For those who like patterns, biotech names’ growth stories tend to look remarkably similar. These stocks are less reliant on earnings reports and more on a few select markers which can decide what direction they will take in the near-term. A favorable outcome from a regulatory committee or promising data from a clinical trial can send the stock soaring. Conversely, rejection or disappointing readouts can send the company’s share price tumbling down. While they present possible mercurial upside, these tickers aren’t for the faint of heart because although the patterns usually play out, the direction they might take is very hard to predict.

So, how should investors choose which biotechs to invest in? There are different strategies, of course, but one trusted way is to listen to the experts. Investment bank BTIG is a well-known name on the Street, housing several top analysts. The company has identified three companies in the sector that will present new data over the coming months, and BTIG analysts think positive results can propel each of them forward.

Using the Stock Comparison tool from TipRanks, a company that tracks and measures the performance of analysts, we were able to zero in on their choices and find out why the firm finds them so compelling. Let’s get familiar with the data at hand.

Sarepta Therapeutics (SRPT)

Let’s start off with a good example of the impact regulatory forces can have on a stock. Sarepta Therapeutics made headlines towards the end of 2019, when the FDA approved Vyondys 53, the company’s treatment for Duchenne muscular dystrophy (DMD) patients with exon 53 mutations. The approval came as a surprise as only a few months earlier, Sarepta received the dreaded CRL (complete response letter) from the FDA following its original submission. As is de rigueur in the sector, Sarepta stock responded to the announcement by soaring over 30% in a day.

In addition to the recently approved drug, the genetic disorder-focused biotech has a robust pipeline, with gene therapy programs in DMD and LGMD (Limb Girdle Muscular Dystrophy). BTIG’s Tim Chiang believes the company is steadily progressing with these key programs.

The analyst said, “We believe SRPT is making progress on the gene therapy manufacturing front, and has achieved yields sufficient to begin study 301 (which we think could enroll up to a hundred or more patients). We believe SRPT plans to provide an interim look at data from this study in ~15 patients dosed (evaluating expression levels at ~3 months post dosing). In LGMD2E, SRPT has dosed two patients in the higher dose cohort, with a third patient to be dosed shortly. We expect a data read out from this high dose arm in early 2Q.”

Chiang expects that US gene therapy sales in the DMD market will reach a peak in 2024, with the figure landing at roughly $2 billion. There are three companies currently in the race to develop gene therapies for the treatment of DMD; Sarepta, according to the analyst, is leading the way and could be the first to enter the US market with its gene therapy for DMD in the second half of 2021.

Chiang added, “We think one of the key differences among the 3 micro-dystrophin gene therapy programs in the clinic are that both Solid Biosciences (SLDB, Neutral) and Pfizer have studies where ascending dose cohorts are being utilized. In contrast, Sarepta’s study incorporates just one dose (2E14 vg/kg).”

