Investment bank Needham has done investors a solid favor, making it easier to sort out the nuggets from the pebbles. For background, the S&P 500 is back to record levels, after volatile trading in recent weeks. A combination of factors, including President Trump’s Senate acquittal, an excellent January jobs report, and the constant leak of medical news from China giving a window to the Coronavirus epidemic, have all buffeted the markets. But it looks now like investors are back to the optimism, driving the exchanges to record after record.

Of course, not every stock rises steeply, even when the market as a whole does, and that’s where Needham’s recent spate of stock reports comes in. The firm employs a cadre of top analysts who monitor the markets and crunch the numbers, following stocks to see which will lead the gains.

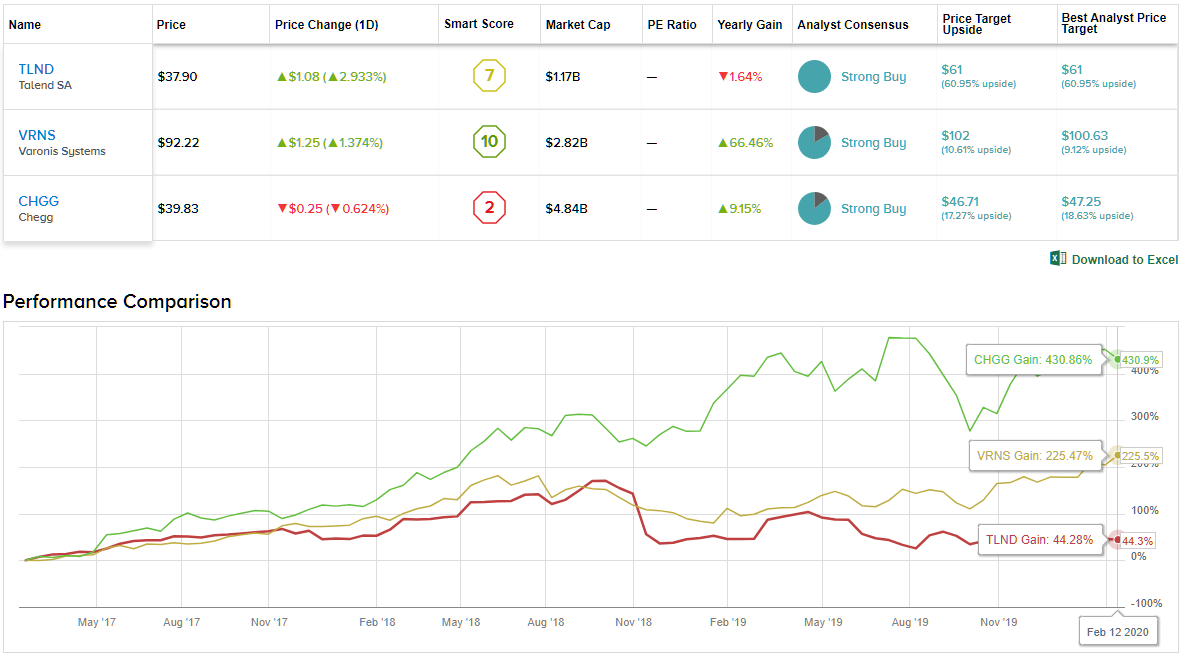

This week, three 5-star analysts have published their notes on three small- to mid-cap companies in the software tech sector. We’ve pulled the reports and looked at the stocks through the lens of the Stock Comparison tool, to find out what makes them special. Let’s dive in.

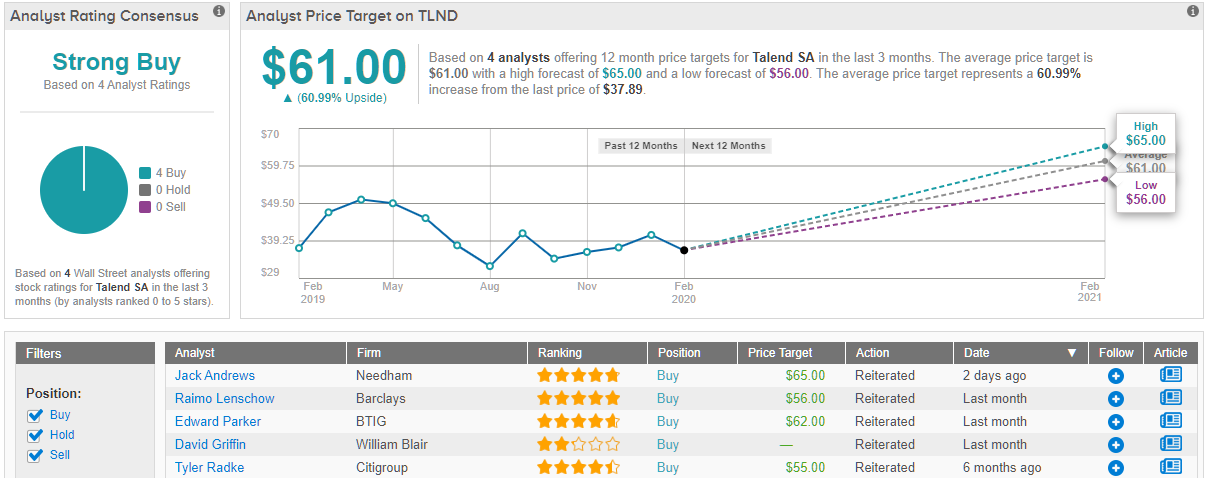

Talend SA (TLND)

