Oil may be a necessity in today’s economy, but that doesn’t mean oil prices always go up. In recent years, supply has outpaced demand, putting downward pressure on prices. The fracking revolution in the US oil industry, which opened up previously non-viable or unavailable reserves in shale formations, has turned the US into the world’s largest oil producer and, for now, a net exporter of crude oil products.

The effect on prices has been long-term macro-level volatility. Prices troughed four years ago, in January 2016, climbed steadily to peak in September 2018, and have been unable to regain highs since, in the face of increasing US production and slack global demand. Prices gained 35% last year, bur remain well below their 2018 high.

OPEC, the world’s largest cartel of major oil producers, has announced several production cuts since December 2018 – the most recent just a month ago – in efforts to support prices and balance supply and demand. At the same time, the cartel sees demand expanding in 2020 and into 2021. OPEC Secretary General Mohammed Barkindo said recently, “what we see from our side is an upside potential of growth from the demand side of the equation, which will affect the total balance for the rest of the year…”

For oil producers, increased demand may be the only way out of low-price regime. Middle East tensions in recent months – the Iranian attack on Saudi oil facilities, and the US-Iran spat in December – spiked prices, but the spikes faded quickly. Oil producers are hoping that Barkindo turns out to be correct, and that demand intensifies, as that will likely be the surest way out of the current low-price regime.

For some small- to mid-sized oil companies, renewed demand may catch them well-prepared for an increased operational tempo and higher product deliveries. Which, in turn, will translate to improved profits and share prices for investors.

We’ve used TipRanks’ Stock Screener tool to find three “strong buy” energy stocks that are primed for gains, as recent months have pushed their share price down. Let’s take a closer look.

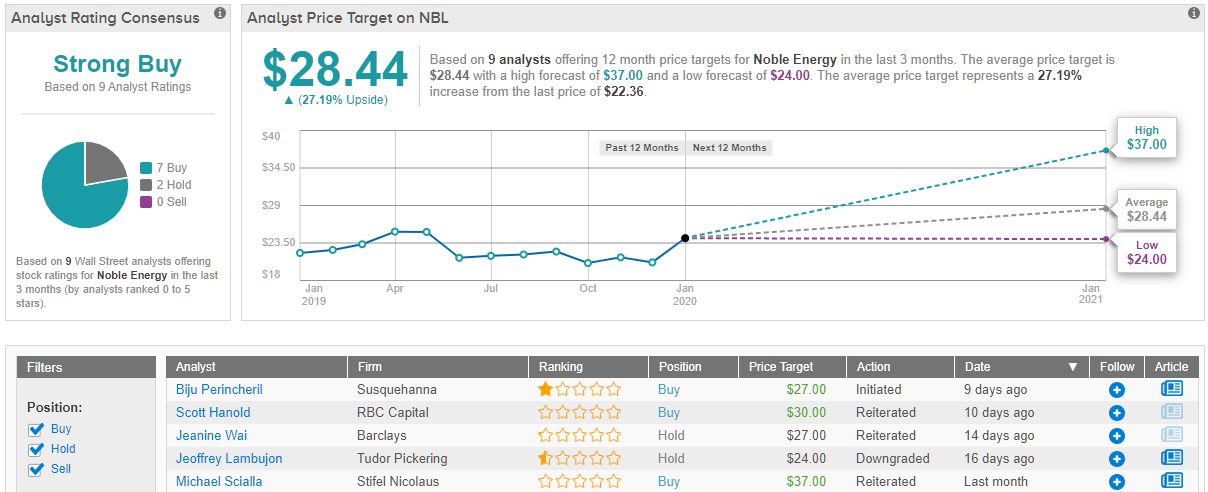

Noble Energy (NBL)

Houston-based Noble energy is mid-cap hydrocarbon exploration and development company with a global footprint. A slim majority of the company’s operations are in Texas – Noble is a major player in the Permian Basin and Eagle Ford formations – but the company is heavily invested in offshore operations in Equatorial Guinea and in the first natural gas production by both Cyprus and Israel. The Israeli gas fields holds 43% of Noble’s proven reserves.

Noble’s operations in the Mediterranean went online in late 2019, and the capex on expansion combined with low prices to depress earnings. The company’s revenue came in at $1.12 billion for Q3, but that was down from $1.27 billion the prior year. Unadjusted earnings saw a sharper loss, from Q3 2018’s 47 cents to the recent 4 cents. However, the adjusted EPS, a net loss of 10 cents, was better than the 11-cent loss expected.

Writing on the stock from Stifel Nicolaus, analyst Michael Scialla said, “Our analysis suggests the company’s DJ and Southern Delaware Basin wells are significantly outperforming nearby peers. Despite an impending Eagle Ford production decline, the NBL’s U.S. assets are poised to generate 2020 oil growth and FCF.”

Scialla raised his price target on NBL to $37 (from $34), supporting his Buy rating on the stock. His price target implies room for a robust 65% upside. (To watch Scialla’s track record, click here)

Another bullish view of Noble’s strength comes from its TipRanks Smart Score. This score, derived from eight separate data sets, comes in at a perfect 10, showing that the stock is likely to outperform the broader markets in the coming year.

All in all, NBL’s recent analyst reviews include 7 Buys and just 2 Holds, giving the stock a Strong Buy from the consensus view. Shares are priced at an affordable $22.36, and the $28.44 average price target suggests an upside potential of 27%. (See Noble stock analysis at TipRanks)

Goodrich Petroleum Corporation (GDP)

Next up for our inspection is a micro-cap oil and gas company, with oil operations in Texas’ Eagle Ford formation and gas ops in Louisiana’s Haynesville Shale. Falling prices for both oil and gas have hurt the company, depressing share prices more than increasing production could compensate. GDP shares lost 32% in 2019.

