, click here)

Not many analysts have presently weighed in on the small cap’s potential for the year ahead. With a consensus of 2 Buys, CYRX currently ranks as a Moderate Buy. That being said, the average price target is $25.00, implying nice upside of almost 64% from its current price of $15.56. (See Cryoport stock analysis on TipRanks)

Sonos (SONO)

Speakers act louder than words, so the phrase goes. Well, not quite, but it does lead us nicely to our final choice.

Consumer electronics company Sonos is mostly known for its smart speakers. Apart from the excellent sound quality, Sonos’ Sonoset system creates a custom Wi-Fi network, eliminating the need for old fashioned wires and allowing for music to be played simultaneously in different rooms.

This is great for household systems, and earlier this year Sonos partnered with furniture giant Ikea on a new line of products, an alliance RBC Capital’s Robert Muller thinks has the potential to drive new customer adoption.

The analyst said, “We believe the true value of Sonos lies in the family ecosystem whereby additional speakers complement one another. Once exposed to Sonos, we expect new customers to quickly envision the benefits of additional speakers throughout their homes. If SONO is able to expand the number of homes it’s in (currently in ~8MM worldwide with nearly 4MM in the US), we should see a wave of secondary purchases.”

Emphasizing this thesis, Muller says almost 4 out of 10 new purchases are from existing Sonos customers. Furthermore, the analyst also views SONO as a potential acquisition target for one of the tech giants, adding, “We do not believe current valuation adequately captures acquisition potential, expansion opportunities, or current baseline growth”. Following his analysis, Muller initiated coverage, along with a price target of $18.00. (To watch Muller’s track record, click here).

A consensus rating of 3 Buys and 1 Hold means the Street is ready to turn the volume up on Sonos, rating the speaker manufacturer as a Strong Buy. The average price target is $18.25, providing upside of 24% from its current price of $14.70. (See Sonos stock analysis on TipRanks)