Wall Street is experiencing some major déjà vu. The tensions between the U.S. and China flared after President Trump threatened to impose new import tariffs. The difference this time? These tariffs would serve as a punishment for China’s role in the COVID-19 pandemic. In response, stocks posted sharp declines, a rough start to the month of May.

The new week of trading could see more of the same. U.S. stock pointed to losses in Monday’s trading session as statements made by U.S. Secretary of State Mike Pompeo the day before failed to alleviate trade war fears. Going off of the administration’s earlier statements, Pompeo supported the President’s claim that the virus originated in a Wuhan, China laboratory, adding that the country also stocked up on medical supplies while covering up the extent of COVID-19’s spread.

The possibility that a trade war could be reignited has spooked market watchers, but for those looking at the glass half full, there’s a silver lining. Compelling names have seen their share prices driven lower, presenting investors with more attractive entry points. Seasoned Street veterans argue this is particularly true of the biotech space, with this area of the market holding up better than others.

Bearing this in mind, we set out to find exciting yet affordable opportunities within the biotech industry. Using TipRanks’ database, we found three stocks trading for under $10 per share that fit the bill, with each offering up “Strong Buy” consensus ratings from the analyst community and plenty of upside potential. Here’s the full scoop.

Aptinyx (APTX)

Using a differentiated approach that involves modulating the N-methyl-D-aspartate (NMDA) receptor via a unique mechanism rather than switching it on or off, Aptinyx develops cutting-edge therapies for brain and nervous system disorders. Deemed “the comeback kid”, at $2.72 per share, now could be the time to pull the trigger before APTX takes off on an upward trajectory.

This is the opinion of H.C. Wainwright’s Raghuram Selvaraju. The five-star analyst doesn’t dispute that shares have been put through the ringer as of late, but he believes Wall Street has reacted unfairly to non-statistically significant Phase 2 trial results for its lead candidate, NYX-2925, in diabetic neuropathic pain (DPN) early last year.

In fact, Selvaraju cites several reasons for his continued optimism. During the DPN trial, there was clear evidence of NYX-2925’s activity, which was supported by additional proof of efficacy in a separate Phase 2 study in fibromyalgia. Additionally, NYX-2925’s modulation of the N-methyl-D-aspartate (NMDA) receptor is a validated target in the central nervous system (CNS) space. It should be noted that multiple post-hoc analyses on the Phase 2 DPN data were conducted. NYX-2925 is also in a confirmatory Phase 2b trial that incorporates the discoveries from the Phase 2 study, and the current trial is evaluating a single dose vs. Placebo, making it more robustly powered than the earlier trial.

All of this prompted Selvaraju to comment, “From our vantage point, the lack of value being attributed to Aptinyx’s technology platform, lead asset and pipeline provides an intriguing entry point for those investors willing to judge the clinical data on its own merits. We also note the precedent cases of gabapentin and duloxetine, which ultimately achieved market entry in neuropathic pain despite setbacks in DPN trials.”

If that wasn’t enough, Selvaraju sees multiple upcoming clinical data catalysts for not only NYX-2925, but also for its NYX-783 asset and NYX-458 candidate. Speaking to the large market opportunity, he added, “We believe that chronic neuropathic pain—whether embodied by DPN or fibromyalgia—constitutes a poorly addressed condition. Furthermore, the recent opioid crisis has made it well-nigh impossible for physicians to rely on opioid drugs for pain management. Accordingly, there is a burgeoning need for non-opioid, non-addictive analgesic agents that work via novel mechanisms. We note that approximately 8 million individuals in the U.S. alone suffer from DPN, while roughly 5 million suffer from fibromyalgia.”

