The last few trading days, which have seen some of the worst market losses of the 2000’s, bring up some serious questions for investors. The stock markets reached record-high level in recent weeks, raising concerns about bubbles. Are these sharp drops just a correction, as buyers cash in their profits? Or is the market reacting to the coronavirus outbreak, and the chance that a global pandemic won’t just disrupt trade and travel but also break the Chinese economy and spark a global recession?

These are some of the questions on investors’ minds, and there may be no easy answers. So, it’s natural at times like this to turn to the financial experts – traders who’ve risen to prominence through long-term success in the markets. Leon Cooperman, of Omega Advisors, has been just such a market force for decades, and has built his firm into a multi-billion-dollar behemoth. He recently spoke up about the near- and mid-term prospects for the markets.

First, Cooperman sees the current slips as essentially beneficial for the markets. Even though the Dow and S&P have both seen their highest point-drops ever, the markets actually not even close to recession territory. Cooperman says, “The correction is healthy for the market. Even though I’ve lost a ton of money.” He added his view that the viral outbreak will likely taper down by June, and that with stock prices down now, investors have an opportunity to buy in at discount prices.

We’ve taken three of Cooperman’s recent investments and looked them up in the TipRanks database. These are investments that the Stock Screener tool reveals as ‘Strong Buy’ rated and, more importantly, all three have a clear positive upside potential for the near future. Let’s dive deeper, to find out what those analysts have to say.

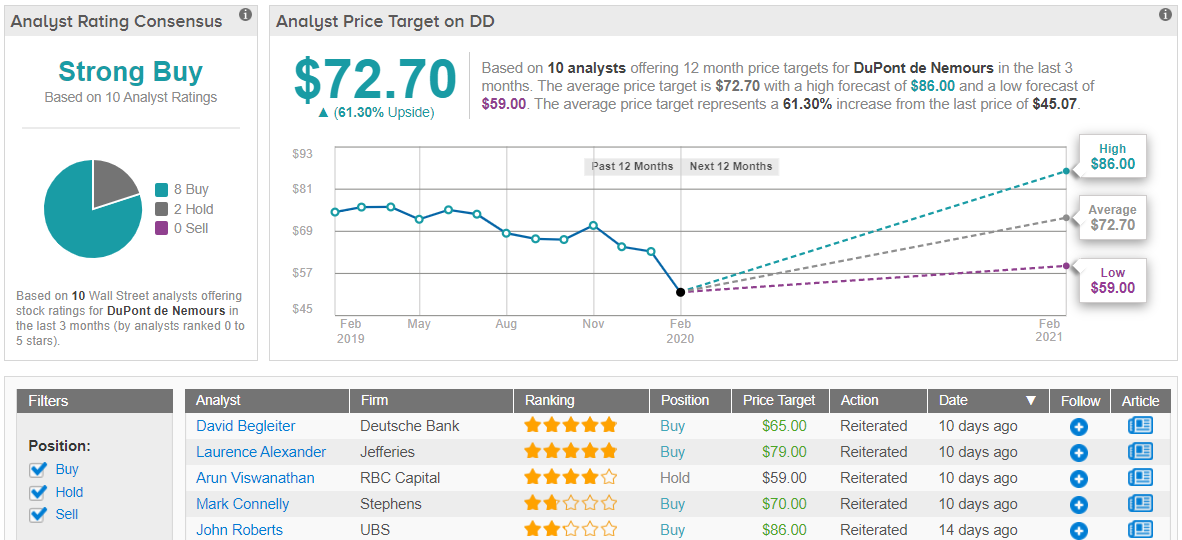

DuPont De Nemours (DD)

The first Cooperman buy that caught our attention is the largest player in the US chemical manufacturing industry. Dupont is a famous name, dating back to the early 1800s. The company’s products have applications in a wide range of industry and manufacturing, including electronics, transportation, biosciences, and construction. DuPont’s adhesives, fluids, reinforcing composites, foams and coatings, rubber and elastomers, and synthetic fibers are found throughout the economy.

A stable stock, from a company with a sound footing, offering steady dividend returns, is practically a poster child for defensive investing – and Cooperman bought up 426,335 shares in Q4. That more than doubled his shares of DD, a stock which he has held since Q3 2017. Cooperman’s recent purchase in DuPont is now worth over $19 million, and his total holding in the stock is valued at $35.7 million.

Analyst John McNulty, of BMO Capital, is bullish on DuPont’s near-term prospects, writing, “Following what has been a choppy run for DD over the past eight months… In addition to maintaining focus on portfolio optimization, we believe the move is to enhance the attention to operational excellence, return DD to growth, and ensure the company delivers on its targeted goals.”

