It’s another day on the stock market roller coaster, with the S&P 500 starting off the second-quarter in the negative.

If you don’t think that you can correctly call the bottom in a deep bear market, don’t worry. So far, that crystal ball hasn’t been invented. But if you can get a clear snapshot of current conditions, you may be able to set up a profitable trading strategy no matter what the broader market is doing.

This all just brings us back to the question: how do you find investment-grade stocks in a volatile market? There isn’t one sure answer; plenty of investment strategies can steer you toward profits. But there is one possibility that might make investing easier – just follow the insiders.

Insiders – the corporate officers, board members, and others ‘in the know’ – don’t just manage the companies, they know the details. Legally, they are not supposed to trade that knowledge, or to blatantly trade on it, and disclosure rules by government regulators help to keep the insiders honest. Their honest stock transactions, however, can be highly informative. These are the people with the deepest knowledge of particular stocks. So, when they buy or sell, especially in bulk, take note!

TipRanks has the tools to help you do just that. The Insiders’ Hot Stocks page shows which stocks top insiders are most active on, for both purchases and sales. You can sort insider trades by a variety of filters, including trading strategy. We’ve done some of the legwork for you, and pulled up three stocks with recent informative buy-side transactions. Here are the results.

Prosperity Bancshares (PB)

We’ll start in the financial sector, with a mid-cap bank holding company. Prosperity Bancshares is the owner/operator of Prosperity Bank, a regional bank with 285 branches in Texas and Oklahoma. Prosperity ended 2019 on a high note, with strong Q4 results after concluding a merger with Legacy Texas Financial Group, a move that gave the bank an additional 42 branches in the northeastern part of the state.

The insider sentiment on PB is strongly positive, as three company officers have used the stock’s low price to pick up large blocks of shares in recent days. The two largest purchases came from David Zalman, Senior Chairman and CEO, who laid down $650,000 for some 15,000 shares, and from H. E. Timanus, Chairman, who paid $215,000 for 5,000 shares. These two purchases are part of a larger run of insider buys, that have totaled almost $4.2 million over the past three months.

In addition to holding a solid financial position, Prosperity also pays out a reliable dividend. The company has a 17-year history of maintaining the payments, and has raised the quarterly payout three times in the past three years. The current dividend, at 46 cents quarterly, annualizes to $1.84 and gives a yield of 3.73%. This compares favorably to the 2% yield average among S&P listed companies.

