After a month of rising stock markets, which have seen the S&P 500 gain 14%, there is a hope that the economic contraction will be shorter than was initially feared. As the Trump administration has begun setting guidelines for reopening economic activity, and at the State level some governors are planning to reopen while others tighten social distancing restrictions, some market strategist are openly saying that the worst is now behind us.

Chiming in from Ned Davis Research, chief US strategist Ed Clissold has revised the cautious stance he set early in March. Noting, “The market tends to lead the economy,” Clissold goes on to say, “An average of four months before the end of recessions is when the S&P 500 bottoms. So, if you look out a few months and think things will be getting a little bit better, stocks should anticipate that.”

Assuming that the S&P’s March 23 reading of 2,237 was the bottom, then by Clissold’s logic we should see the recessionary factors start to recede in mid-July. This would be consistent with the V-shaped recovery hypothesis, and an early economic turnaround in 2H20. Other recent forecasts have proven correct – especially that the S&P would find resistance in the 2,750 to 2,850 range. The index has now broken above that level, in a positive sign for investors.

If the optimists are right, and markets are just a few months away from breakout, then now – while prices remain low – is the time to prepare your portfolio.

And this brings us to penny stocks, those low-cost equities priced below $5 per share – are a high-stakes opportunity with upsides that frequently approach several hundred percent and a low enough cost of entry to mitigate the attendant risk. These companies are priced low for a reason, but for those that break out, the rewards are tremendous.

With this in mind, we’ve used the TipRanks database to pinpoint three penny stocks poised for sky-high gains. To minimize the risks, all three combine high ratings from Wall Street’s analysts, and a growth potential of 80% or higher.

Arcimoto, Inc. (FUV)

We’ll start with a green manufacturer. Arcimoto has developed a tandem two-seater electric vehicle – a three-wheeled design – Fun Electric Vehicle, or FUV, as the company has dubbed it. The company is currently producing FUVs at a rate of one per day in its Oregon factory, and has received pre-orders for 4,128 vehicles. The tiny FUV is marketed as a leisure product, perhaps the only marketing route for American customers who usually prefer their cars large.

Looking forward, Arcimoto has plans to upsize its vehicle line, and is developing prototypes to test out FUVs as emergency or delivery vehicles. The company already has a rental franchise in Key West, Florida, and has delivered 8 vehicles. The rental franchise will target tourist rentals on the island.

H.C. Wainwright analyst Amit Dayal sees the current economic slowdown as a net positive for the company. Arcimoto is using the opportunity to streamline operations and increase efficiency, measures that will reduce overhead in the long run. Dayal writes, “We were expecting the company to deliver 729 vehicles during 2020, which we have revised down to 235 now. We expect production to bounce back to nearly 2,000 units in 2021. We expect the company’s operating costs to be lower because of the furlough; we are projecting 2020 operating costs of $9.3M, compared to $21.3M previously.”

“We believe that the company could see increased interest in its Deliverator model, as businesses shore up their delivery strategies in a post-COVID-19 environment. In line with this, the company has expanded its Deliverator pilot program to include a major national grocer,” Dayal added.

