Unphased by some risk? If the answer is yes, then healthcare stocks might be the way to go. These names tend to be more volatile in nature as a single catalyst like trial data or a verdict from the FDA can either propel shares upward or send them plummeting overnight.

While the degree of risk involved can turn-off some potential investors, others are enticed by the possibility of sky-high rewards. Take Agile Therapeutics, for example. Shares popped over 200% after an FDA AdCom voted in favor of Twirla, its contraceptive patch.

That being said, when it comes to biotechs it’s important to do your due diligence as not all names in the space are ready for takeoff. To narrow down only the most compelling stocks, we took advantage of TipRanks’ Stock Screener. The tool pointed us in the direction of 3 biotech stocks with huge upside potential from the current share price. We’re talking 100% or more here. If that wasn’t enough, we found out that the Street is also in favor of these names as each has earned a “Strong Buy” consensus rating.

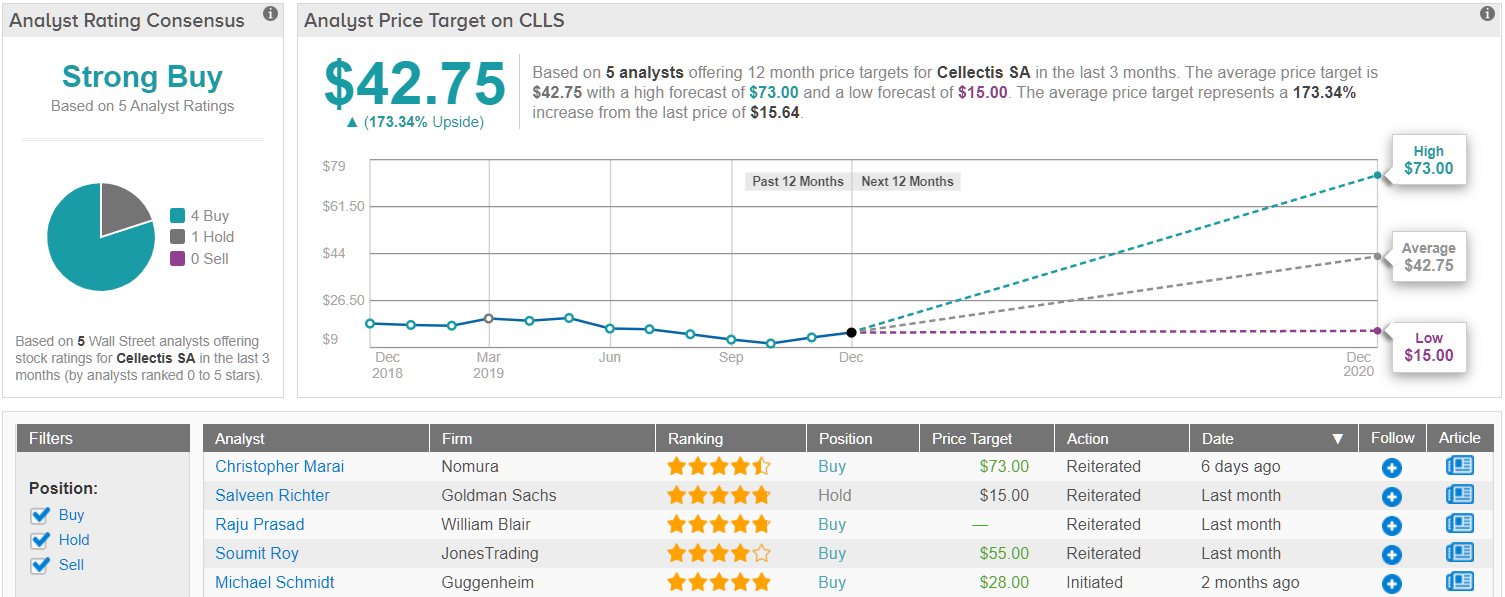

Cellectis SA (CLLS)

Who’d have thought that editing our genes to treat cancer would become a possibility? Cellectis had just that thought. The biotech uses its innovative TALEN technology to edit the Chimeric Antigen Receptor (CAR) T-cells taken from healthy donors to create “off-the-shelf” immunotherapy product candidates that could work for the largest amount of people. Even though shares have dipped year-to-date, some members of the Street see major growth in store.

While the company did report a net loss in its third quarter, Wells Fargo analyst Jim Birchenough reminds investors to consider the progress of its CAR T-cell platform and pipeline. CLLS has three wholly owned clinical UCART candidates, with it recently administering CS1 CAR-T, UCARTCS1, in the first multiple myeloma patient in the MELANI-01 trial. In addition, the trials for the two other products are open for enrollment.

All of this has impressed Birchenough, noting that the UCART pipeline is even more promising thanks to manufacturing changes. “Since the original UCART123 IND filing, CLLS has improved the reliability and reproducibility of the UCART manufacturing process and, for UCART123 these changes necessitated filing a new IND. While CLLS can supply several hundred patients from a single healthy donor, the company has manufactured several batches of each of its UCART products from several donors using the refined manufacturing process that accommodates inherent variability between donors,” he explained.

