The second quarter of 2020 started with a slide in the markets, as the glum mood came after President Trump acknowledged publicly that the first two weeks of April are likely to see a rise in deaths from COVID-19, as the epidemic intensifies.

In one way, this is to be expected – the disease has an incubation period up to 14 days, and course of illness lasting up to 14 cases, in cases with notable symptoms. The majority of cases are reported as mild, but the disease, as we know can be deadly in more severe cases. The social distancing moves, imposed through lockdowns and quarantines, are pounding the economy – but also slowing the spread of COVID-19. But they were implemented some two to three weeks ago, so the natural course of the disease, in those exposed before the lockdown policies took hold, is reaching its peak now, The good news is, the success of social distancing policies is slowing the disease spread, allowing hospitals to cope.

Downturns can present buying opportunities for contrarian-minded investors. Investment firm Needham has recently been thinking along these lines and came out with reports on stocks that should rally when the spread of COVID-19 will stabilize, or actually benefit from the current situation.

We’ve taken three of Needham’s top picks and looked them up in the TipRanks database. These are investments that TipRanks reveals as “Strong Buys” and, more importantly, all three offer robust upside potential. Let’s take a closer look.

EverQuote, Inc. (EVER)

Everything is available online these days. It’s one of the wonders of the internet information age in which we live, as just about any product or service can be researched and purchased with the click of a mouse and a simple online search. Some products are more amenable to online service than others, and insurance is clearly in that category.

Online insurance firm EverQuote connects customers and providers through its platform, and has expanded from its beginnings in the car insurance sector to also offer life and home policies. EverQuote’s services are free for site visitors – insurance customers don’t pay any fee for using the site. The company brings in profits from charging referral fees to the policy providers – but those fees are only assessed when policies are purchased.

EverQuote shares have underperformed the broader markets recently, having lost half of their value since the current bear trend began. This came after a Q4 that saw the company outperform expectations, with a net loss of 4 cents per share against a forecast of 6 cents – a loss that was less than one-third the year-ago figure of 15 cents. Revenue growth was strong in Q4, reaching $73.8 million, 8.2% over the estimates and up 85% year-over-year.

With the coronavirus pandemic in full swing, older forward guidance is of little use. But it’s important to note that as restrictions are lifted and business begins to resume in 2H20, customers will need to renew lapsed insurance policies – or may have been ‘scared straight’ by the downturn, into putting their insurance protections in order.

5-star Needham analyst Mayank Tandon agrees, seeing a clear path forward for the company. The analyst noted, “In our view, EVER’s business model should remain largely resilient given that it is run through a digital marketplace and ~85% of the revenue comes from auto insurance, which is a nondiscretionary expense… we believe that demand should remain strong as consumers look for ways to save money in a difficult economic environment and carriers/agents compete for share by leveraging highly measurable marketing channels.”

