Penny stocks, you either love them or you hate them. One of the obvious draws of these stocks trading for under $5 per share is the ability to get more bang for your buck. And should these bargain priced stocks see their share prices rise by only a small amount, the rewards can be staggering.

However, before jumping right into an investment in a penny stock, Wall Street pros advise looking at the bigger picture and considering other factors beyond just the price tag. For some names that fall into this category, you really do get what you pay for, offering little in the way of long-term growth prospects thanks to weak fundamentals, recent headwinds or even large outstanding share counts.

Taking all of this into consideration, we used TipRanks’ Stock Screener tool to zero in on the crème-de-la-crème when it comes to penny stocks. We are referring to the names that have not only received substantial support from Wall Street analysts but also boast sky-high upside potential from their current levels. Let’s take a closer look.

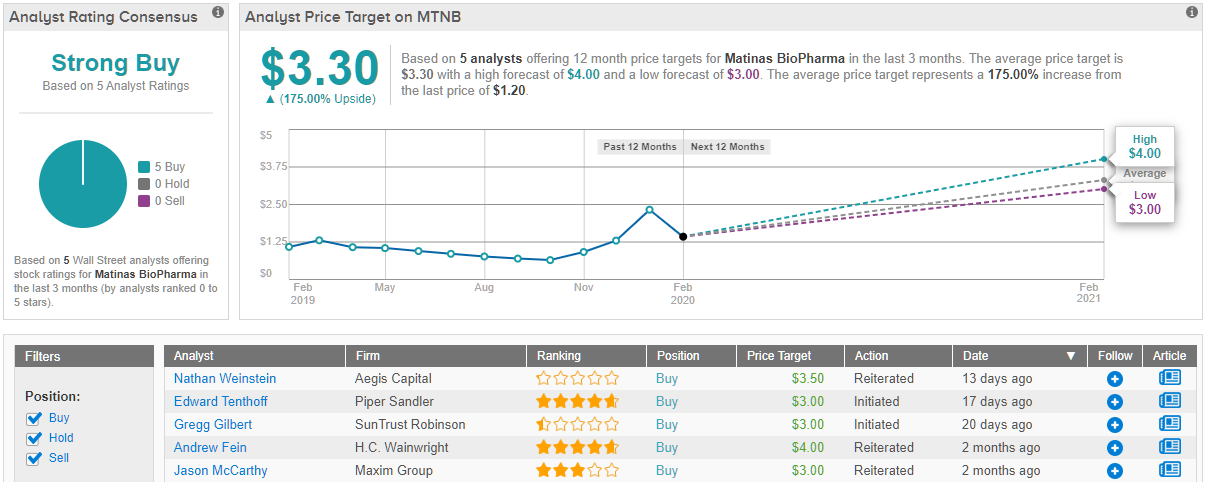

Matinas BioPharma Holdings (MTNB)

Through the development of its lead candidate, MAT9001, Matinas BioPharma wants to offer new treatments for cardiovascular and metabolic conditions. MAT9001 is an omega-3 fatty acid-based drug designed as a more effective hypertriglyceridemia treatment. With it well positioned in an expanding market, SunTrust Robinson analyst Gregg Gilbert believes that at $1.35 per share, now is the time to buy.

Despite having struggled year-to-date, investors shouldn’t panic according to the analyst. MTNB’s descent was partly related to the early success of its competitor Amarin’s Vascepa, its omega-3 fatty acid drug, as its label expansion to include cardiovascular risk reduction was just approved in December. However, Gilbert actually sees Vascepa’s launch as a positive for MTNB.

Gilbert cites the growth of the omega-3 class as the source of his optimism. Currently, there are only two prescription omega-3s to reduce triglycerides in patients with severe hypertriglyceridemia available in the U.S., Lovaza and Vascepa. As more and more research is conducted, the evidence in support of the benefits of omega-3s is mounting, implying that there’s plenty of room for MTNB to take market share.

On top of this, Gilbert points out that MAT9001 is unique in that it contains EPA and DPA in free fatty acid form and is highly bioavailable. Based on early clinical data, the drug’s composition has been shown to produce substantial reductions in lipid markers and higher bioavailability compared to Vascepa. “While a few years from market, we believe MAT9001 could carve out a nice slice of the omega-3 market given its unique characteristics,” the analyst commented.

