Apple, Verizon, Nokia — there are almost as many stocks you can use to play the “5G revolution” as there are investors attempting to play it. Today, we’re going to use data from TipRanks’ Stock Screener to explore two lesser-known names that might be worth buying — and also examine why another could be one to avoid.

Without further ado — but with a word of thanks to Susquehanna Financial Group for doing the legwork — let’s dive right in and introduce you to all three:

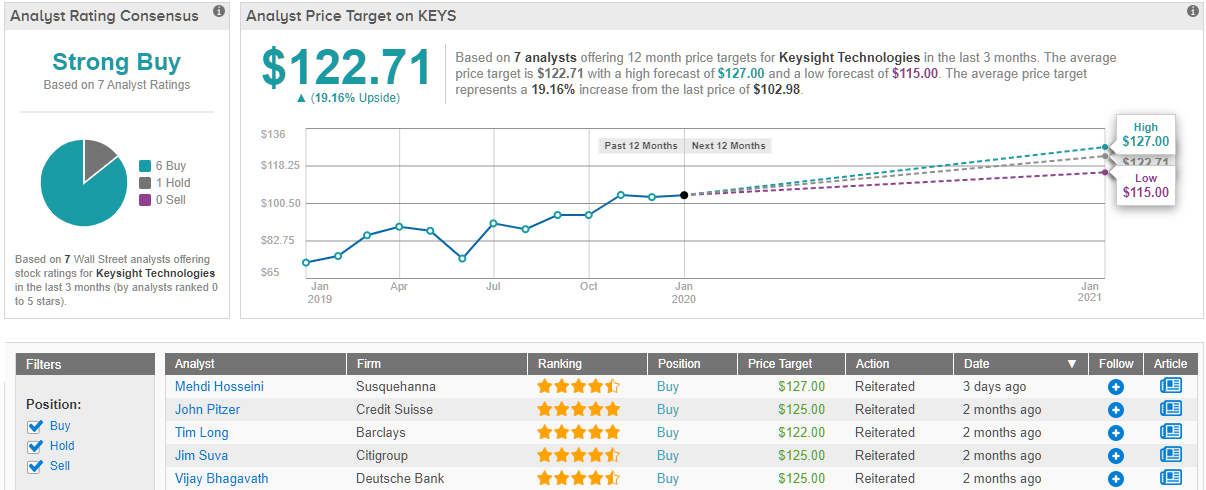

Keysight Technologies (KEYS)

We’ll begin with Keysight — at $19.4 billion in market cap, possibly the biggest 5G play you’ve never heard of.

Santa Rosa, California-based Keysight provides electronic design and test solutions to the 5G industry, ensuring that products designed to implement this new technology will work as promised, and with an emphasis on infrastructure testing as well as R&D work. Within 5G, Susquehanna analyst Mehdi Hosseini notes that Keysight “has exposure throughout the entire [5G] ecosystem including chipsets, devices, network infrastructure and data centers,” and plays a role in testing base stations and network upgrades as well.

Keysight is coming off a strong Q4 report in November, says Hosseini, in which the company reported 8% sequential sales growth (that might have been 10% growth but for the impact of the Trump administration’s ban on sales to customer Huawei). Based on how the stock is performing so far, Hosseini predicts Keysight could earn as much as $4.73 per share in fiscal 2020, and $5.77 in 2021, en route to consistent annual earnings in the $6-plus range. Not bad for a stock selling for only about $103 a share.

The analyst establishes his $127 price target on the stock based on the fiscal 2021 earnings estimate, applying a 22x multiple to those earnings, roughly in the middle of “peer group” stocks that are being valued at between 20 and 24x FY2021 earnings, which seems fair. (To watch Hosseini’s track record, click here)

For the record, six of the seven Street analysts who have published ratings on Keysight stock in the past two months, have rated it a “buy.” Even with average price targets a bit short ($122) of what Susquehanna is saying ($127), the consensus on the Street is that Keysight buyers today can expect to earn an 18.5% profit on their investment. (See Keysight stock analysis on TipRanks)

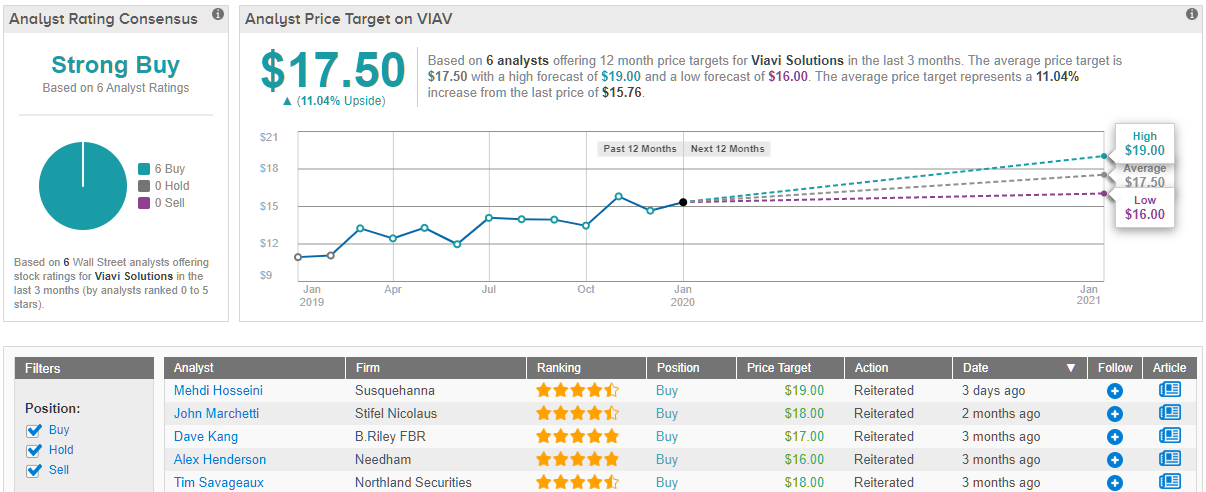

Viavi Solutions (VIAV)

