There are thousands of companies traded on the world’s stock exchanges – 2,800 on the NYSE alone. Making sense of the constant data flow, the ebbs and tides of the stock prices and positions, is a challenge even for the most experienced investors. This is where the indexes come in. They aggregate smaller numbers of stocks, and distill the price movements into a single number. One of the most important of the indexes, covering most of the market’s largest companies, is the S&P 500.

As the name indicates, there are some 500 companies in the S&P index, but together they hold over 80% of the US stock market’s total value. The five largest publicly traded companies, counting by market cap, are all indexed by the S&P. Taken together, Apple, Microsoft, Amazon, Alphabet, and Facebook are worth almost $4.7 trillion – roughly as much as the GDP of Japan, the world’s third-largest economy. So, the S&P 500 tracks the macro moves of the stock markets.

Today’s market climate, however, doesn’t necessarily push investors toward the big companies. Bond yields are low, below 2%, and the US Federal Reserve has pushed its key rate down to the 1.5% to 1.75% range. In Europe, some sovereign bonds are actually yielding negative rates. In this climate, investors are naturally drawn to stocks – but especially toward dividend stocks.

The average dividend yield among S&P listed companies is only 2%, but that still beats bonds. And what about the five largest companies mentioned above? Amazon, Alphabet, and Facebook don’t offer any dividend, while Apple and Microsoft pay dividends yielding significantly less than 1.5%. So, income-minded investors will naturally be drawn to the smaller side of the S&P 500.

We’ve customized the filters setting on the TipRanks Stock Screener tool to match this strategy. Setting them to sort out stocks with very high dividend yields, high upside potential, or a high Smart Score – an aggregated measure of TipRanks’ data – gave us three stocks that are sure to spark your interest.

Occidental Petroleum (OXY)

Occidental Petroleum is a $30 billion player in the energy industry. The company has exploration and drilling operation, for oil and natural gas, across the United States, in Colombia, and in the Middle East. The company is also heavily invested in the petrochemical manufacturing industry, with manufacturing facilities across the United States.

The scope of Occidental’s operations can be seen from the company’s revenues. In calendar year 2018, Occidental brought in $17.8 billion, and saw a net income of $4.1 billion. Low oil prices in the past year have hurt the company, however, and the stock is down significantly this year. In Q3, reported at the beginning of November, OXY missed the forecasts by a wide margin. Earnings were negatively impacted by the company’s $38 billion purchase of competitor Anadarko Petroleum.

OXY showed a net loss of $912 million in the third quarter, down from a $1.78 billion profit the year before. Production was up, at 1.16 million barrels of oil and gas sold, but the declining prices meant that the average selling price was $56.26, down $6 from Q3 2018. The combination of pressures on OXY has pushed the stock down 38% this year, and has led the company to announce a 40% spending cut for 2020.

Through all of this, Occidental has not only maintained its dividend, it has raised the payment. The current $3.16 annual payout comes to quarterly checks of 79 cents per share, and an impressive yield of 8.3%. OXY raised the dividend in mid-2019, the third increase since 2017. The company has an 11-year history of dividend growth.

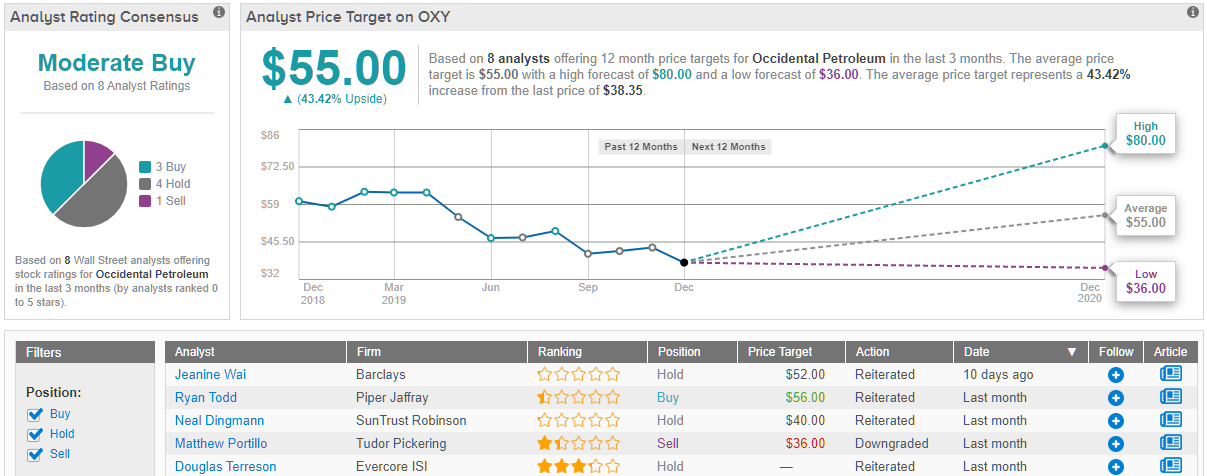

OXY has had some thumbs-up from the analyst recently. Susquehanna’s Biju Perincheril said of the stock, “With further refinement of cost assumptions on a de-consolidated basis, we estimate OXY could generate at least $800-$900 million in free cash flow (de-consolidated basis, but including WES distributions) after funding its dividend obligations next year. In 2021, the excess could be close to $1.5 B.” Perincheril believes that OXY is trading at a discount. His Buy rating comes with a $55 price target, suggesting a 45% upside to the stock. (To watch Perincheril’s track record, click here)