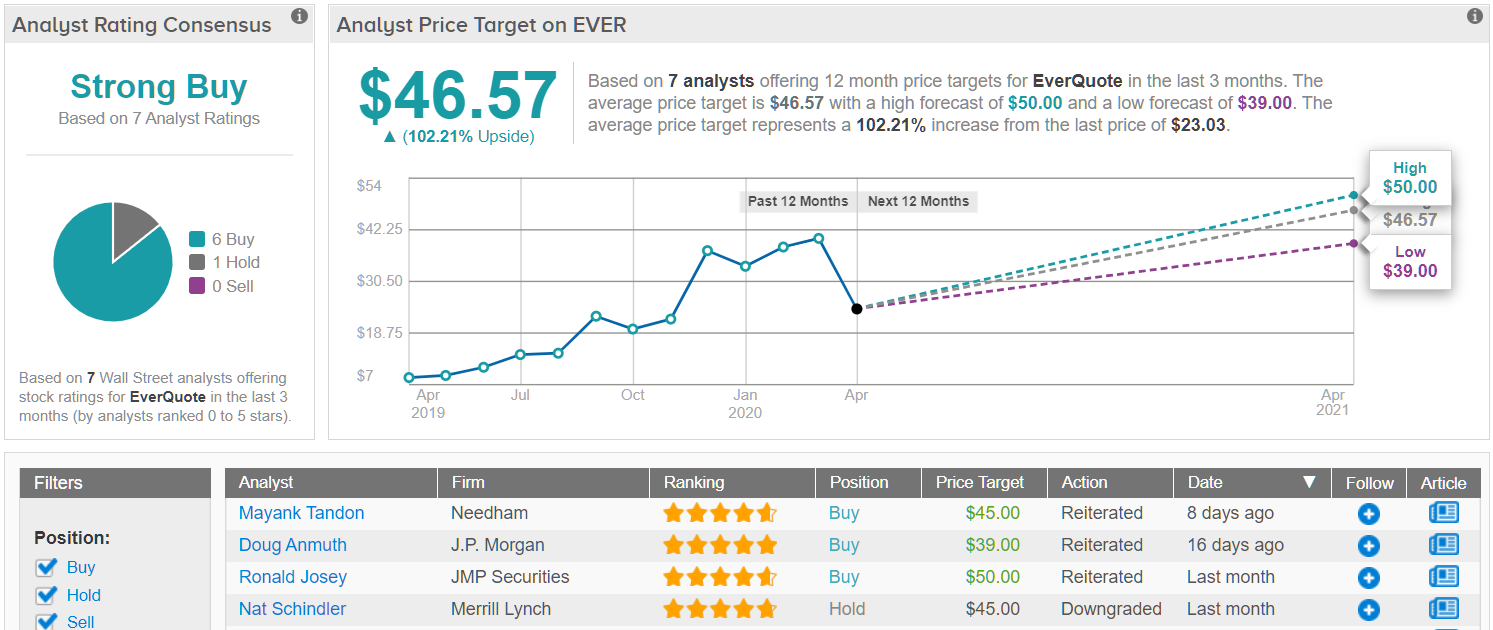

Tandon reiterates his Buy rating here, and sets a price target of $45, suggesting an upside 95%. (To watch Tanon’s track record, click here)

EVER’s Strong Buy analyst consensus rating is based on a 6 to 1 split of Buys versus Hold. Shares are priced low, at $23.03, and the $46.57 average price target suggests an upside potential of 102%. (See EverQuote’s stock analysis at TipRanks)

Livongo Health, Inc. (LVGO)

Moving to the health industry, we find an interesting company with a unique niche. Livongo is a biotech – that develops systems for the treatment of chronic health conditions. Specifically, the company works with patients with diabetes, using a combination of medical treatment and real-time data analysis technology to give customers a personalized approach to disease management. The connection here to COVID-19 is apparent: the coronavirus disease is dangerous to patients with preexisting chronic conditions, and better management of those is key to maintaining good health.

At the beginning of March, LVGO reported a strong Q4. Earnings were positive, at 2 cents per share, versus the 5-cent loss expected, and revenue, at $50.2 million, was 1.8% better than forecast. The revenue total also represented 137% year-over-year, a clear testament to the company’s valuable niche. In another clear sign that LVGO is well-suited to current conditions, the stock has posted 12% gains year-to-date, while the overall market has dropped sharply.

Writing for Needham, 5-star analyst Scott Berg notes these points, saying of Livongo, “We note shares of Livongo have significantly outperformed the broader market including the Russell 2000 significantly since they reported 4Q results on March 2… We want to highlight our belief Livongo’s success in FY20 is not perfectly correlated with the broader economy and they may actually benefit from some recent economic trends related to COVID-19.”