We’ll start with Talend, a company offering an open-source integration and synchronization software packages. The company’s products are designed to make owning open source systems easy. Talend’s software packages solve common problems of cost, development, and learning involved in commercial use of open platforms.

Talend most recent quarterly report showed rising results. The company has been trimming its net loss, and reported a loss of 8 cents against the 23-cent loss forecast. It was an impressive 15-cent beat, or 65%. The revenue beat was more modest, but the $62.6 million reported was a 20% year-over-year gain.

Looking forward, TLND has guided revenue higher than the consensus estimates, with company management predicting $66.5 to $67 million in total sales for the quarter. The company will report Q4 2019 earnings today after trading hours; the release is scheduled for midnight, so investors will have wait until Friday to see how the numbers hold up.

5-star Needham analyst Jack Andrews believes the Q4 news will be good, in line with the best-case possibilities. In his note on the stocks, he writes, “There are 5 reasons why we are positive: 1) Pending disclosures on the cloud business should provide visibility and improve sentiment; 2) Migrations from on-premise to the cloud should result in upsell opportunities; 3) Leverage to rapid growth of cloud data warehouses; 4) FX headwinds should abate; and 5) Discounted valuation creates a favorable risk/reward setup.”

Andrews buttresses his Buy rating on TLND with a $65 price target, indicating confidence in a 72% upside potential. (To watch Andrews’ track record, click here)

Overall, Wall Street appears to agree with Andrews on this one. TLND shares have 4 recent Buy reviews, making for a unanimous Strong Buy consensus rating. Shares are priced at $37.87, and the average price target, $61, suggests a strong upside of 61%. (See Talend stock analysis on TipRanks)

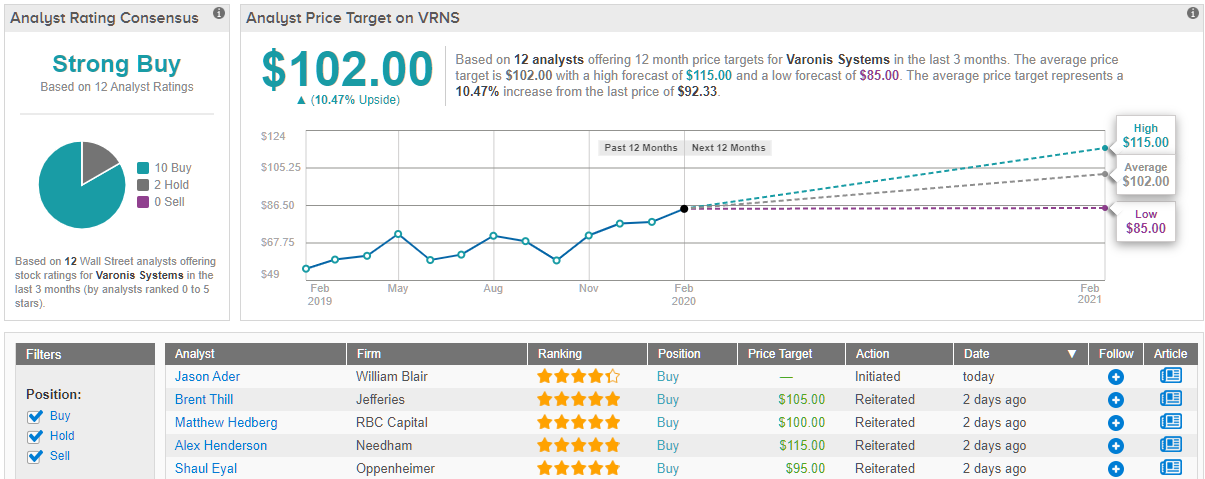

Varonis Systems (VRNS)

Second on our list is Varonis Systems, a data security software company. Varonis’ products are data management systems, for managing, organizing, and protecting unstructured and semi-structured data environments. Business data, including documents, media files, presentations, and spreadsheets are all targeted by Varonis’ data security solutions.

A quick measure of the company’s success is the share appreciation — over the past 12 months, VRNS shares have gained 46%.