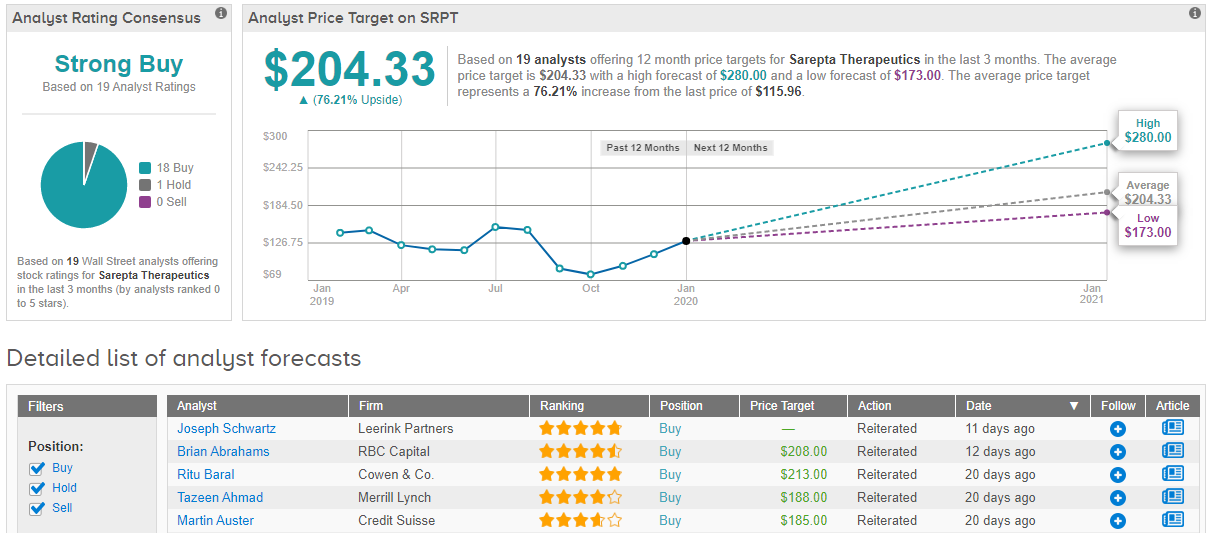

So, what does this mean? It means Chiang kept his Buy rating on Sarepta, along with a price target of $190. Should the target be met, investors stand to see a handsome 64% gain over the next year. (To watch Chiang’s track record, click here)

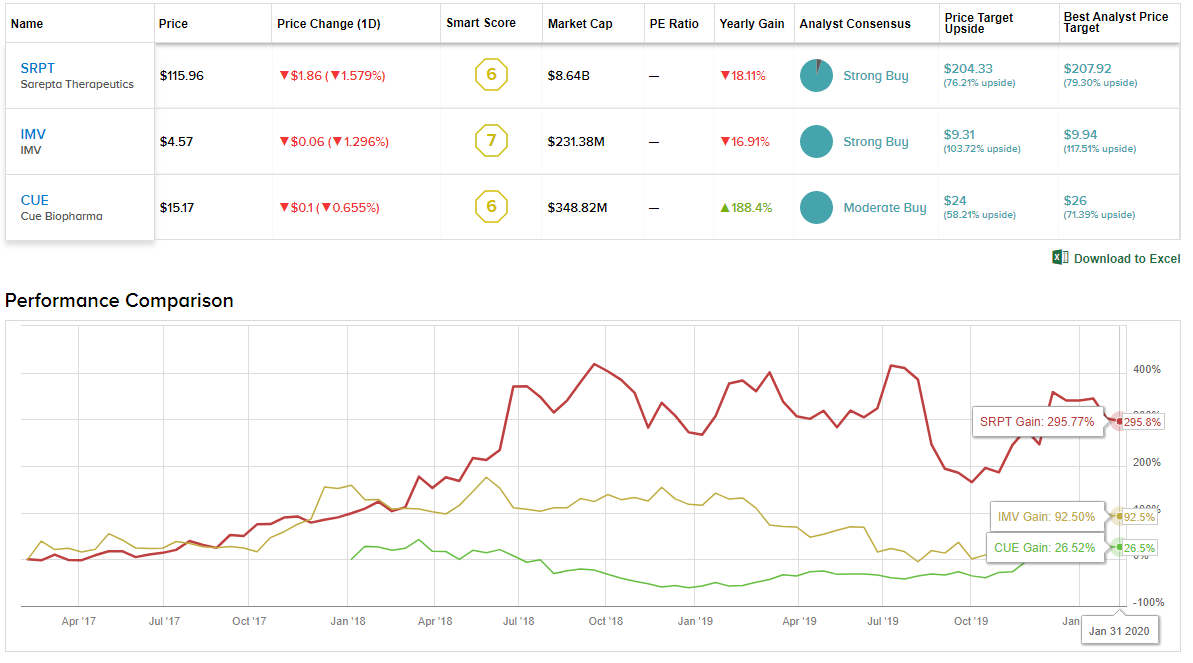

The Street, too, is bullish on the DMD fighter. A Strong Buy consensus rating breaks down into 18 Buys and a single Hold. The average price target comes in at $204.33 and indicates potential upside of 76%. (See Sarepta stock analysis on TipRanks)

IMV Inc. (IMV)

IMV’s market performance in 2019 was a disappointing affair; The stock lost 39% of its value along the way. By contrast, 2020’s performance so far has been the exact opposite – and some. The stock is up by 58% year-to-date. According to BTIG’s Thomas Shrader, there is more to come, too.