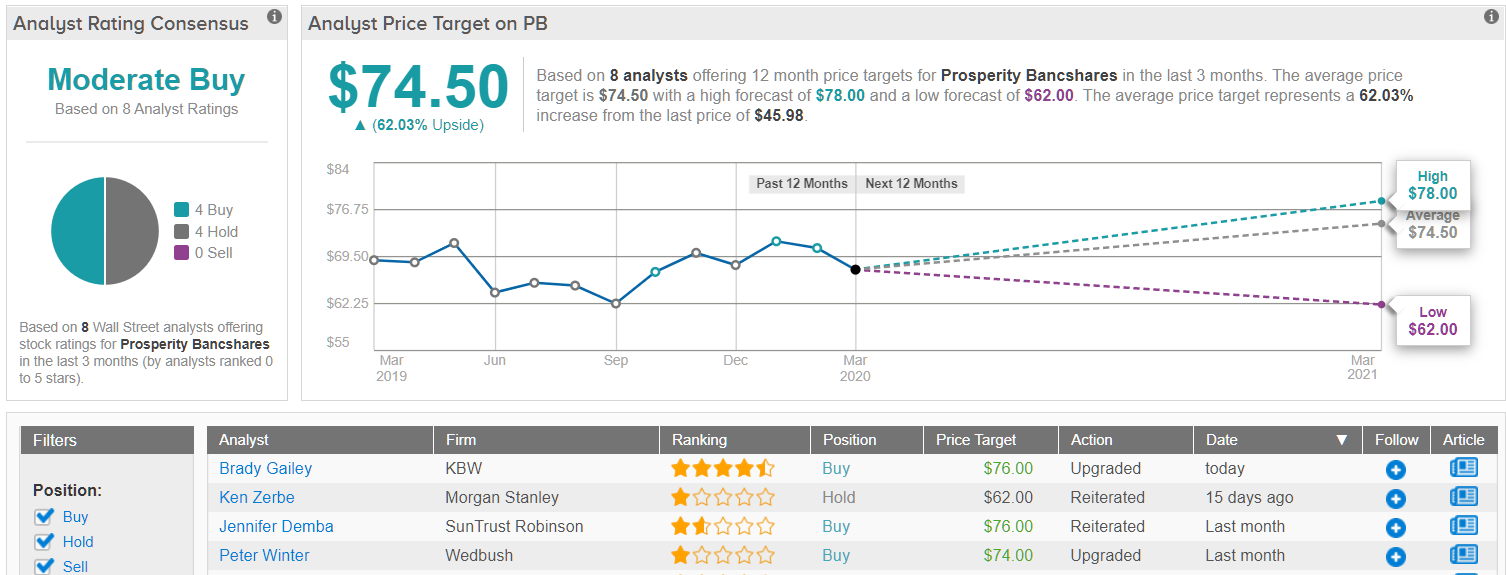

Covering this stock for Wedbush, analyst Peter Winter likes what he sees and upgrades his stance on the shares from Neutral to Buy. Supporting his view, Winter writes, “PB is a flight to quality bank in times of stress and we believe its acquisition of Legacy Texas will be more accretive than originally projected, offsetting potential margin pressures from the precipitous drop in rates and potentially much weaker economy. PB has consistently maintained some of the best credit metrics in banking through many economic cycles.”

Winter gives PB a $74 price target, suggesting an upside of 61%. (To watch Winter’s track record, click here)

Also upbeat here is SunTrust Robinson analyst Jennifer Demba. She particularly likes the bank’s long history of strong credit and smart acquisitions: “PB has proven itself to be a credit safe-haven over the past 20 years… we think PB should be an outsized beneficiary of a more challenging fundamental environment for the banks given it is a proven, experienced and disciplined bank acquirer.” Demba’s reiterated a Buy rating on PB shares, which is backed by $76 price target — a bullish 65% upside potential. (To watch Demba’s track record, click here)

All in all, Prosperity gets a Moderate Buy rating from the analyst consensus, as it has 4 Buys and 4 Holds in its most recent reviews. Shares are selling for just $46.09, and the average price target of $74.50 indicates an upside potential of 62% for the coming 12 months. (See Prosperity stock analysis on TipRanks.)

GMS, Inc. (GMS)

The next stock on our list is from the construction industry, which had been doing well in 2019 only to face a serious hit during the coronavirus lockdowns. Long-term, however, that hit may just provide investors with a low-cost point of entry now for companies like GMS.

This company, whose initials stand for Gypsum Management and Supply, is a provider of wallboard, dropped ceiling systems, steel framing, and other interior construction materials. GMS is a major supplier for homebuilders and contractors in the US, and boasts a market cap of $661 million.

Turning to the insider activity, we find that company Director Ronald Ross has made two large purchases, totaling 189,800 shares. His purchases cost a combined $2.5 million. Also making an informative buy was David Smith, another director of the company. He spent $36,270 to pick up 3,000 shares, in another move made last week. These purchases indicate a high level of confidence in the company, by company officers.

