Most of the FAANG family are reporting earnings this week, in a macro environment no one would have expected at the start of the new decade. The Street, and investors alike, will be extra keen to see the viral outbreak’s influence on the mega caps’ top and bottom lines.

Social media giant Facebook (FB) will be in the spotlight when it reports first-quarter results this afternoon. As the countdown to Facebook earnings starts, Wall Street’s confidence backing the stock is strong.

5-star Merrill Lynch analyst Justin Post believes Facebook will “meet or beat lowered Street estimates.” Key areas of focus for Post are advertising revenue growth and user growth and engagement. This is hardly surprising, as the two areas have been impacted the most by COVID-19, though each in the opposite direction.

“While user activity is higher across Facebook/Instagram/WhatsApp platforms, we expect pressure on ad spending, reflecting large GDP declines. Street seems prepared, Bloomberg consensus is at $17.3bn (+15%) which suggests about a 810% y/y decline in revenues in last 3 weeks of March (assuming 22% growth in first 10 weeks),” Post noted.

Expenses wise, the analyst doesn’t see Facebook pulling back as much as Google (FB announced plans to hire 10,000 new employees this year. Google’s objective of 20,000 new additions to the workforce are expected to be shelved to rein in spending). Although some areas will probably see a reduction in marketing spend and investments.

Looking ahead to Q2, Post expects ad business to drop by 5 to 10% year-over-year and forecasts revenues to “decelerate materially” along with GDP in the next quarter. Although the negative outlook is tempered somewhat on account of Snap’s recent earnings results, which indicated ad spend had stabilized following March’s sharp drop. The anticipated lack of pullback on expenses could lead to “margin pressure” but might also suggest “relative revenue resiliency.” Moreover, the lack of spending restraint might indicate Facebook “sees big opportunities ahead.”

Overall, Facebook’s “long-list of future revenue drivers,” keeps Post in a buoyant mood. Accordingly, ahead of the print, the analyst keeps his Buy rating intact, along with a $200 price target (To watch post’s track record, click here)

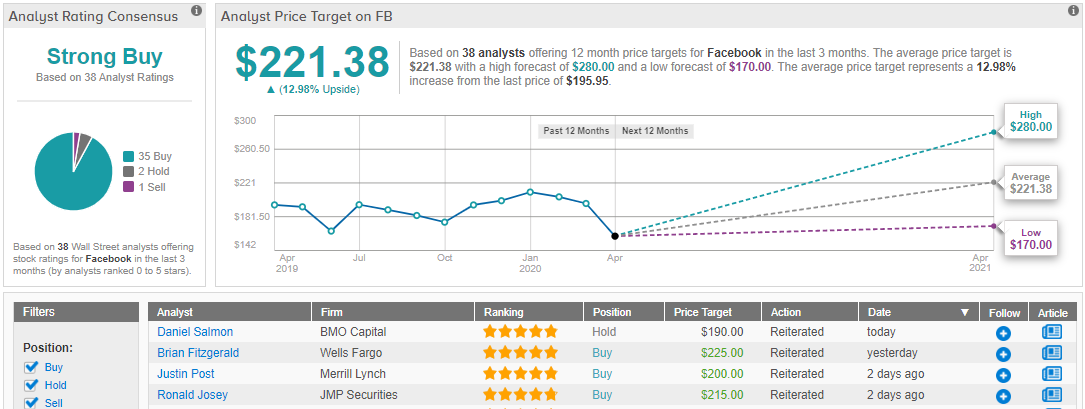

Overall, Wall Street analysts tend to side with Post’s bullish perspective on the social media giant’s stock. Out of 38 analysts tracked in the past 3 months, 35 are bullish, while 2 remain sidelined, and only 1 is bearish. The 12-month average price target of $221.38 boasts potential upside of 13% from current levels. (See Facebook stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.