Also bullish is Scotiabank’s 4-star analyst Paul Cheng. Cheng went into detail on the stock, writing, “As expected, OXY’s 3Q19 earnings release was messy… On the positive side, we fully agree with company’s decision to pare back spending in 2020 and now estimate 1) a small 2020 standalone free cash flow… and 2) a year-end 2020 net debt balance ~$2bn below our prior forecast. We also view the underlying 2020 capital and production assumptions as reasonable. Finally, we believe operating performance was strong across most of OXY’s core areas…” Cheng gives OXY a $53 price target and a Buy rating. His target implies an upside of 40%, suggesting that he sees the stock as undervalued. (To watch Cheng’s track record, click here)

Overall, OXY gets a Moderate Buy from the analyst consensus, based on 3 Buy, 4 Hold, and 1 Sell ratings set in the last quarter. OXY shares sell for $37.71, and the $55 average price target implies a premium of 45% from that price. (See Occidental Petroleum’s stock analysis on TipRanks)

Macerich Company (MAC)

Real estate investment trusts are well known for their high dividends. These companies are formed to buy and manage residential and commercial property, and US tax law requires that they return the bulk of their earnings to shareholders. They comply primarily through high dividend yields, and it’s not uncommon to find REITs with payout ratios exceeding 100%.

Macerich is an REIT focused on commercial properties, and it is the third-largest owner-operator of shopping center space in the US. Macerich’s 53 properties exceed 50 million square feet in total area, and are profitable. For Q3, reported at the end of October, Macerich showed an EPS of 33 cents per share based on a net profit of $46.37 million. This was down 36% from the year-ago quarter, reflecting the difficulties facing brick and mortar retailers in the US.

As mentioned above, REITs are required by law to pay out a high dividend; Macerich’s quarterly payment of 75 cents meets this requirement. The annualized dividend of $3 makes the yield 11.52%, almost 6 times the S&P average, and the company has been raised the payment twice since 2017. With its high cash flow based on reliable property leases, Macerich has been able to sustain a high payout ratio of 85%.

Wall Street has an evenly divided stance of MAC stock. On the bullish side is Evercore analyst Samir Khanal, who gives the stock a Buy rating and a $40 price target. Khanal wrote, after the company reported the Q3 earnings, “While we fully recognize that the retail leasing environment remains under pressure in the near-term, we believe many of the short-term headwinds are priced into MAC’s stock price today and the risk/reward remains compelling over the next 12 to 18 months especially as the company remains highly focused on reducing leverage and backfilling vacancy or converting temp tenants into permanent occupancy.”

Khanal’s $40 price target indicates confidence in the stock and a potential upside of 53%, in line with his buying stance. (To see Khanal’s track record, click here)

Overall, MAC gets a Moderate Buy rating from the analyst consensus, with one Buy and one Hold review set in recent weeks. Shares sell for a low price, $26.27, making this an easy stock to enter for speculation, and the $36.50 average price target suggests a high upside of 40%. (See Macerich’s stock-price forecast and analyst ratings)

Invesco, Ltd. (IVZ)

With a market cap of $8 billion, Invesco is one of the smaller companies in the S&P listing. Small size, however, doesn’t translate to small status – Invesco is an important player in the financial services industry. The stock has been volatile in 2019, however, making investors wary. But is that wariness warranted?

First off, despite the volatility of IVZ shares (they have varied between $21 and $14 this year, a shift of 33%), the stock is up by 5.25% in 2019 – and much of that gain has come in the final quarter. In the most recent earnings report, for Q3, the company showed an EPS of 70 cents, beating the forecast of 57 cents by a wide margin, and beating the year-ago number by 4 cents. Revenues, reported at $1.72 billion, just missed the estimates, but were substantially higher year-over-year. It was an upbeat quarter, and shares rose accordingly after the report.

For dividend investors, Invesco offers some clear advantages. The quarterly payment, of 31 cents, annualizes to $1.24 per share, making the yield a strong 7.04%. Even better, the company has been growing its dividend for the last 10 years, showing a commitment to rewarding shareholders. And finally, the payout ratio, the comparison of the dividend to the quarterly earnings, is only 48%, indicating that it is easily sustainable for the long term.

A typical bullish analyst review comes from Kenneth Lee, of RBC Capital. The 4-star analyst reiterated his Buy rating after the quarterly reports, writing, “We continue to favor IVZ given its depth of capability and well-diversified asset mix, spanning smart beta ETFs, actively managed products, to alternative investment strategies. Further, Invesco is making significant investments… further broadening its investment capabilities within attractive categories. We think the company [is well positioned] to potentially achieve above-peer-average organic growth rates.”

Lee put a $22 price target on IVZ shares, implying an upside of 24% to the stock. (To watch Lee’s track record, click here.)

Invesco holds a TipRanks Smart Score of 9, indicating a strong likelihood that IVZ will outperform in the coming year. Among the stock’s strengths are a bullish news and blogger sentiments, as well as positive investor sentiment. This last is based on increased purchase activity in the last 7 to 30 days.

To find good ideas for dividend stocks trading at fair value or better, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.