As a result, the five-star analyst left the Outperform rating and $47 price target as is. Given this target, the analyst thinks that shares could soar 195% in the next twelve months. (To watch Birchenough’s track record, click here)

Like Birchenough, Ladenburg Thalmann’s Wangzhi Li points to the UCART products as the key component of his bullish thesis. “We are encouraged that UCART-CS1 now dosed 1st pts, and UCART123 and UCART22 expect to dose pts in the near term. We see clinical data reports from any of the programs (likely in 2020) as key catalysts for CLLS story, and a clinical win could be a key to potentially unlock CLLS value,” the four-star analyst noted. To this end, Li reiterated the bullish call and $40 price target. (To watch Li’s track record, click here)

Turning now to Wall Street, other analysts are on the same page. With 4 Buys and 1 Hold received in the last three months, the word on the Street is that CLLS is a Strong Buy. On top of this, the $42.75 average price target brings the potential twelve-month gain to 173%. (See Cellectis stock analysis on TipRanks)

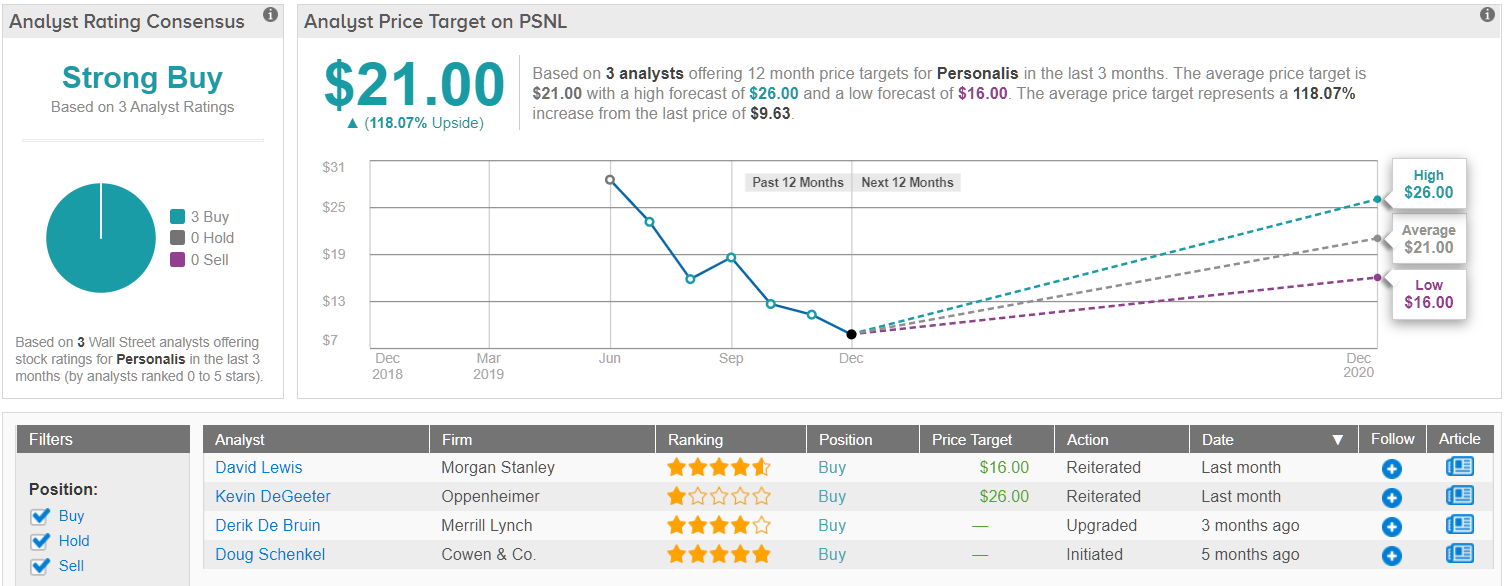

Personalis (PSNL)

Also focusing on treatments for cancer, Personalis provides more comprehensive molecular data about each patient’s tumor. Since its June IPO, shares have definitely struggled, but the tide could be turning according to analysts.

Kevin DeGeeter of Oppenheimer tells investors that he is especially excited about PSNL’s collaboration with Merck KGaA, arguing that it validates the ImmunoID Next platform’s immunophenotyping capacity in a research setting. Adding to the good news, the analyst cites the expansion of the number of ordering customers, specifically larger customers with multiple potential research projects, as driving possible customer base growth in the first half of 2020.