Earlier this week, VRNS reported Q4 2019 earnings, and the results were in line with expectations. The company frequently operates a net loss, common among cutting edge tech start-ups, but the loss of 9 cents per share compared favorably to the 10 cents expected. Revenues were down year-over-year, but at $72.56 million the top line also beat the quarterly forecast. It was the third quarter of the last four that VRNS has exceeded expectations on quarterly results.

5-star Alex Henderson, who reviewed this company for Needham, sees Varonis staking out a clear, and profitable, niche in data security, He wrote, after the Q4 release, “Varonis called out data growth, cloud growth, and privacy legislation as key drivers for data protection and security, We think laws like GDPR and CCPA continue to drive interest in Varonis, and while these customers are originally motivated by the ability to classify protected data, they are adding to the upsell pipeline as they see value in other Varonis solutions.”

Supporting his Buy thesis, Henderson gave the stock a $115 price target, implying room for 25% upside growth. (To watch Henderson’s track record, click here)

Overall, Varonis’ Strong Buy analyst consensus rating is based on 10 reviews, including 9 Buys against a single Hold. All nine of those Buy-side analysts published their ratings on the stock in the wake of the Q4 earnings report. The average price target, $102, suggest an upside of 10% compared to the $92.59 current share price. This is a bit more conservative compared to Henderson’s bullish target above. (See Varonis stock analysis at TipRanks)

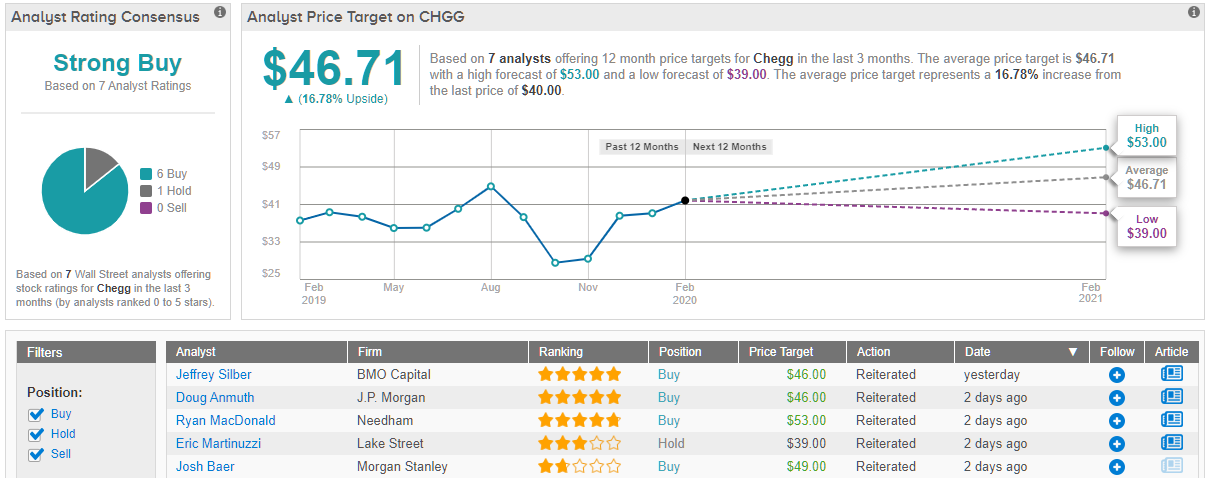

Chegg, Inc. (CHGG)

Last on our list today is Chegg, an interesting twist on the educational software niche. Chegg provides online rental for textbooks, as well as flash cards, study guides, writing guides, and online tutors. The company is aggressive about expanding through acquisition, and in the last two years purchased two competitors: WriteLab was acquired for $15 million and Thinkful was bought for $80 million.

Since mid-2018, Chegg has consistently beaten analyst forecasts on earnings, and CHGG shares gained 29%, matching the S&P 500, over the past 12 months. The company’s Q4 earnings, just released, chalked up another win in that record.

For Q4 2019, CHGG reported a 35-cent EPS, 17% above the estimate, and top-line revenues of $125.5 million. The revenue beat was only 1.9%, but it did gain 34% year-over-year – an impressive performance.

Needham’s Ryan MacDonald, a 5-star analyst, gave Chegg a $53 price target and a Buy rating, based on the company’s steady gains. His target suggests an upside of 33% for the stock.

In his comments on CHGG, MacDonald writes of the forward prospects, “[We] are increasingly optimistic regarding the multiple initiatives to sustain heightened levels of subscriber growth. This includes a larger than expected opportunity internationally, continued strength in domestic demand, and a contribution from Thinkful.” (To watch MacDonald’s track record, click here)

The analyst consensus on Chegg shares, another Strong Buy, is based on 6 reviews, which include 5 Buys against a single Hold. The share price is $40, while the average price target of $46.71 indicates room for 17% upside. MacDonald, quoted above, takes a more bullish stand here. (See Chegg’s stock analysis at TipRanks)