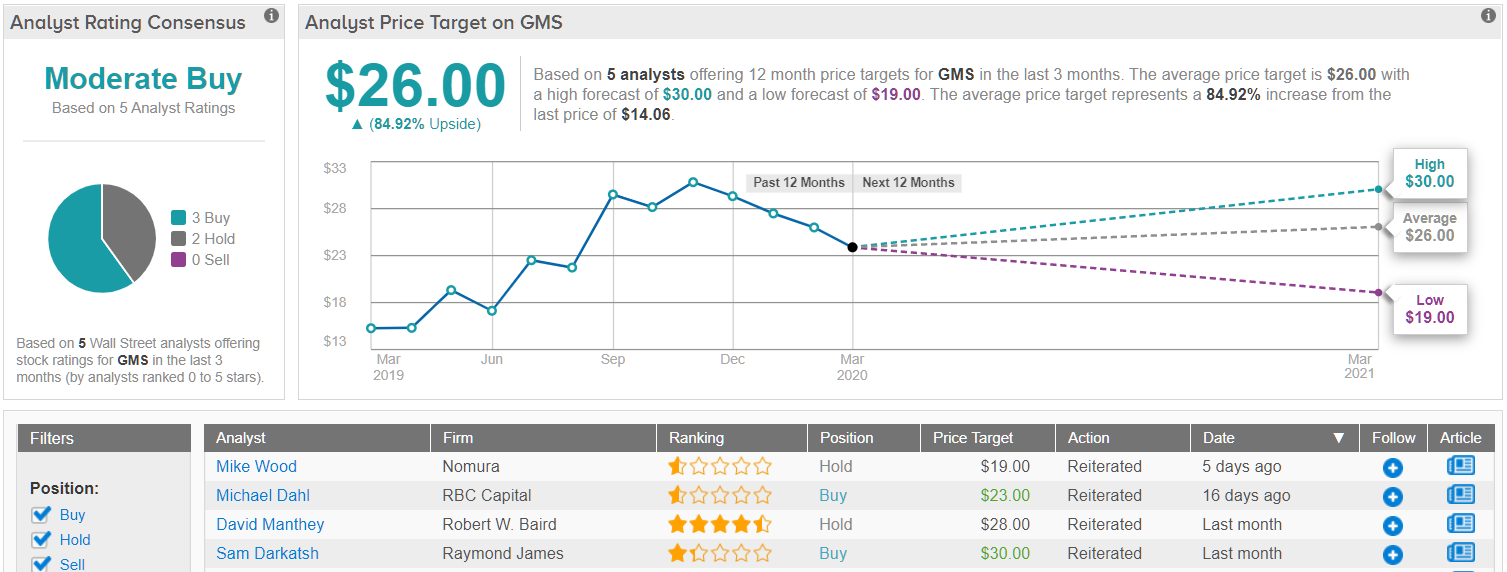

The insiders’ confidence is shared by two Wall Street analysts who reviewed this stock in early March. SunTrust Robinson analyst Keith Hughes maintained his Buy rating, and backed it with a $33 price target that suggests a 135% upside potential. (To watch Hughes’ track record, click here)

In his comments, Hughes noted some positive points from the earnings release: “GMS reported a ~90 bps increase in gross profit margin due to price/cost dynamics, mix and synergies. Good wallboard volume helped mix but was aided by a higher percentage of commercial work.” He added, at his own bottom line, “We look for GMS to continue to increase its market share, both organically and through acquisitions.”

Trey Grooms, from Stephens, also puts a Buy rating on the stock, saying, “Looking forward, mgmt. see signs of stabilization in Canada. Commercial activity was robust and the outlook has improved since last quarter. Residential remains promising and GMS’ focus on Other Products should support top-line growth… with guidance that appears achievable, an improved end-market outlook with opportunity for price inflation, and a current valuation below the historic range…” Grooms gives GMS a $30 price target, implying an upside of 113%. (To watch Grooms’ track record, click here)

Overall, the Moderate Buy analyst consensus rating on GMS is supported by 3 Buys and 2 Holds set in recent weeks. The stock is priced at a discount, $14.06, and the $26 average price target suggests a potential upside of 85%. (See GMS’ stock analysis on TipRanks)

Accelerate Diagnostics (AXDX)

Our final stock on the list is from the medical tech sector. Accelerate develops diagnostic systems for healthcare providers on the global market, for the identification and treatment of bacterial infections. In short, AXDX offers new technology for medical labs, allowing them to speed up the testing process and get results to clinicians and patients faster, promoting better medical outcomes.