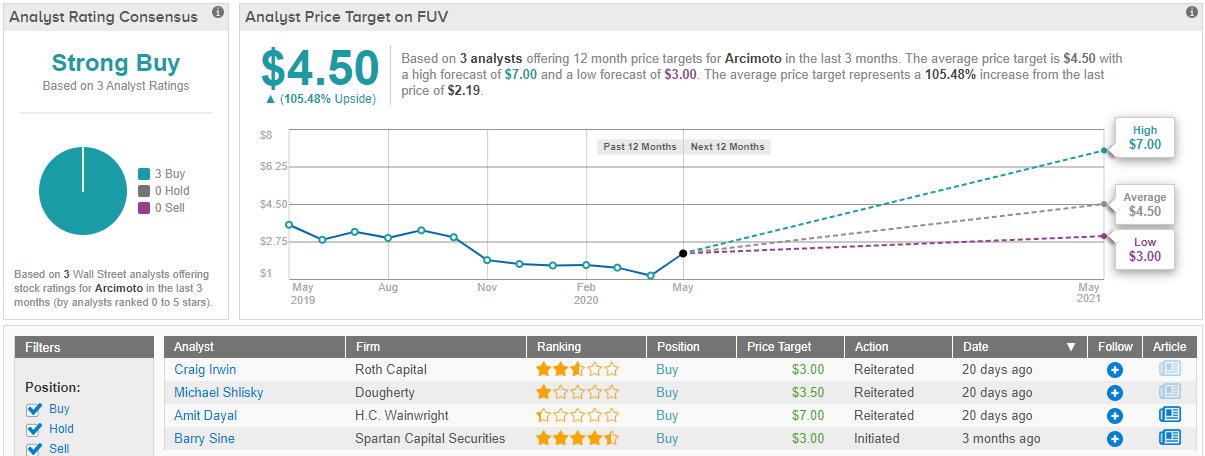

As a result, Dayal gives FUV shares a Buy rating, and his $7 price target suggest an upside potential of 220%. (To watch Dayal track record, click here)

Wall Street generally agrees with Dayal that Arcimoto has a clear path forward. This is seen in the average price target of $4.50, which indicates an upside of 105%. The Strong Buy consensus rating is based on a unanimous 3 Buy reviews. (See Arcimoto stock analysis on TipRanks)

Emcore Corporation (EMKR)

Next up is a technology company, with strong links to the defense industry. Emcore produces mixed-signal optics and micro-electromechanical systems (MEMS) that underlie many leading aerospace and defense systems. Emcore products are vital components in navigation systems.

After missing earnings expectations in calendar Q3 by 12 cents, and reporting a 29 cent per share loss against a forecast of 17 cents, calendar Q4 (fiscal Q1) showed a strong sequential improvement. The company still recorded a net loss, but it was only 8 cents – far better than the 22 cents forecast. Revenue in the final quarter of 2019 reached $25.48 million, up 6% from the year-ago quarter.

The long – and recently extended – lockdown in California is hurting Emcore’s production capabilities. At the same time, as a company with contractual ties to the defense establishment, Emcore is almost certain to have a deep backlog of pent-up demand waiting for it when normal or near-normal work resumes.

That is the thesis underlying 5-star analyst Dave Kang’s stance on EMKR. Writing from B. Riley FBR, Kang says “We believe it has a compelling risk/reward, considering its CATV business should benefit from increased telecommuting, and once the CA lockdown is lifted, its A&D business should immediately kick into a high gear based on strong pent up demand.” The analyst added, “We are buyers of EMKR into the print based on a favorable risk/reward profile, coupled with a recent trend of investors being less concerned about supply-related issues as long as demand remainsr obust. We believe its CATV demand could benefit from increased telecommuting, and its Aerospace/Defense (A&D) should immediatelykick into a high gear once the CA lockdown is lifted by the end of May.”

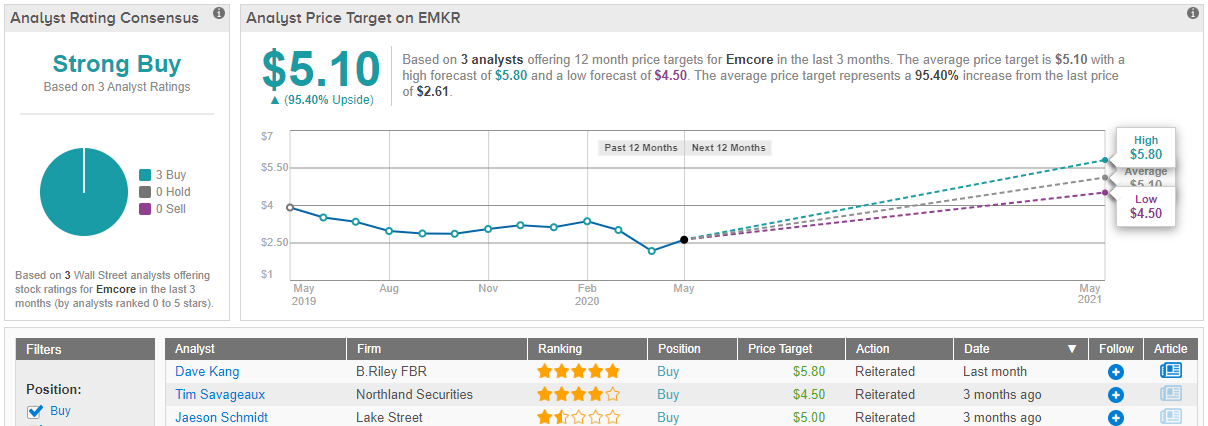

Kang gives Emcore shares a Buy rating, in line with this bullish stance. His $5.80 price target indicates his confidence in a 122% upside potential for the stock. (To watch Kang’s track record, click here)