The cancer fighter’s lead candidate is DPX-Survivac, which targets the surviving TAA (tumor associated antigen) that is overexpressed in more than 20 different types of cancers. Clinical data so far has been promising, with long disease-free intervals in the ovarian cancer (OC) adjuvant setting and compelling treatment response rates in both OC and DLBCL (diffuse large B-cell lymphoma). Important DPX-Survivac data is expected this quarter which Shrader notes “could greatly de-risk the current programs and potentially demonstrate the utility of the low-COGS DPX platform to deliver many other TAAs and neoantigens.”

The 5-star analyst added, “The drug has shown robust and prolonged CD8 TCell responses in the adjuvant setting and a Phase 1b/2 trial has shown a 100% DCR and 60% ORR in the subgroup of patients with non-bulky disease (tumor burden < 5 cm) most of which are platinum-resistant (few treatment options). The company expects to provide topline Phase 2 monotherapy data in mid-February 2020 that we expect to be an important catalyst for the story.”

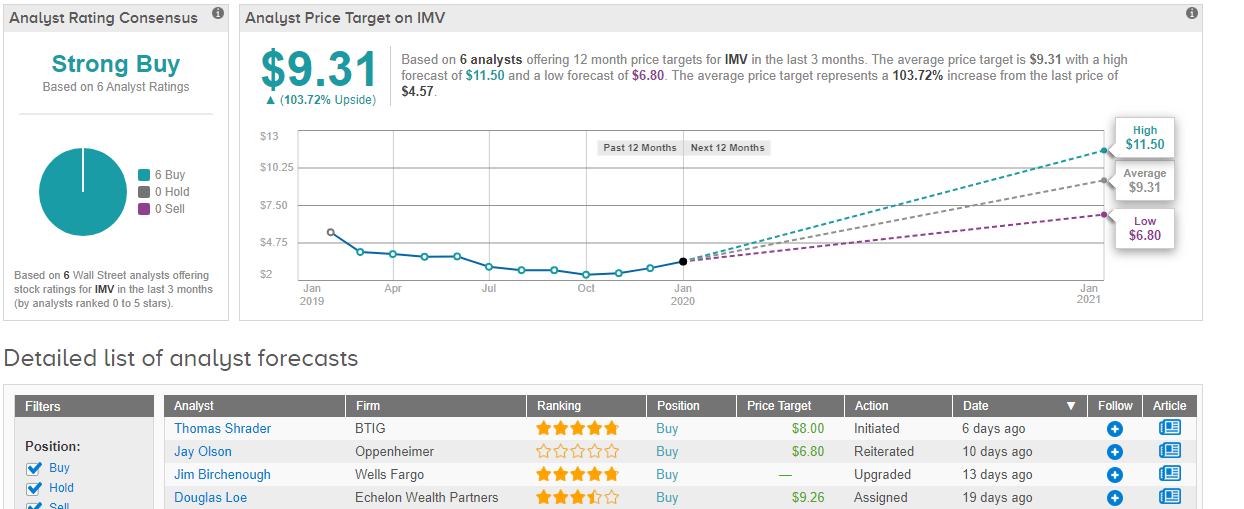

Ahead of this upcoming data readout, Shrader is siding with the bulls. The analyst initiated coverage of IMV with a Buy rating along with an $8 price target. The implication? Further gains in the shape of 75% over the next 12 months. (To watch Shrader’s track record, click here)

The Street agrees. A total of 6 Buys add up to a unanimous Strong Buy consensus rating. With an average price target of $9.31, the analysts see potential upside of 104% for IMV over the coming 12 months. (See IMV stock analysis on TipRanks)