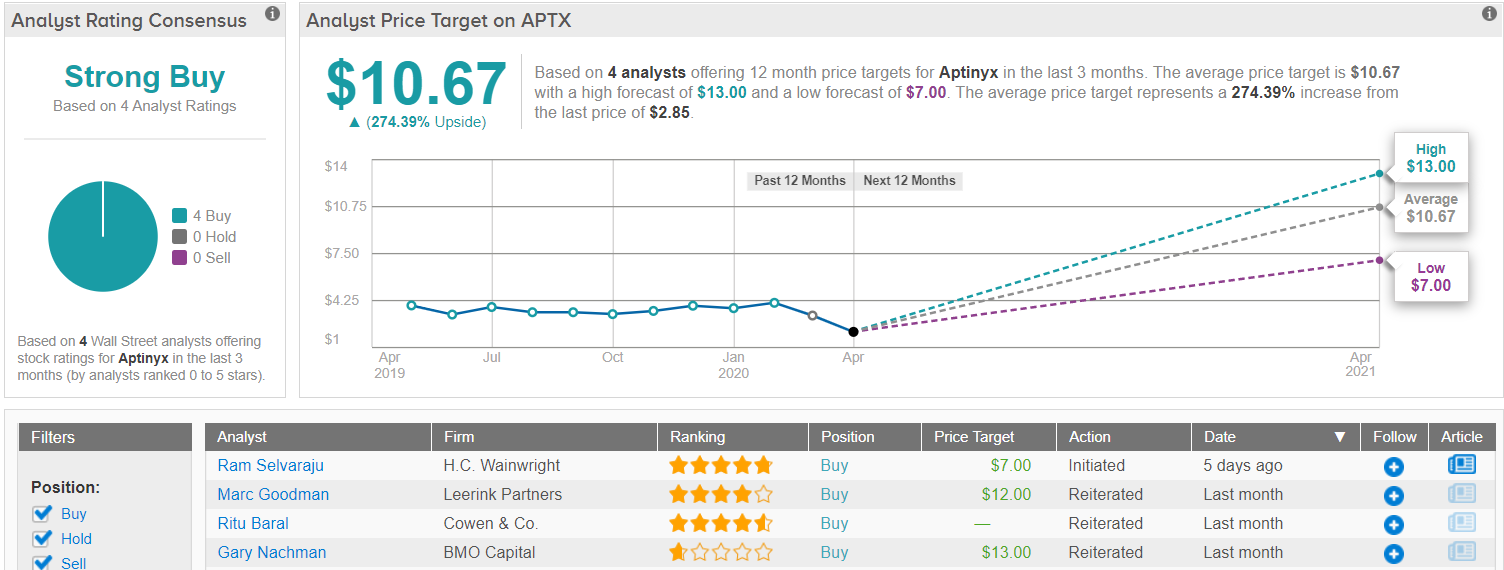

It should come as no surprise, then, that Selvaraju decided to join the bulls. To initiate his APTX coverage, he put a Buy rating and $7 price target on the stock, implying 145% upside potential. (To watch Selvaraju’s track record, click here)

Turning now to the rest of the Street, other analysts agree with Selvaraju. The stock has received only Buy ratings in the last three months, 4 to be exact, so the consensus rating is a Strong Buy. Given the $10.67 average price target, the upside potential comes in at a whopping 274%. (See Aptinyx stock analysis on TipRanks)

Viking Therapeutics (VKTX)

Targeting metabolic and endocrine disorders, Viking Therapeutics’ technology could be a game changer, with it boasting lead candidate, VK2809, an orally available, liver selective thyroid hormone receptor β (TRβ) agonist. Given its vast potential in this area of medicine, several members of the Street believe that at $5.45 apiece, it’s undervalued.

Digging a bit deeper into VKTX’s technology, TRβ agonists are powerful anti-steatotic drugs (reducers of liver fat) that could be capable of reversing NASH and even fibrosis, based on available clinical data. In addition, TRβs are safe and convenient oral drugs that demonstrate efficacy close to the levels seen in injectables with significantly less clear safety windows.

Writing for BTIG, analyst Julian Harrison noted, “Within the TRβ space, we believe VK2809 is positioned to be best-in-class with a favorable mix of potency and tolerability/safety, thanks to calculated prodrug chemistry. Competition from Madrigal’s resmetirom (MGL-3196) has a 2 to 3-year development lead, but in a market of chronic and predominantly asymptomatic disease, safety, tolerability and even ease of administration will matter considerably.”

Expounding on the competition with Madrigal, Harrison points out MGL-3196 doesn’t limit systemic exposure, while VKTX’s VK2809 remains in prodrug form outside the liver. This means that VK2809 can generate truly selective activation in the liver, making the issue of targeting bias a nonissue.

Even though COVID-19 has caused industry-wide delays, twelve-month biopsy data from the Phase 2b trial of VK2809 in patients with biopsy-confirmed NASH shouldn’t face much of a disruption.

“Overall, we view VK2809’s strong clinical data and the enterprise value of only $140 million as a chance for investors to invest in an undervalued asset ahead of de-risked POC readouts,” Harrison concluded.