This is another stock with a unanimous Strong Buy rating from the analyst consensus. Like FUV above, EMKR’s rating is based 3 recent Buy reviews. The stock is priced low, at just $2.61, and the average price target of $5.10 suggest that is has room for 95% upside growth in the coming 12 months. (See Emcore stock analysis on TipRanks)

Medallion Financial (MFIN)

The last stock on our list is a specialty finance company based in New York City. Medallion’s name reflects an important part of the company’s portfolio: taxi medallions. These permits to operate a taxi cab are available in limited numbers, and cab operators will pay top dollar – often securing large loans – in order to procure them. In addition to medallion-backed loans, Medallion also offers and services consumer, light industry, and small business loans.

Medallion reported its Q1 results just yesterday (April 30), and showed deep losses. EPS came in at a 56-cent per share net loss, much worse than the 12-cent loss expected. Revenue for the quarter was also down – the $19.6 million reported was 33% below forecasts and down 32% year-over-year.

The COVID-19 pandemic and associated economic disruption are behind MFIN’s Q1 losses. The company’s portfolio has large numbers of taxi medallions and consumer loans – and both are segments that have been hard-hit by the lockdowns. NYC taxi traffic is far down, and unemployment is skyrocketing – making it harder for people to make their loan payments.

Riley FBR analyst Scott Buck sees the current difficult times as an opportunity for Medallion. He believes that the company can make a meaningful write-down in its medallion loans, and pivot toward more profitable endeavors. Describing MFIN’s prospects, he writes, “Given what we expect to be a more challenging environment for consumer loan demand, more challenging credit and the ongoing shutdown in New York City, we are reducing our estimates for 2020 and 2021. We are now modeling full-year 2020 EPS of $0.26, down from $1.05. The decline is driven almost entirely from higher provisioning, predominantly on the medallion portfolio, which we view as a positive long-term as it allows investors, and management, to put their attention on the growing and profitable consumer lending segment.”

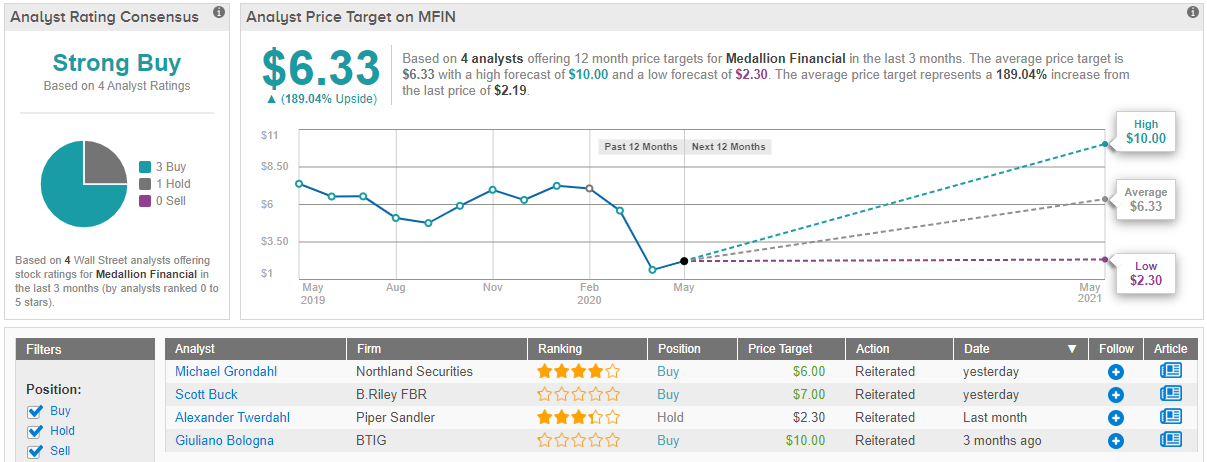

Buck keeps his Buy rating on MFIN, and his $7 price target suggests a robust 220% upside potential. (To watch Buck’s track record, click here)

Overall, Medallion Financial keeps a Strong Buy analyst consensus rating, based on 4 recent reviews, including 3 Buys against a single Hold. Meanwhile, the $6.83 average price target reflects an impressive 12-month upside potential of 189%. (See Medallion stock analysis on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.