That loss, however, has made the company’s stock a bargain buy should improved demand push prices back up. In Q3 2019, the most recent reported, Goodrich’s natural gas output increased by 61% year-over-year, reaching 136 million cubic feet per day. High production kept earnings in the black, and while the 14-cent EPS missed the forecast, it was up 16% yoy.

So, Goodrich’s situation now is simple: the stock is selling low, yet the company’s oil and gas production is increasing, and earnings are solid. It’s a firm base for future investment, and Wall Street is casting an interested eye at the company.

Welles Fitzpatrick, of SunTrust Robinson, is among the analysts who believes Goodrich’s current position makes the stock a buying proposition. Fitzpatrick noted that the company’s forward guidance is “extremely conservative,” offering projections “substantially below” consensus. He was impressed, however, with the “[Goodrich’s] clean balance sheet and acreage in the core of the Haynesville.”

Fitzpatrick backed his Buy rating with a $12 price target, suggesting room for 34% upside growth. (To watch Fitzpatrick’s track record, click here)

GDP’s three most recent analyst reviews are all Buys, giving the stock a unanimous consensus rating of Strong Buy. Shares are priced modestly, at $8.71, and the $14.33 average price target indicates an impressive upside of 86%. (See Goodrich’s price targets and analyst ratings on TipRanks)

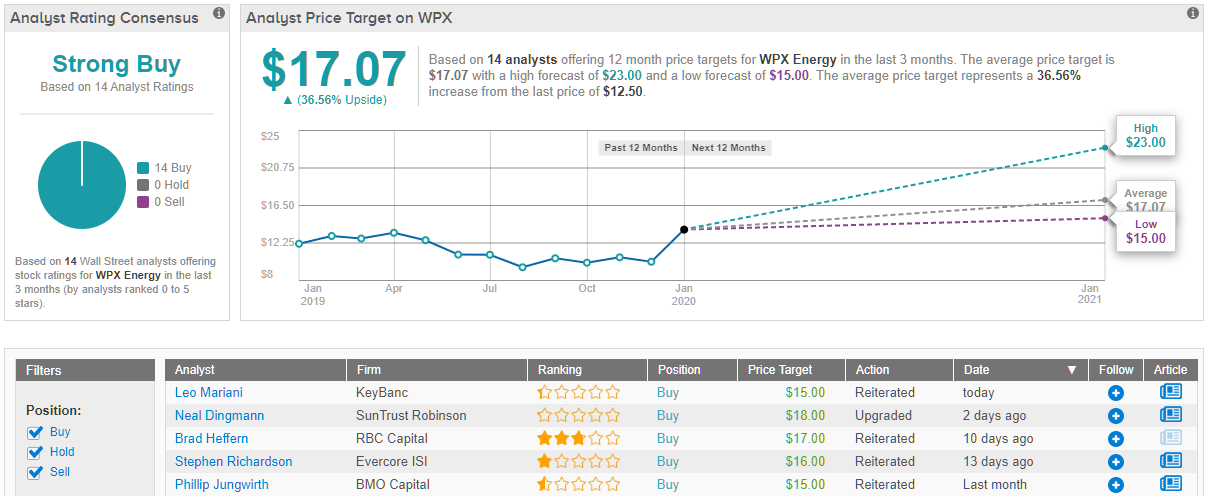

WPX Energy, Inc. (WPX)

Last on our list is WPX, a mid-cap company with a $5.3 billion market cap and operations in North Dakota and Texas. The company’s assets lie in the Williston Basin and the Permian Basin – two of North America’s richest oil-bearing formations. WPX’s proven reserves contain more than 480 million barrels of oil equivalent, of which a majority are in Texas. The company has over 700 operating wells on its land holdings.

WPX holds a strong position in production, backed by large reserves. In 2018, the company showed $2.3 billion in revenues and brought in $150 million in net profits. WPX’s most recent reported quarter was Q3 2019, and showed EPS at 9 cents, below the 11-cent forecast but above the 7 cents reported the year before. Revenues beat the forecast, by 25%, coming in at $795 million, and beat the year-ago number by 64%.

In mid-December, WPX shares spiked after the company announced its purchase of the privately held oil company – and Permian Basin competitor – Felix Energy. The deal was valued at $2.5 billion, adds land holdings from the Delaware Basin to WPX’s already-valuable portfolio. The Delaware is a rich shale-oil formation; this purchase adds the acreage, and reduces WPX’s competition.

Evercore ISI analyst Stephen Richardson writes of WPX, “The market has rewarded WPX for a well-timed, structured, and priced acquisition of Felix… We have been of the view that legacy WPX was setting up to beat and raise in the Permian in 2020, and we think this… accounts for some of the additional oil growth now reflected in combined-co guidance… Felix is ratably almost doubling production on an exit to exit basis which unsurprisingly raised some eyebrows.”

Richardson is bullish on this stock, and his Buy rating is backed up by a $16 price target – implying room for 28% growth to the upside. (To watch Richardson’s track record, click here)

With 14 Buy ratings, WPX shares hold a Strong Buy rating from the analyst consensus. Shares are not expensive, priced at just $12.51, and the average price target of $17.07 suggests a strong upside potential of 37%. (See WPX’s stock analysis at TipRanks)