Next up: San Jose, California-based Viavi Solutions, another testing provider that also offers monitoring and assurance solutions to the 5G industry. Once again, this is one of Hosseini’s favorites, and “a leader on fiber network testing and testing of base stations.” Hosseini goes so far as to describe it as “the king of fiber.”

“But wait!” you object. Aren’t we talking about 5G wireless internet? What does fiber have to do with that?

Hosseini explains: Even if 5G is a wireless technology, wireless providers still “need more fiber at points of access and as networks continue to replace legacy cables with advanced fiber technology.” What’s more, because 5G technology won’t appear by magic, and all in an instant, “between the 5G network buildout and the core network upgrade, the fiber business is in a strong position to capitalize on new opportunities,” which is a good reason to own Viavi in the time period leading up to the 5G buildout.

Hosseini has a $19 price target on this one, and viewed from one perspective, it’s slightly more aggressive than what some other analysts are saying.

So why does Hosseini think $19 (20% upside) is a more likely price? As the analyst points out, $19 a share is only about 20x to the company’s fiscal year 2022 earnings estimate. For comparison, some of Viavi’s competitors are trading for even richer multiples, approaching 27 times forward earnings! Viewed in that light, a $19 target price doesn’t look all that unreasonable.

TipRanks’ records show that over the last three months, even as six rating analysts have unanimously declared Viavi a “buy,” their average price target is only $17.50 per share. Which by the way is till 11% upside. (See Viavi stock analysis on TipRanks)

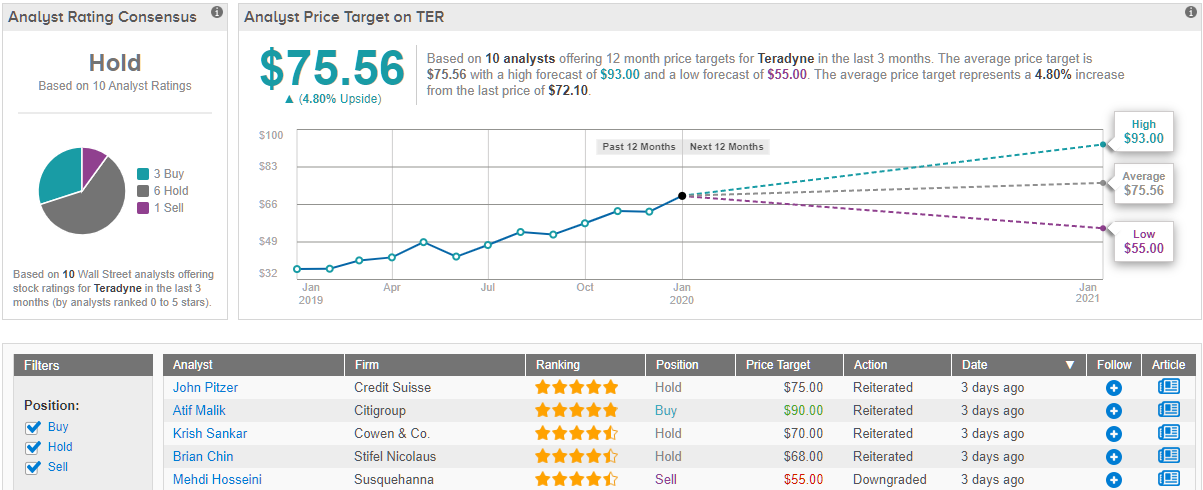

Teradyne (TER)

But will tell you what Hosseini does think unreasonable: Buying and holding Teradyne stock.

The only one of these three stocks that Hosseini dislikes enough to tar with a “negative” rating, North Reading, Massachusetts-based semiconductor tester Teradyne is almost certainly the best-known of the three stocks discussed in Hosseini’s report. It’s also, at a valuation of just 26.5 times earnings, arguably the best bargain of the three. (Keysight stock costs almost 32 times earnings, and Viavi — more than 133x!)

So why doesn’t Hosseini like it?

Simply put, he doesn’t think this stock’s earnings power is going to stick around much longer. Earnings per share are “peaking” at Teradyne, says the analyst, “with no rebound till mid 2021” — and 18 months may feel like a long time to wait for investors as they see competitors to Teradyne stock pulling ahead. Meanwhile, Teradyne stock is priced close to a 20-year high right now, which suggests there’s substantially more downside risk than upside potential in the near term.

With revenues slowing and costs rising, Teradyne’s current share price north of $72 just isn’t sustainable, argues Hosseini, and he believes that a year from now, the shares could be selling for as little as $55 — 24% downside risk.

Simply put, Hosseini thinks you can do better than that — and thinks buying Keysight and Viavi are the best ways to do it.

Granted, the analyst may be early to this call. Most of the other bankers following Teradyne today rate the shares no worse than “hold.” But even these optimists think Teradyne stock won’t climb much farther than $75 a share over the next 12 months — a bare 5% profit off of today’s prices. (See Teradyne stock analysis on TipRanks)