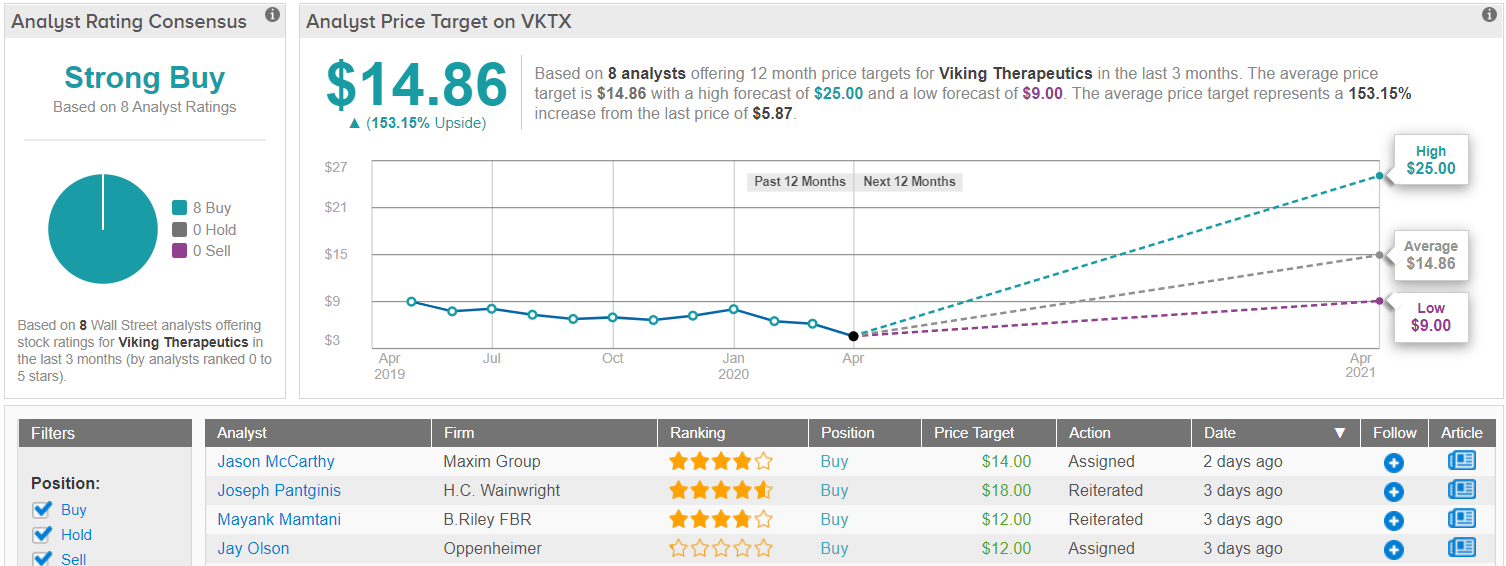

Taking all of this into consideration, Harrison kicked off his VKTX coverage by publishing a Buy rating. The analyst also set a $9 price target, which indicates shares could climb 65% higher in the next year.

Like Harrison, other Wall Street analysts are optimistic about this biotech’s long-term growth prospects. With 8 Buys assigned in the last three months compared to no Holds or Sells, the message is clear: VKTX is a Strong Buy. Should the $14.86 average price target be met, a twelve-month gain of 153% could be in the cards. (See Viking stock analysis on TipRanks)

Mersana Therapeutics (MRSN)

Last but not least we have Mersana, a biotech company that develops antibody-drug conjugates (ADCs) for oncology, with its focus on drug payloads designed to deliver more chemotherapy to the tumors and less to the surrounding tissue, particularly the bone marrow. Ahead of several upcoming data readouts, some analysts believe that its $8.23 per share price tag presents investors with a unique buying opportunity.

Part of the excitement surrounding MRSN is related to its lead program, XMT-1536. The ADC for later-line ovarian cancer (OC) and non-small-cell lung carcinoma (NSCLC) was designed using two innovative technologies that enable it to spur controlled bystander killing, with it specifically targeting NaPi2b, a clinically validated target over-expressed on several important tumor types. It should be noted that XMT-1536 is already progressing through dose-ranging studies and data has demonstrated it is active in platinum-resistant OC and NSCLC adenocarcinomas.

Representing BTIG, five-star analyst Thomas Shrader argues that key data sets, which are scheduled for release in the second half of 2020, could de-risk XMT-1536 in both OC and NSCLC, as well as fuel even more upside by “further validating the Mersana ADC platform and its application in the earlier-stage pipeline.” He added, “The ~33% ORR seen in very late-line NaPi2b-high OC patients (at dose ≥ 30 mg/m2) seems likely to be good enough for accelerated approval and should increase in earlier line patients.”

