We’re coming off a year of major-league gains in the markets, and analysts are predicting a flatter year ahead. With the strong likelihood that share price returns will slow down, now is a logical time to start reassessing your portfolio. It’s time to decide which stocks to shed, and which to snap up.

Income is the deciding factor. Investing is all about making money, making your investments grow. So, if markets follow the predictions, and growth slows, that leaves dividends as the sensible route to go. Dividends provide a steady income stream, whether markets go up or down. But not all dividend stocks are created equal.

With that in mind, we delved into the market data from TipRanks.com to get the lowdown on 3 high-yield dividend stocks, two of which analysts think are set to shine in 2020, and one whose prospects aren’t quite as bright. Let’s dive in:

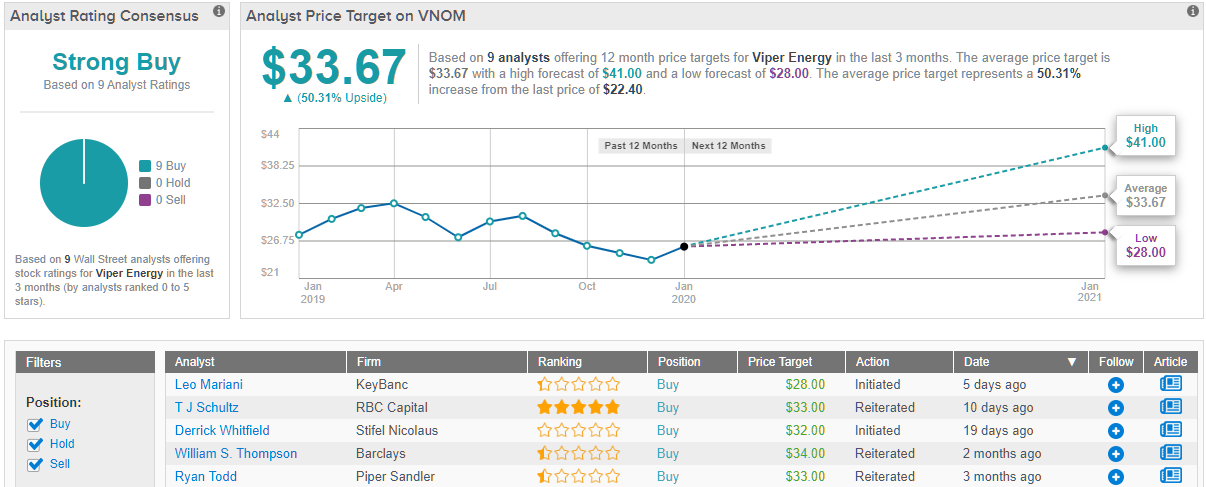

Viper Energy Partners (VNOM)

We’ll start with the cash-rich energy industry. Specifically, with Viper Energy, an oil company operating in the Midland formation of the Texas Permian Basin. This basin holds the largest proven oil reserves in North America, and operations in the Permian have made the US the world’s largest producer of crude oil. Viper has exploration rights in more than 14,000 acres in the Midland, which are exploited by third parties and subsidiaries who then pay the royalties that make up Viper’s income. Viper Energy’s land holdings contain an estimated 10 billion barrels of recoverable oil and oil equivalents.

Despite low oil prices, Viper’s position as a land holder rather than direct operator allowed it to continue recording profits in 2H19. At the same time, lower forward guidance pushed the stock price down. The top- and bottom-line numbers in Q3 – the last reported – disappointed; revenues missed the forecast by 6% and came in at $71.8 million, while EPS, at 13 cents, missed the estimate by only a penny. At the same time, EPS was up 160% year-over-year, and oil production showed a 9% sequential gain.

Better for investors, Viper has held fast to its dividend commitment. The company is consistent about making the payments, and has a history of adjusting the payment to make sure that it is sustainable. Currently, VNOM shares pay out a quarterly dividend of 46 cents, or $1.84 annually, giving a yield of 8.21%. This is more than four times the average yield found among S&P 500 stocks.

