Micron (NASDAQ:MU) remains well-positioned to capitalize on the AI boom, but near-term uncertainty reared its head again following the memory giant’s latest update on Wednesday.

Speaking at the Wolfe Research investment conference, Micron signaled a bumpier road ahead for its gross margins in the May quarter (FQ3), expecting a sequential decline of a few hundred basis points. The company pointed to a shift in consumer DRAM mix as a key factor, alongside underutilization charges and ongoing pricing pressure in the NAND segment.

Management anticipates gross margins will improve after F3Q and reaffirmed its earlier expectation that PC and smartphone inventories will reach healthy levels by spring.

However, the new margin outlook falls short of Citi analyst Christopher Danely’s previous expectation of a “slight increase.” Consequently, Danely has revised his F3Q25E gross margin estimate downward from 40% to 35%. In addition, due to the revised margin guidance, he has lowered his F25 sales and EPS estimates from $34.6 billion and $6.75 to $33.8 billion and $5.93, respectively. He has also reduced his F26 revenue and EPS forecasts from $45 billion and $13.31 to $43.5 billion and $12.03, respectively.

That’s not to say Danely’s overall stance has changed, with the analyst pointing out that HBM (high bandwidth memory) is still the ‘star of the show.’

“While the lower guidance is disappointing, we are still optimistic on Micron given their AI HBM opportunity,” the analyst went on to explain. “We estimate HBM revenue to total $7.6 billion for Micron in C25 or 22% of revenue with gross margins at least 70% – driving margin expansion.”

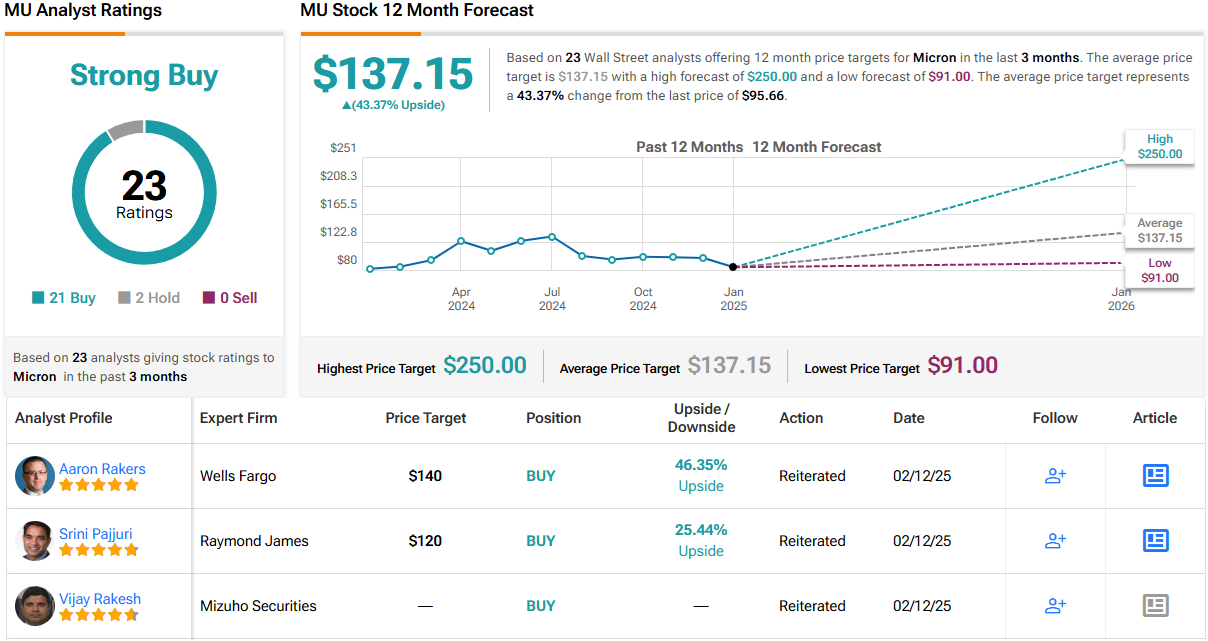

Bottom line, Danely rates MU shares a Buy, along with a price target of $150, suggesting the stock will gain ~57% in the months ahead. (To watch Danely’s track record, click here)

Raymond James analyst Srini Pajjuri offers a similar take, but even goes as far to say that while the update is obviously disappointing, his positive take is based on HBM, which is “arguably the best secular story the industry has ever seen (and in our view, has the potential to extend the upcycle into CY26).”

Pajjuri has also revised some estimates downwards, with his F3Q gross margin estimate now at 35.4% vs. 38% beforehand. Additionally, his FY25 EPS forecast goes from $7.07 to $6.54 while his FY26 estimate falls from $10.32 to $9.52.

Still, the analyst sees an appealing risk/reward setup and maintains an Outperform (i.e., Buy) rating on MU shares, with a $120 price target – suggesting a potential 25% upside from current levels. (To watch Pajjuri’s track record, click here)

20 other analysts also keep a bullish stance on Micron stock, while the addition of 2 Holds can’t detract from a Strong Buy consensus rating. Going by the $137.15 average price target, shares will be changing hands for a 43% premium a year from now. (See Micron stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.