This prompted the analyst to comment, “We view PSNL as a proxy for continued growth in pharmaceutical immune oncology research budgets and differentiated based on its complete focus on corporate and government customers (no clinical testing). We view this focus as a key asset supporting a premium product offering emphasizing quality of sequencing result and flexible menu.” Bearing this in mind, DeGeeter gave PSNL his stamp of approval, maintaining the Outperform rating and $26 price target. As such, the upside potential comes in at a whopping 155%. (To watch DeGeeter’s track record, click here)

Meanwhile, Cowen’s Doug Schenkel did acknowledge that the VA-heavy mix poses a cause for concern. However, he thinks that the valuation still reflects a compelling opportunity, lending itself to his conclusion that the biotech is a good Buy. (To watch Schenkel’s track record, click here)

What does the rest of the Street have to say? Looking at the 100% Street support, the consensus is unanimous: PSNL is a Strong Buy. While the $21 average price target is lower than DeGeeter’s estimate, it still suggests that shares could more than double in the twelve months ahead. (See Personalis stock analysis on TipRanks)

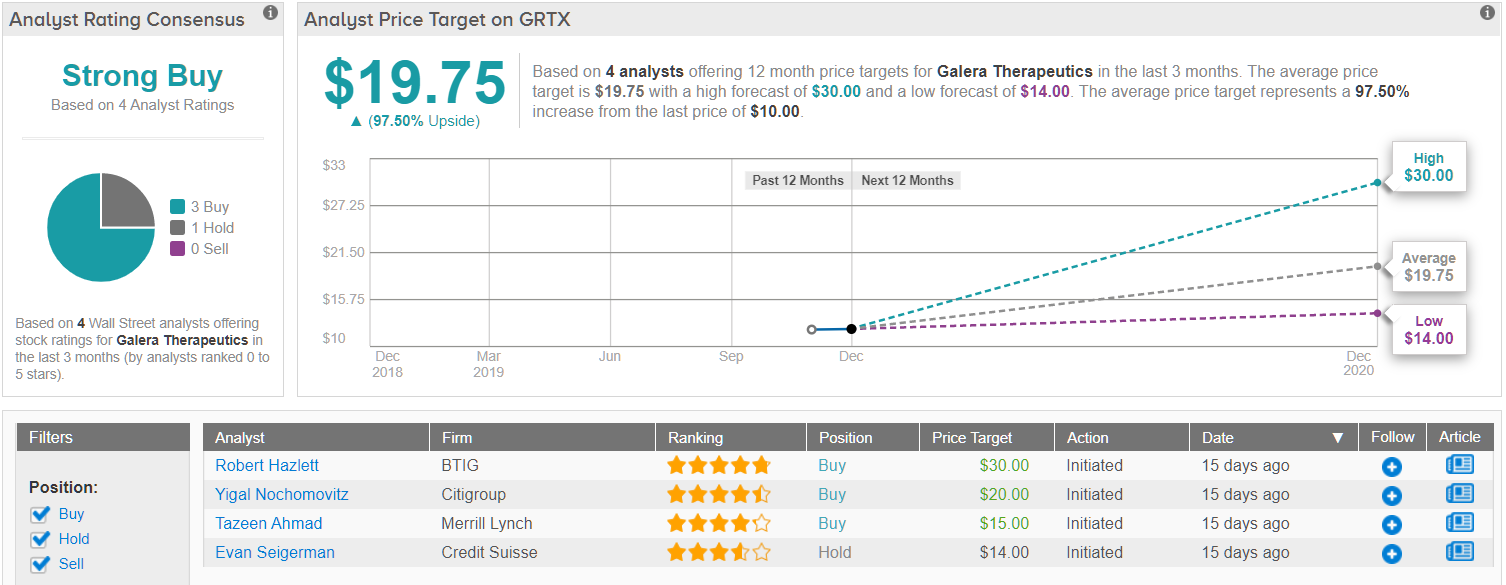

Galera Therapeutics (GRTX)

Making its market debut this past November, Galera Therapeutics is working on developing mechanism-based therapies for cancer patients. Given the huge unmet need that could be met by the biotech’s products, one analyst has high hopes.

BTIG analyst Robert Hazlett highlights GRTX’s candidates that have the potential to not only protect patients from radiotherapy induced toxicities but also to enhance the efficacy of the radiotherapy itself as a key point of strength. Its lead asset, GC4419, is an IV superoxide dismutase (SOD) mimetic, currently progressing through a Phase 3 trial for use in the reduction of severe oral mucositis (SOM) in head and neck cancer patients who are undergoing radiotherapy.

In Phase 2b, data indicated that the drug was able to cut the duration and incidence of SOM, leading to an FDA Breakthrough Designation for GC4419. As SOM occurs in about 70% of patients receiving radiation for head and neck cancer, Hazlett sees a substantial material opportunity. “With nothing currently approved for SOM in head & neck cancer patients, we estimate GC4419’s peak revenue potential in this setting in the US is greater than $500 million,” he stated.

It also doesn’t hurt that GRTX is evaluating GC4419’s ability to reduce esophagitis brought on by radiotherapy in patients with lung cancer. As enrollment could begin in the first half of 2020, Hazlett puts the peak potential in the U.S. at over $300 million.

Based on this potential, it’s no wonder, then, that the five-star analyst initiated coverage with a Buy recommendation. At the $30 price target, shares could skyrocket 205% in the coming twelve months. (To watch Hazlett’s track record, click here)

All in all, the rest of the Street also likes what it’s seeing. 3 Buys and 1 Hold assigned in the last three months amount to a Strong Buy consensus. Thanks to the $19.75 average price target, the upside potential lands at nearly 100%. (See Galera stock analysis on TipRanks)