Viper’s production has been strong in recent months, and Wall Street analysts are taking notice. Pearce Hammond, of Piper Sandler, writes, “Positive news for VNOM as the company announced Q4’19 total production of 26.1 Mboe/d which bested our estimate by 2%… Taking into account increased equity unit count, VNOM increased production per million partnership units outstanding by ~5% q/q despite the headwinds of a broad activity slowdown on non-operated properties in Q4.” Hammond puts a Buy rating on the stock, along with a price target of $33, indicating an upside potential of 47%. (To watch Hammond’s track record, click here)

Also bullish is Welles Fitzpatrick from SunTrust Robinson. Fitzpatrick notes the strategic implications of Viper’s more recent land acquisitions: “While the company has been extremely active on the acquisition front, as of the last update interest had gone down somewhat. Instead we expect the company to refrain from adding acreage that it cannot reasonably predict activity plans for, a move that we think will be rewarded by the currently more conservative energy investor base.” Fitzpatrick backs his Buy rating with a $32 price target, showing confidence in an upside of 42%. (To watch Fitzpatrick’s track record, click here)

Overall, Wall Street likes VNOM shares. In fact, the analyst consensus on this stock is a unanimous Strong Buy, with 9 positive reviews. Shares are selling for $22.04, and the average price target of $33.67 suggests an impressive 50% upside potential. (See Viper stock analysis at TipRanks)

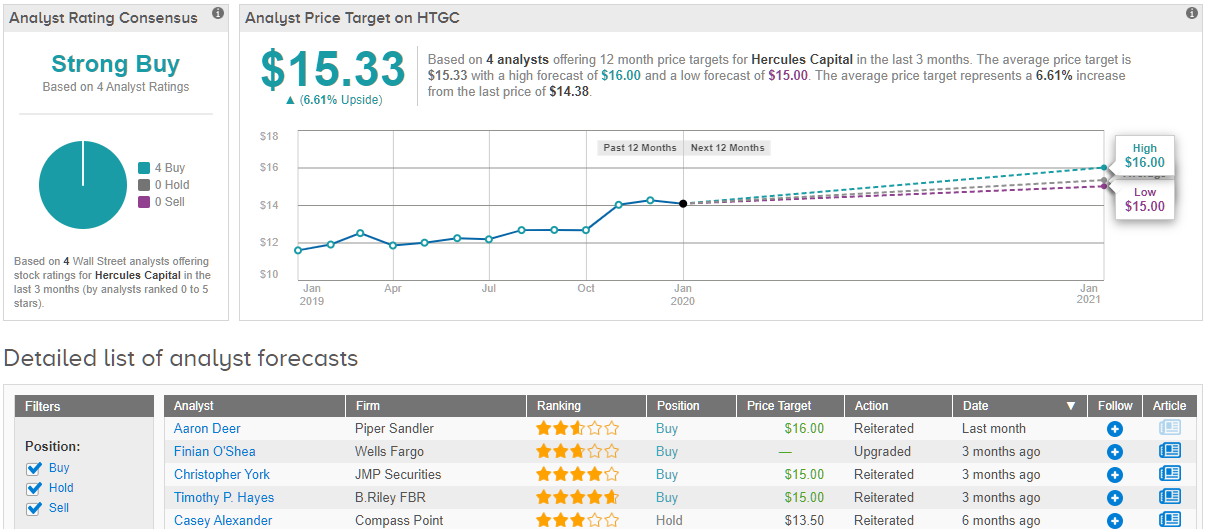

Hercules Capital (HTGC)

Venture capital is the lifeblood of innovation. Start-ups couldn’t start without money, and all new research and development has to be paid for. Venture firms are a major vehicle for injecting private money into the business world. Hercules Capital inhabits that niche, and to date has committed $10 billion to the life sciences, technology, and financial SaaS sectors.

Venture capitalists are necessary for innovators to succeed, but they don’t operate as a charity. They want to see a return on their money. Hercules has been fortunate, and its investments have provided strong returns. In Q3, the most recent report on record, the company showed a record in net investment income of $38.9 million, which came out to 37 cents per share. For the 12 months ending on September 30, the company showed a total of $103.2 million net investment income, or $1.03 per share. In three of the past four quarter reported, HTGC has beating the earnings forecasts.

The company has also grown its dividend. After holding the payment steady at 31 cents from 2013 to 2018, HTGC began increasing the payout, raising it three times in 2019. The current payment, 35 cents, annualizes to $1.40, for a yield of 8.9%. It’s a clear boon for investors.