Looking at the insider purchases, we find that Jack Schuler, member of the Board of Directors and a 10% owner in the company, made two informative purchases in recent days, totaling 322,900 shares. Schuler spent $2.17 million on that purchase, a clear sign of confidence.

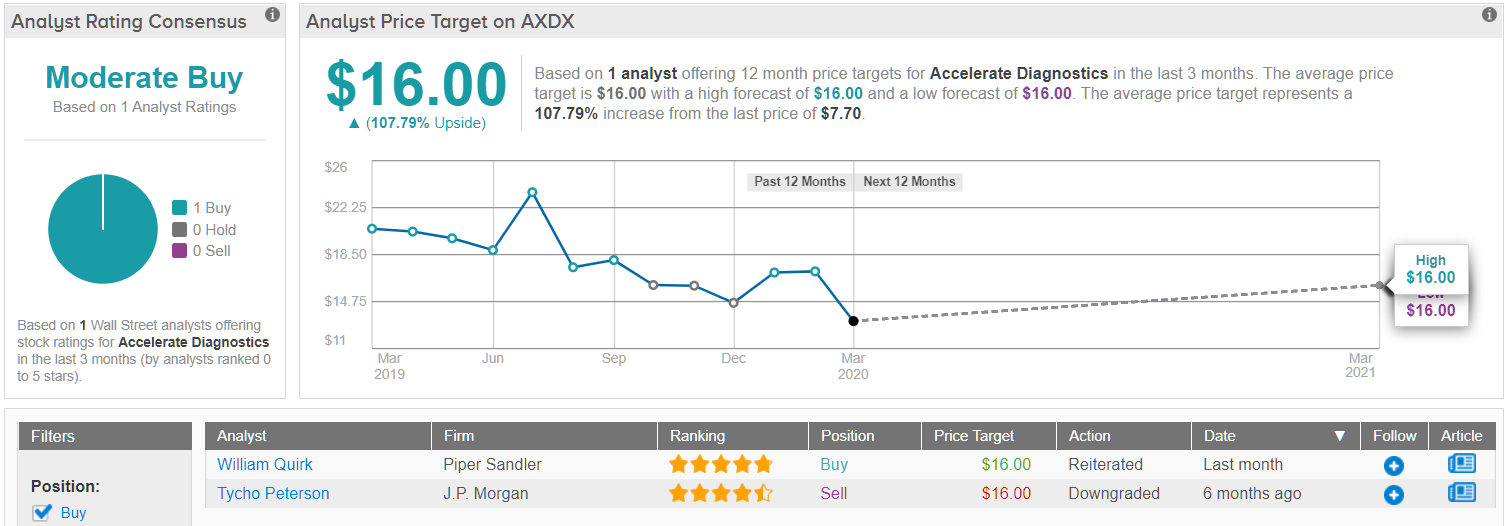

Writing on this stock for Piper Sandler, 5-star analyst William Quirk sees plenty of room for optimism. He gives AXDX a Buy rating, with a $16 price target implying a 109% upside. To watch Quirk’s track record, click here)

In his comments supporting his stance, Quirk wrote, “Accelerate is utilizing clinical data from customers in the selling process to demonstrate cost savings and decreased length of stay. Accelerate also developed an ROI tool to help customers realize the incentives of Pheno. Management was upbeat about both of these tools and said the additional data points have been key for closing deals.”

William Blair analyst Brian Weinstein, also rated 5-stars, sees the COVID-19 pandemic as a long-term net positive for the company. He writes, “…as the dust settles on the pandemic, the company believes this could create additional buy-in from key stakeholders, including hospital executives and government agencies, with respect to how they view and promote rapid diagnostics.” Weinstein gives AXDX a Buy rating, but declines to set a specific price target. (To watch Weinstein’s track record, click here)

Net net, this stock is selling for a modest $8.69 right now, and the average price target of $16 suggests room for an impressive 84% share appreciation. (See Accelerate Diagnostics’ stock analysis at TipRanks)

To find good ideas for biotech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.