McNulty gives DD shares $82 price target and a Buy rating. His target suggests an upside of 81% for the stock – plenty of potential to attract investors. (To watch McNulty’s track record, click here)

Weighing in from Deutsche Bank, 5-star analyst David Begleiter focuses on recent top-management churn at the company, saying, “We view the firing of DuPont’s CEO and CFO and the return of Ed Breen as CEO as a slight positive… The changes are being made to accelerate operational performance improvement and to more directly tap Mr. Breen’s significant management experience.”

Given his optimistic view of the new leadership, Begleiter rates DD shares a Buy, with a $65 price target and a 44% upside potential. (To watch Begleiter’s track record, click here)

Overall, the analyst consensus on DD is a Strong Buy, based on 8 Buy ratings and just 2 holds. Th stock is selling for $45.07, and the average price target of $72.70 suggests an upside of 61%. (See DuPont stock analysis at TipRanks)

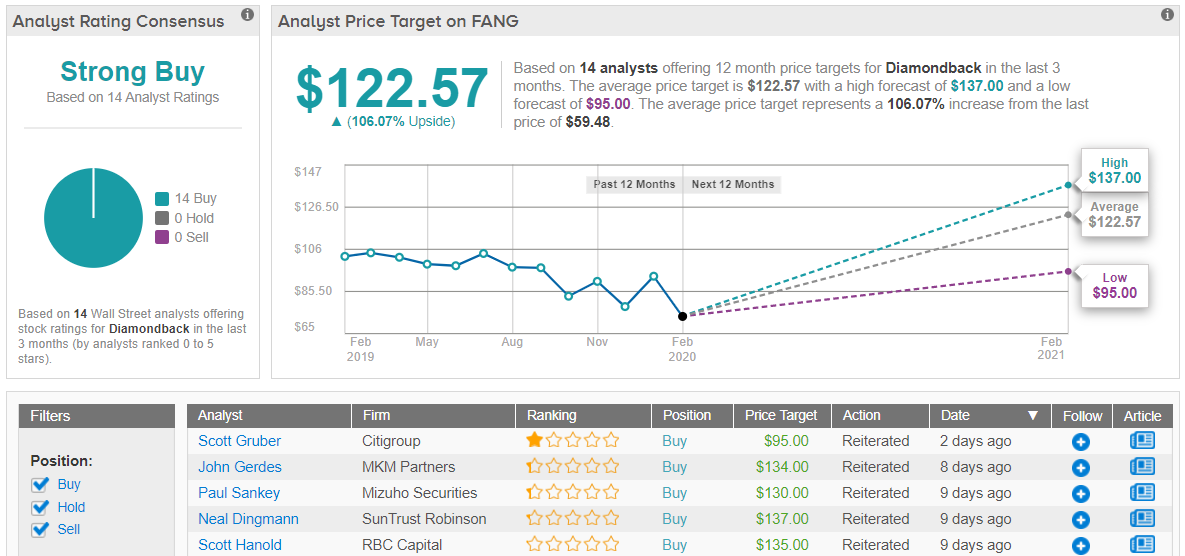

Diamondback Energy (FANG)

Next up is a Texas oil company. Diamondback is part of the Permian Basin oil boom that has energized the Texas economy and helped make the US a net exporter of crude oil and oil products. Diamondback is an oil exploration and drilling company, and produced over 130,000 barrels of oil equivalent per day. With a market cap of $9.4 billion, Diamondback is considered a mid-size player in the oil industry.

Like many of its peers and competitors, FANG tried to compensate for low oil prices with increased production – and in Q4 it succeeded. Earnings for the final quarter of CY2019 came in at $1.93, well above the $1.80 estimate. Revenues gave an even better print, growing 74% year-over-year and beating the estimates to reach $1.104 billion.

The strong earnings prompted company management to announce an increase in the dividend, raising the quarterly payment from 19 cents to 38 cents. Annualized at $1.52, this gives a yield of 2.4%, comparing well with the 2% average among S&P listed companies. And at 19%, the payout ratio indicates no difficulties for the company in maintaining the payments.

Cooperman is familiar with FANG’s strengths and potential. His Q4 stock purchases, of 200,000 shares, doubled his holding in the oil producer, and his total stake, 400,000 shares, is now worth $23.8 million. When the new dividend is paid out in March, Cooperman stands to earn $152,000.

Wall Street also likes FANG stock. Imperial Capital analyst Jason Wangler writes of the stock, “The company intends to see continued cost improvements, improved oil realizations, and production growth during 2020 which should drive free cash flow from operations used to help fund its recently-increased dividend program as well share repurchases when appropriate. Excess cash generation can also help strengthen FANG’s balance sheet… We believe this balanced approach should help drive shareholder value going forward.”