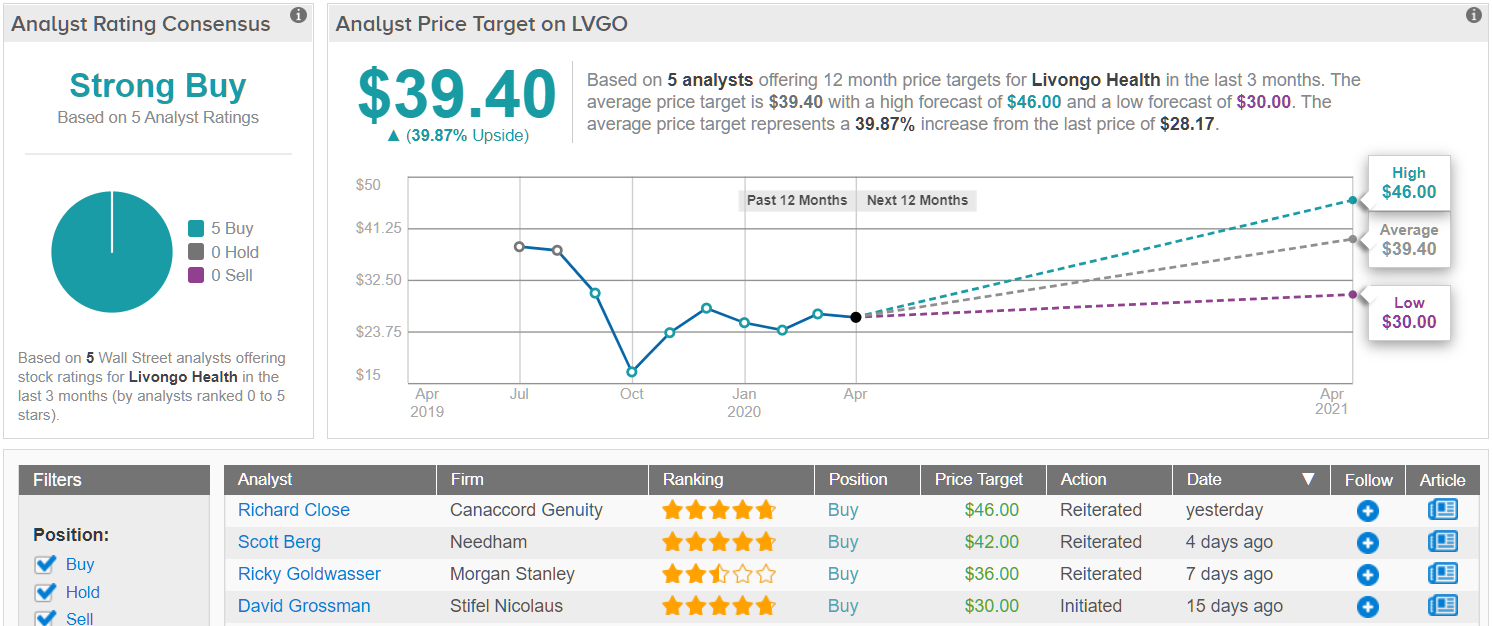

Berg sets a $42 price target to back his Buy rating, implying an upside of 51%. (To watch Berg’s track record, click here)

With 5 Buy-side reviews, Livongo holds a unanimous Strong Buy analyst consensus rating. The stock has an average price target of $39.40, which suggests a strong 40% upside potential from the current share price of $23.22. (See Livongo’s stock analysis at TipRanks)

Monolithic Power Systems (MPWR)

While its name suggests a utility, this is actually a tech company. Monolithic Power is maker of power circuits and converters, for digital, analog, and mixed-signal systems, used in portable electronics, wireless devices, computer systems, cars… and medical equipment. That last is a segment in high demand, as hospitals and medical providers are seeking expand their inventories in expectation of increased near-term need due to COVID-19.

Where most companies have lost heavily recently, MPWR has managed to outperform the market. While the stock is still down in the bear market, the loss is only 13%, compared to the 23% to 26% losses in the S&P 500 and Dow Jones indexes. Monolithic entered 2020 after an in-line Q4 report. Specifically, EPS, at $1.04, edged over the estimates by 1 cent, while revenue, at $166.74 million, was 2.23% higher than expected.

