While COVID-19 has sent investors of badly hit industries – travel, aviation, food service, oil – to the exit doors, industries catering to “stay at home” needs have flourished. Video conferencing, gaming, cloud services – have all befitted from the forced enclosures. But one particular segment has remained somewhat under the radar.

Online education specialist Chegg (CHGG) reported earnings yesterday and Wall Street was impressed, to say the least. Shares popped by 32% and shone a spotlight on the remote learning industry.

In the first quarter, Chegg’s revenue increased by 35% year-over-year to $131.6 million, well ahead of the Street’s call for $122.7 million, while adjusted earnings of $0.22 per share soared 40% year-over-year to easily beat the consensus estimates of $0.16 EPS. The company’s services segment grew by 33%.

Chegg is expecting a strong second quarter, too, forecasting subscriber growth to increase by 45%.

Although Chegg is most famous for its college textbook rental service, only 20% to 25% of the company’s revenue is derived from the segment.

Chegg’s services division plays a much larger role, assisting students’ studies in various subjects, and providing online tutoring for those who require a more personal approach. As such, the coronavirus has played right into Chegg’s hands. With school interrupted across the globe, Chegg has been able to step into the fold and supplement students with additional remote learning.

Barrington analyst Alexander Paris is impressed with the performance and expects “accelerated growth.”

The analyst said, “Chegg is currently trading at 9.7x and 7.9x our 2020 and 2021 revenue estimates, a premium to its Ed Tech peers, which average 3.7x and 3.2x, and its vertical-focused SaaS peers, which average 7.3x and 6.4x, respectively. We feel the premium valuation is justified, given its sustainable, above-average revenue growth rate (vs. both peer groups) and high and rising profitability, combined with a balance sheet including more than $1 billion in cash to finance further growth initiatives including strategic acquisitions when the time is right.”

Paris maintains an Outperform rating on Chegg shares, whilst the price target gets a boost – up from $50 to $60, which implies a slight downside. (To watch Paris’s track record, click here)

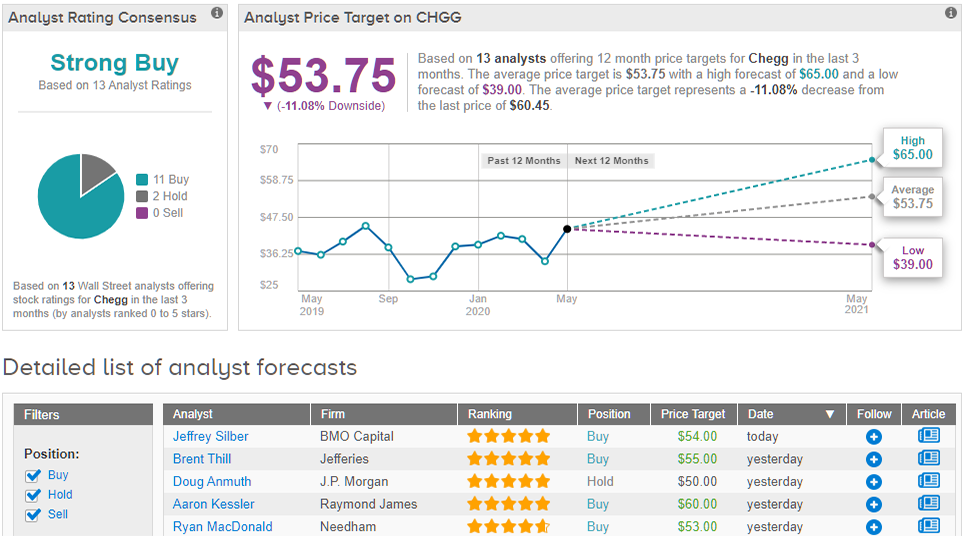

Turning now to the rest of the Street: Chegg’s Strong Buy consensus rating is based on 11 Buys and 2 Holds. The average price target, though, comes in at $53.75 and implies downside of 11% — most likely a result of yesterday’s quick surge and analysts’ inability to turnaround new price targets so quickly. (See Chegg stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.