According to Shrader, the potential of ADCs can be taken one step further. “We believe the future of ADCs may be to replace the chemo component in chemo + IO combinations. In this approach, Mersana’s safety profile seems well placed, as their drugs to date seem particularly gentle on the patient’s bone marrow while clearly showing tumor killing (and corresponding tumor antigen release). Similarly, the newest focus at Mersana, termed iADCs, should drive increased anti-tumor innate immune responses – an area widely considered to be the next leg of IO,” he explained.

When it comes to the balance sheet, MRSN is standing on solid ground. As of Q4 2019, the company had $100 million in cash and cash equivalents, and last month, it exercised its ATM to raise an additional $65 million. This should be enough to support Phase 1 clinical studies of XMT-1536 and Phase 1 dose-expansion studies for its XMT-1592 therapy.

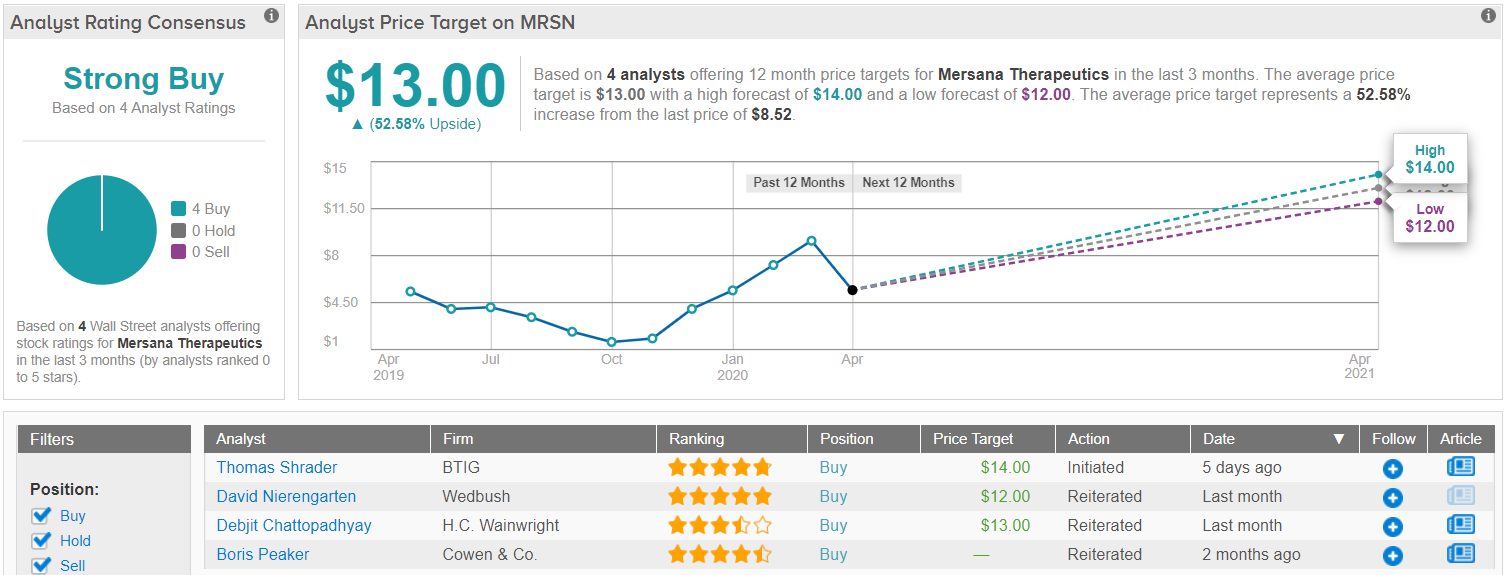

Based on everything MRSN has going for it, it’s no wonder Shrader decided to initiate coverage. Along with a Buy recommendation, he set the price target at $14, suggesting 70% upside potential. (To watch Shrader’s track record, click here)

All in all, other Wall Street pros echo the BTIG analyst’s sentiment. Out of 4 total reviews issued in the last three months, 100% were bullish, making the consensus rating a Strong Buy. The $13 average price target is less aggressive than Shrader’s, but it still leaves room for shares to gain 53% in the next year. (See Mersana stock analysis on TipRanks)

To find good healthcare ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.