Writing for Jefferies, 5-star analyst John Hecht points out the generally strong position of HTGC stock: “We observe positive trends and developments at HTGC, and we believe this reflects inherent competitive advantages and strong execution. Additionally, we point to an ongoing strong VC market backdrop and further enhanced balance sheet…”

Hecht maintains a Buy rating here, and puts a $16 price target on HTGC. His target suggests room for 11% upside growth in this stock. (To watch Hecht’s track record, click here)

HTGC is another company with a unanimous analyst consensus of Strong Buy, this one based on 4 Buy ratings. Shares sell for $14.30, and the average price target of $15.33 implies a modest upside of 6.6%. The key point here is the high dividend. (See Hercules Capital’s stock analysis at TipRanks)

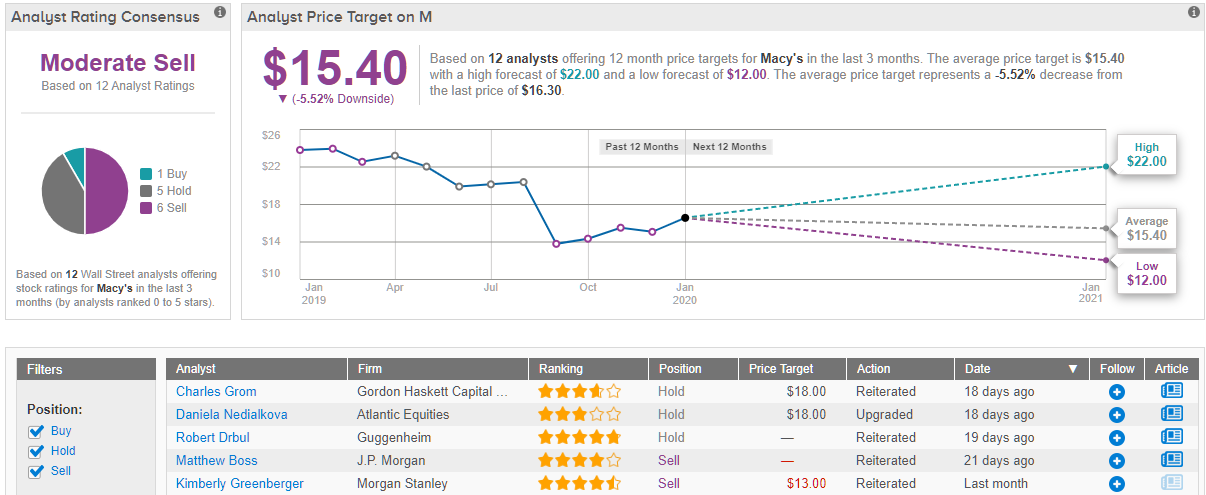

Macy’s, Inc. (M)

Macy’s is a storied name in American retail, a long-time mainstay of the department store segment. Before the decline of indoor shopping malls, there was a time when Macy’s stores were frequently seen as anchors for the country’s retail shopping outlets. But times have been hard for American retail. Since 2015, Macy’s has closed more than 150 under-performing locations.

In the most recent quarterly report, for third quarter 2019, M showed the first same-store sales decline in two years. The drop was 3.5%, and came in hand with a fall-off in revenue of 4.25%, to $5.17 billion. EPS did beat expectations, however, coming in at 7 cents versus the breakeven forecast. On the downside, that was a 65% drop year-over-year.

Falling earnings and a gloomy long-term outlook for brick-and-mortar retail have this stock on the ropes for now – but Macy’s is still paying out the dividend. At 37.75 cents per quarter, it annualizes to $1.51, and gives the highest yield on this list, of 9%. It’s a solid performance, but unless the EPS moves back up, it may not be sustainable.

Top analysts are not sanguine about the future for Macy’s. From Credit Suisse, 4-star analyst Michael Binetti writes, “[W]e think negative -0.6% SSS and -3% YOY gross profit dollar declines in a booming economy offer little evidence so far of a change in the ultimate medium and long-term challenges facing the company. Importantly, we still have little visibility on how EBIT margins can stabilize from here… We continue to believe it’s going to be increasingly difficult for the stock to stabilize on valuation alone.”

Binetti puts a $12 target on M stock, implying a 28% downside for the shares. This is inline with his Sell rating, and his believe that the stock will underperform in coming months. (To watch Binetti’s track record, click here)

Kimberly Green, 5-star analyst with Morgan Stanley, is also bearish here. She writes, “Despite closing stores proactively, store-only comps remain negative and we forecast them to remain so in the future, eroding ROIC. Expense cuts, real estate monetization, and secondary growth initiatives are encouraging, but we think the market needs to see core retail EBIT stabilization and a return to strong cash flow generation in order to become more constructive on the stock.”

Green’s price target is slightly higher than Binetti’s, at $13, but even that implies a downside of 22.5%. Again, this is in-line with her Sell rating. (To watch Green’s track record, click here)

The analysts clear on this stock: the consensus rating here is a Moderate Sell, based on 6 Sells, 5 Holds, and just 1 Buy. Despite the high dividend, Wall Street does not see this as a strong market play. Shares are selling for $16.78, but the average price target is $15.40, suggesting the stock will slip 8% in the next year. (See Macy’s stock analysis at TipRanks)