While noting that it’s difficult to gauge the size of the omega-3 market, about 4 million patients are candidates for Lovaza or Vascepa based on the indication for severe hypertriglyceridemia. With the recent expansion of Vascepa’s label, the opportunity could be further expanded.

All of the above prompted Gilbert to kick off his MTNB coverage by issuing a bullish call. At his $3 price target, shares could be in for a 122% gain over the next twelve months. (To watch Gilbert’s track record, click here)

What does the rest of the Street think? As it turns out, all 5 of the analysts that have published a recent review see the stock as a Buy, making the consensus rating a unanimous Strong Buy. Adding to the good news, the $3.30 average price target indicates 144% upside potential. (See Matinas BioPharma price targets and analyst ratings on TipRanks)

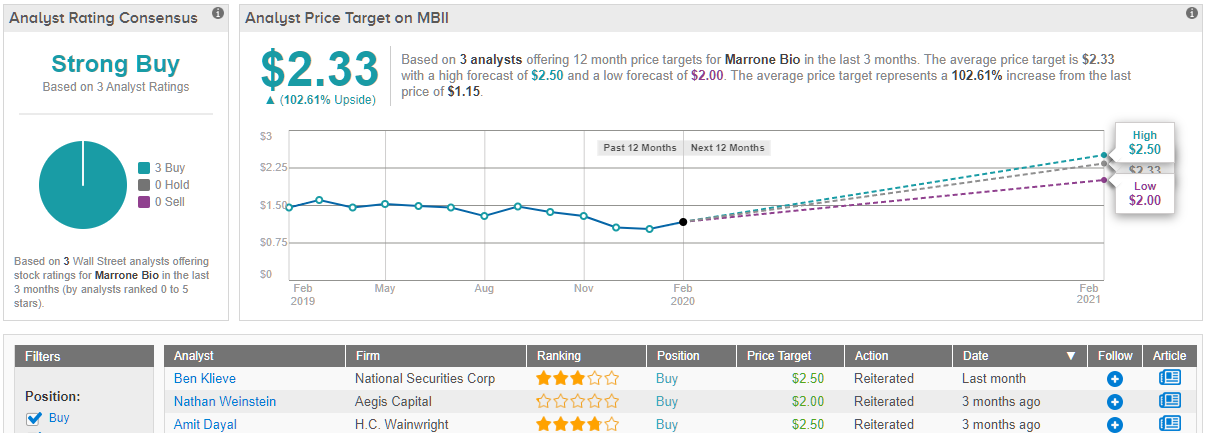

Marrone Bio Innovations (MBII)

For Marrone Bio, sustainability is the name of the game. The company uses microorganisms isolated from samples collected from flowers, insects, soil and composts to find effective solutions for pest management and plant health. Currently trading for $1.14 per share, some argue that this price can only go up from here.

During the first three quarters of 2019, the company was able to report revenue growth of 46% year-to-date. However, its disappointing bottom line results have worried investors. Even with the revenue gains, earnings haven’t improved. That being said, National Securities analyst Ben Klieve thinks that MBII’s financials are in for a change. He cites its investments in several growth initiatives as potentially fueling reductions in adjusted EBITDA losses.

Additionally, Klieve highlights the improvements in both gross margins and gross profit and new collaborations with Corteva and Compass Minerals as being encouraging signs. “We believe this momentum can continue into the fourth quarter and carry into 2020. With organic growth being supplemented by the acquisition of Pro Farm, we expect revenue growth can again approach 50% in 2020 with continued progress in gross margins,” he explained.

Based on the company’s efforts to drive a turnaround, Klieve kept both his Buy rating and $2.50 price target as is. This implies that shares could climb 119% higher in the next twelve months. (To watch Klieve’s track record, click here)

Meanwhile, Amit Dayal of H.C. Wainwright points to the EPA’s recent approval of two of its biofungicide products, Stargus and Regalia, for use on hemp plants as reaffirming his bullish thesis. Since 2018, no other crop protection products have been given the thumbs up for use on hemp. Not to mention the company estimates the hemp market in 2018 reached over $1.1 billion and could more than double by 2022.