Strong customer orders powered the quarter, and MPWR finished 2019 with a backlog of work orders. That was noted by Needham’s 5-star analyst Quinn Bolton, who sees the backlog as a firm foundation for the company going forward, despite an overall gloomy economic outlook. Bolton opined, “Monolithic Power Systems has a consistent track record of execution and faster growth than its analog/mixed-signal peers. Targeting a growth rate 10-15 pts higher than the overall market, MPS is the fastest growing company in the attractive catalog analog segment, in our opinion. We believe MPS will continue to grow faster than the analog market in 2020 and 2021 driven by market share gains, the ramp of new products/design wins and co-development projects with tier-one customers.”

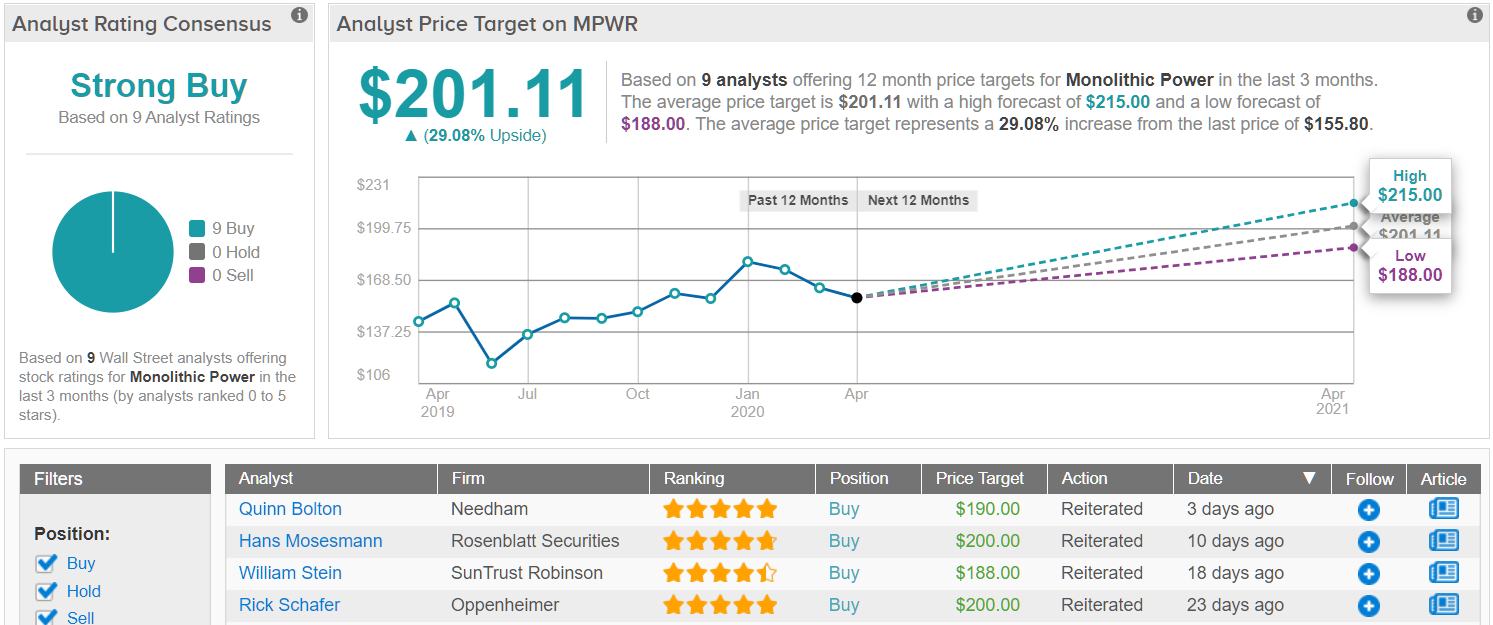

Bolton maintains his Buy rating on this stock, and while he lowered his price target considering current economic declines, he still sees the stock gaining 23% in the coming year, to reach $190 per share. (To watch Bolton’s track record, click here)

Monolithic is another company with a unanimous analyst consensus rating. The Strong Buy rating is based on 9 Buys, while the $201.11 average price target implies an upside potential of 29% from the current share price, $155.80. (See Monolithic stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.