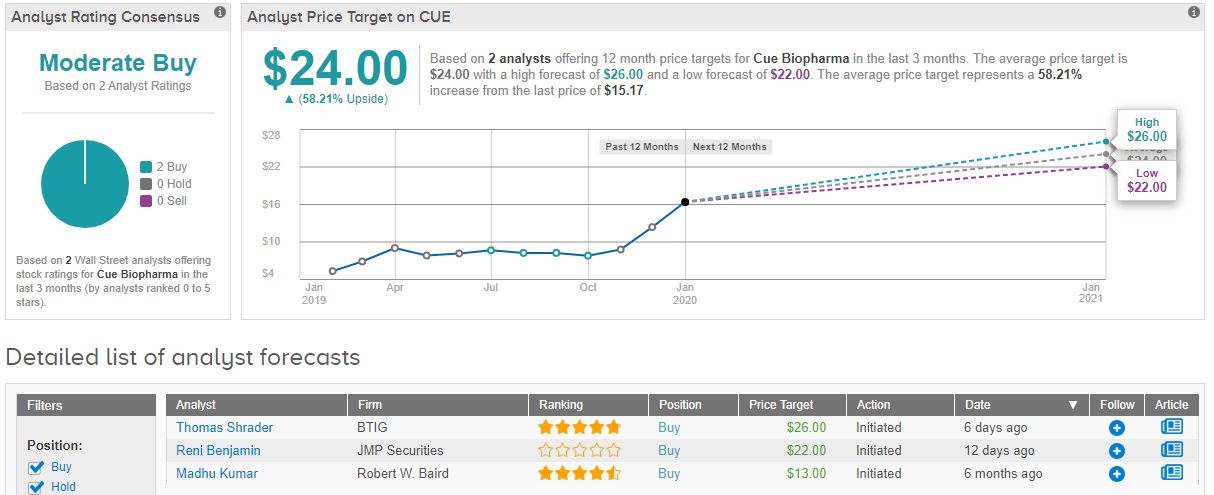

Cue Biopharma Inc. (CUE)

A fellow company taking the fight to cancer is Cue Biopharma. In 2019, Cue’s exceptional performance beat the market considerably. The stock added an astounding 238% to its share price throughout the year. Following such a surge, though, is this the right time to get in on this high-flying biotech?

Yes, it is, according to BTIG’s Thomas Shrader. In fact, the 5-star analyst just recently initiated coverage of Cue with an emphatic Buy rating. The thumbs up comes with a price target of $26, indicating Shrader believes an additional 71% will be added to Cue’s share price over the next 12 months.

So, what’s all the fuss about, then? A cure for cancer is one of modern medicine’s most coveted prizes. Cue is working on an immunotherapy platform which will assist immune systems by recognizing solid tumor cells and repeatedly attacking them until they stop working.

The company’s lead candidate is CUE-101, which was developed for patients with head and neck cancer driven by human papillomavirus (HPV). Topline results from a Phase 1 trial are expected later this year, and so far, results have been promising.

Shrader said, “Data to date is preclinical but the lead programs termed CUE-101 has exploited well defined subunits and demonstrated tumor antigen-specific T-cells responses without the accompanying systemic immune toxicities that characterize many competing approaches… Preclinical data confirm both robust T-Cell responses and an attractive safety profile setting the stage for clinical studies. These studies have stated (first dosing September 2019) and, based on the preclinical safety profile, will begin with doses that could be efficacious. Clinical data validating the overall approach are expected around 3Q20 and, if promising, a significant pipeline in additional applications should be de-risked.”

Currently, the rest of the Street remains rather quiet on Cue, with only one other analyst chipping in with a take on the biotech’s prospects. The additional Buy recommendation means Cue receives a Moderate Buy consensus rating. The average price target comes in at $24 and implies upside potential of 58%. (See Cue Biopharma stock analysis on TipRanks)