“We believe that being the first company with EPA approved crop protection products for use in hemp–in addition to these products being bio-based–affords Marrone a significant competitive advantage,” Dayal commented. Thanks to this development, the analyst reiterated his bullish call. At $2.50, his price target mirrors Klieve’s. (To watch Dayal’s track record, click here)

When it comes to other analyst activity, it has been relatively quiet on Wall Street. The two analysts above have published the only recent reviews, making the consensus rating a Moderate Buy. (See Marrone Bio stock analysis on TipRanks)

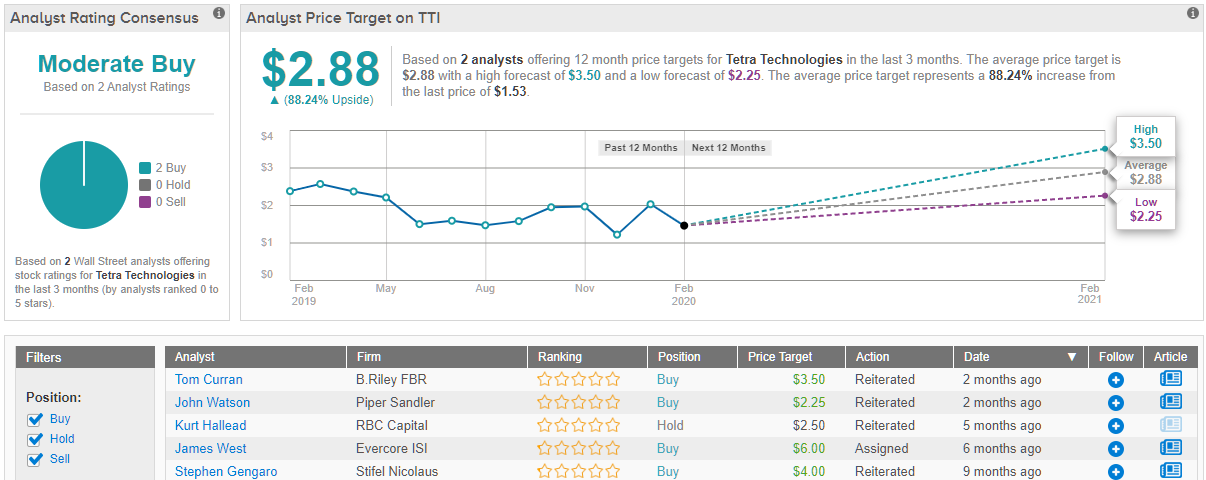

TETRA Technologies (TTI)

Switching gears now, TETRA provides the upstream energy industry with solutions for completion fluids and water management as well as offers various compression services. According to one analyst, its price tag of $1.51 a share is a steal.

B.Riley FBR’s Tom Curran does acknowledge that its onshore NAM OFS businesses, especially water and flowback’s services in the Permian, continue to face challenges, and its long-term hydrochloric acid (HCI) supply agreement impacts the value of its mechanical evaporation (ME) plant in the near-term. Having said that, he argues TTI has a lot going for it. During a recent conference, management stated that the operator who awarded it the CS Neptune project should have started completions activity during Q4 2019, beginning the consumption of product under the contract.

Curran argues that this would be a huge step forward, writing, “Although there is a real possibility that the completion phase did not start until later in 4Q19 and could spill over into 1Q20, we believe that the mere commencement of Neptune sales under this contract should be a significant positive for both TTI’s stock sentiment and fundamental story, especially since the product is so lucrative that even a modest amount of revenue recognition should have a pronounced impact on the division’s margin.”

He concluded by noting, “We continue to like TTI’s cheap valuation, which we suspect is partly due to misperceptions about TTI-only’s actual debt burden; Completion Fluids division’s promising CS Neptune product suite and structurally increasing profitability; and Water & Flowback division’s potential to significantly rebound as competitive improvements converge with a cyclical upswing.”

To this end, Curran maintained a Buy recommendation. Despite reducing the price target from $3.75 to $3.50, he still believes a 132% twelve-month gain could be in store. (To watch Curran’s track record, click here)

Looking at the consensus breakdown, only one other analyst has thrown an opinion into the mix. However, the rating was also bullish, making the Street consensus a Moderate Buy. While lower than Curran’s forecast, the $2.88 average price target still suggests huge upside potential of 91%. (See TETRA stock analysis on TipRanks)