Wangler’s Buy rating is supported by his $110 price target, which suggests an impressive growth potential of 84%. (To watch Wangler’s track record, click here)

Also bullish is Michael Glick, from JPMorgan. Glick puts an aggressive $139 price target on this stock, indicating the extent of his confidence: a 133% upside potential.

Glick writes, in his comments on FANG, “We also note FANG TIL’ed more wells than our model, which should allow for continued growth in 1Q. Overall, we think the positives (magnitude of dividend, TSR focus and Midland inventory growth) outweigh the negatives (4Q capex, slightly higher unit costs in 2020 versus our model) here.” To watch Glick’s track record, click here)

FANG shares have 14 recent Buy-side ratings, making its analyst consensus a unanimous Strong Buy. Shares are selling for a bargain, especially for a stock with such a high potential: the $122.57 average price target suggests a 106% upside potential from the current trading price of $59.48. (See Diamondback’s stock analysis at TipRanks)

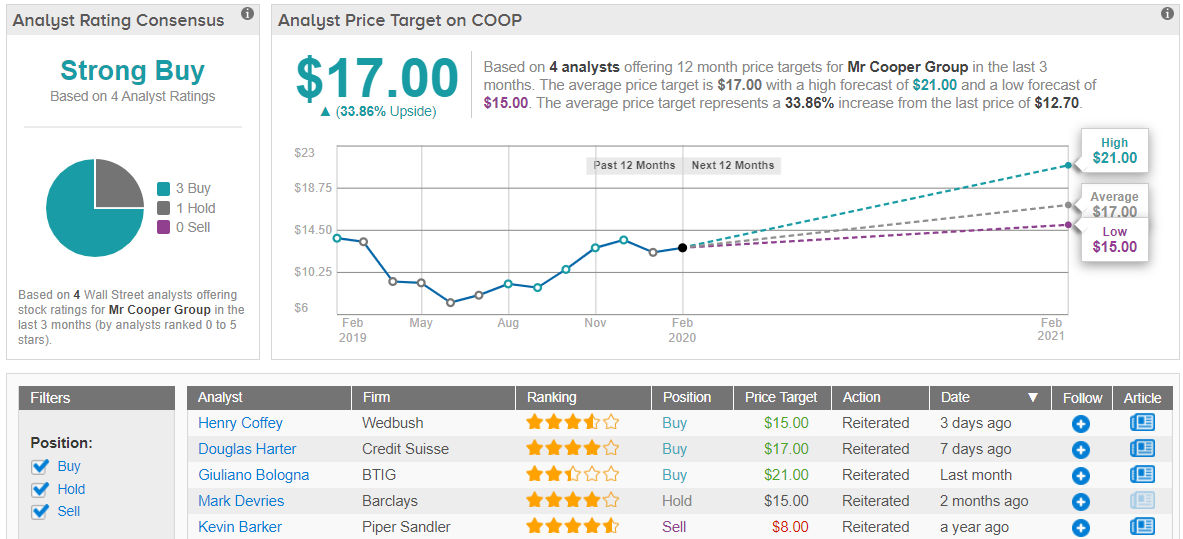

Mr. Cooper Group (COOP)

Last on our list today is a mortgage service company, operating in the single-family residence market in the US. Mr. Cooper Group bills itself as one of the country’s largest home loan providers, and boasts a market cap of $1.16 billion. Since bottoming out last June, COOP shares have gained 86%.

Of the stocks on this list, COOP is the only one not to offer a dividend – but it has shown the strongest share appreciation, and the company’s earnings were net-positive through all of 2019. In Q4, COOP reported $1.03 per share, beating the 67-cent estimate by 53%. Revenues also beat the estimates; the $618 million print was 13% better than the forecast. The quarterly report, and positive performance of the company through 2019, shows that Mr. Cooper Group has successfully navigated the low-interest rate regime in the US mortgage industry.

Cooperman’s purchase of this stock totaled 928,427 shares, increasing his holding by 92% to a total of 1,932,027. Cooperman has held a stake in this company since Q3 2018, and his current stake is worth $24.5 million.

Douglas Harter, a 4-star analyst with Credit Suisse, writes of COOP stock, “While the decline in rates have negatively impacted servicing profitability, the improved performance in originations will result in higher near-term operating earnings and only a modest decline in book value.”

Harter puts a Buy rating here, and supports it with a $17 price target. His target implies an upside potential of 33%. (To watch Harter’s track record, click here)

All in all, COOP shares have 3 Buy ratings against 1 hold, giving the stock a Strong Buy from the analyst consensus. Shares are selling for $12.70, and the average price target, $17, matches Harter’s. The Street sees room for 34% upside growth in this stock. (See Mr. Cooper Group’s stock analysis at TipRanks)