Netherlands-based ASML (NASDAQ: ASML) is at the forefront of the semiconductor industry and is of paramount importance to the West and its allies. The company’s photolithography systems, which are essential for the production of semiconductors, have placed it in a unique position in today’s geopolitical landscape. In light of this, it’s no surprise that ASML’s shares trade at a premium valuation.

The Critical Role of Semiconductors and ASML

In simple terms, ASML is pretty much the only player in the field of EUV lithography systems, the most advanced technology in the semiconductor industry. It operates a natural monopoly.

This makes ASML a vital partner for every semiconductor manufacturing company that aims to stay ahead of the curve and maintain its competitiveness. In a world where technology is advancing at an unprecedented rate, a partnership with ASML is a must for any semiconductor manufacturer who wants to stay ahead of the game.

However, it’s not just the industry that recognizes the importance of ASML’s technology – countries around the globe have realized the impact semiconductors have on their economies and defense capabilities. Investing heavily in the development of these technologies, countries such as the United States, China, and South Korea, have all set their sights on securing access to ASML’s state-of-the-art systems, the key to unlocking the next generation of semiconductors.

The intriguing part is that with this level of importance comes tension and concerns over trade and national security. Not having access to ASML’s systems means falling behind in the global race for technological advancement. It’s a high-stakes game, and countries are pulling out all the stops to gain an edge. Hence, ASML is not just a leader in the semiconductor industry but also a key player in the geopolitical arena.

Also, if you think this just plays out on a theoretical level — with China gradually escalating its threats regarding a potential invasion of Taiwan –Washington has been consistently trying to convince the Dutch to ban ASML from selling its best chipmaking equipment to China.

But why should you care about any of that? Because this whole situation translates to massive leverage in favor of ASML, including the company retaining fantastic pricing power, further growing its ever-expanding backlog, and its shares retaining a pricy premium, which can be a great trait during an uncertain market environment.

ASML’s Q4 Results: Highlighting the Company’s Unstoppable Momentum

Despite fears of the global economy slowing down, which one would expect to affect semiconductor sales negatively, given their cyclical nature, ASML’s momentum appears unfazed as demand for its critical technology remains as high as ever.

ASML just ended its Fiscal 2022 with extreme confidence, as Q4 revenues landed at €6.4 billion, up 28.5% year-over-year. The company had an outstanding performance with net bookings of €6.3 billion, indicating that it is well-positioned for continued success in the next few quarters, with no unexpected downturns in sight. This is because strong bookings make for an accurate indication that the company is on the right track moving forward.

As far as its profitability goes, ASML posted a net income of €1.82 billion, only significantly higher than €1.77 billion in last year’s Q4. That said, management expects that the company will deliver net sales growth of more than 25% in Fiscal 2023, which will come with an improvement in gross margins relative to last year.

The significant revenue growth, along with an expansion in margins and ASML’s underlying share repurchases, should boost earnings per share significantly next year. This is reflected in consensus estimates for Fiscal 2023, which point toward earnings per share of €22.35, implying a year-over-year increase of about 44% relative to Fiscal 2022.

Is ASML Stock a Buy, According to Analysts?

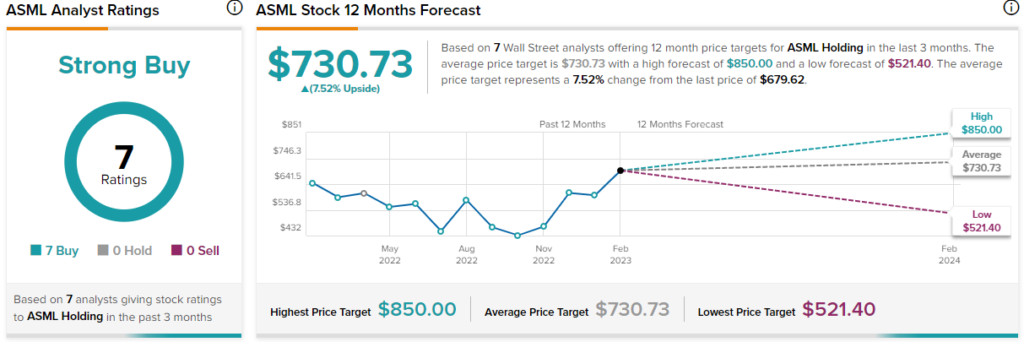

Regarding Wall Street’s view on the stock, ASML Holding has a Strong Buy consensus rating based on seven unanimous Buys assigned in the past three months. At $730.73, the average ASML stock price prediction implies 7.5% upside potential.

Takeaway: ASML’s Premium Valuation Should be Sustained

In conclusion, ASML’s increasing importance makes it a much sought-after holding in investors’ portfolios. The ever-expanding demand for more efficient semiconductors was reflected in the company’s Fiscal 2022 results, as well as in its outlook for fiscal 2023, which suggests no slowdown in its top and bottom line growth as we advance.

As a result, even though the stock’s forward P/E of about 34x appears to be quite pricy given the cyclical nature of the semiconductor industry, ASML’s unique position in the space and critical nature as a geopolitical asset should be sufficient catalysts when it comes to shares retaining their premium valuation.

Management’s long-term guidance, which projects revenues reaching somewhere between €44 billion and €60 billion by 2030, with gross margins between approximately 56% and 60%, should also justify a P/E in the low 30s given the upcoming, rather predictable growth to be realized in the coming years.