Canoo Inc. (GOEV) is a Los-Angeles based mobility technology firm focused on designing, engineering, developing, and manufacturing EVs for both commercial and private purposes. The company uses skateboard architecture technology to manufacture B2B delivery vehicles and lifestyle vehicles along with multipurpose delivery vehicles in the United States. Canoo’s modular electric platform is built to deliver maximum interior space in vehicles.

Additionally, the company includes a range of vehicle applications for both businesses and individuals. These factors have made Canoo an intriguing speculative bet in the EV space.

Currently, I’m somewhat bearish on GOEV stock. (See Canoo Inc. stock charts on TipRanks)

Volatile EV market

One of the reasons for this stance is the volatility of the EV market. Since the onset of the pandemic, EV stocks have surged and dropped to a degree that makes many investors uncomfortable. Indeed, like other EV stocks, Canoo’s valuation has become a point of contention among bears, with bulls noting that the company’s long-term growth prospects make this valuation worthwhile.

That said, one of the key contributing factors to Canoo’s volatile nature is simply the fact that this is a de-SPAC (special purpose acquisition company) company. The SPAC space has been ultra volatile of late, due to the speculative nature of companies that choose reverse mergers to go public.

Accordingly, GOEV stock has fluctuated between a massive range of $5.75 per share and nearly $25 per share over the past year. Currently, GOEV stock is trading near the lower end of this range, as bearish sentiment on this company builds.

Can Canoo come roaring back? Or is the music starting to stop? Let’s dive in.

Key Catalysts for GOEV Stock

Perhaps the most bullish argument that can be made for GOEV stock is that this company is a potential short squeeze candidate. Simply because of the company’s short interest of late, retail investors may want to take a gamble on this stock squeezing.

Such a stance is not insane. Other companies with low share prices, high short interest and borrow fee rates, and low floats, have squeezed in incredible fashion. However, the potential for GOEV stock to pick up the momentum necessary to initiate such a squeeze appears to be the problem.

Earlier this year, GOEV stock rallied by a whopping 35%, courtesy of Reddit users bidding for short-term play. In fact, nearly 33% of the company’s floating shares were sold short.

However, since then, sentiment on platforms such as Reddit group WallStreetBets has calmed down. Investors seem more concerned with the fact that Canoo has recorded no revenue and an operating loss of nearly $97 million, per its first-quarter results posted in May. However, Canoo did get a temporary boost, as it ended the quarter with $641 million in cash and cash equivalents.

In its Q2 report, the company recorded a wider-than-expected loss in the quarter but managed to generate 9,500 non-binding pre-orders. Moreover, loss from operations is also down by 426.8% year-over-year, while total assets took a blow of over $700 million, nearly a 6% fall year-over-year. Additionally, the company’s net loss grew by approximately 385% to over $110 million.

Canoo’s EBITDA loss of around $76 million was also up from $17.7 million during the same quarter in 2020. Further, Canoo also reported negative operating cash flows amounting to $108.8 million, along with around $565 million in cash.

These are not bullish numbers at all.

The Bigger Picture for GOEV

According to Tony Aquila, CEO of GOEV, the company is planning to introduce sustainable and affordable vehicle options to the global market. This strategy takes time to enact, and investors shouldn’t focus on recent results as indicative of what the future will hold.

On the other hand, Canoo has recently made two notable moves. First, Canoo has secured a manufacturing contract with VDL Nedcar. Secondly, the company has selected Oklahoma as the partner for the manufacturing plant.

Indeed, on the production front, Canoo has sourced 87% of its components at the end of the second quarter, 13 points higher year-over-year. When bulk materials are excluded, the company has sourced 95% of its manufacturing materials. These are good signs pointing to production commencing as planned.

Canoo is set to launch its first product in 2022, which the company will follow up with multipurpose delivery vehicles, along with pickup trucks. Aquila added that the company is looking to secure the company’s future and plans to focus on the fundamentals. Further, he claims that companies and stock prices do not always factor in positive events or catalysts.

The company is in a pre-revenue state and aligned with analyst expectations of revenues, hitting the $75 million mark in 2022. This would signify a price-to-sales multiple of over 25, considering the current market cap of around $2.15 billion.

Indeed, most fundamentals-oriented investors would say that’s high. However, for a company with the growth potential of Canoo, perhaps this is reasonable. Time will tell.

What are Analysts saying about GOEV Stock?

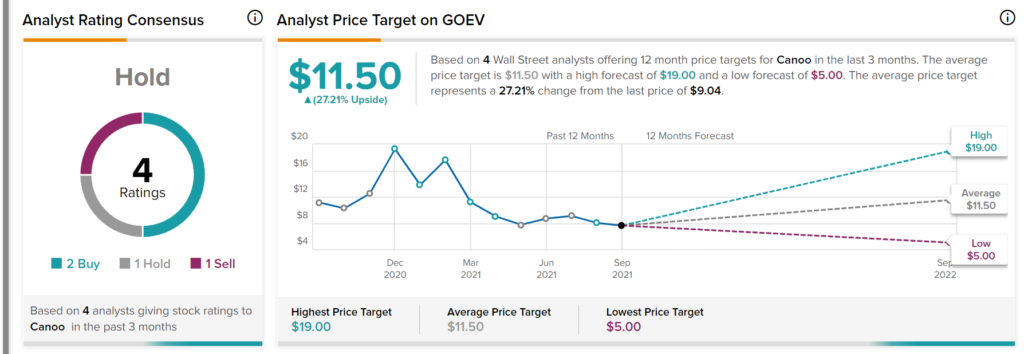

As per TipRanks’ analyst rating consensus, Canoo is a Hold. Out of 4 analyst ratings, there are 2 Buy recommendations, 1 Hold recommendation, and 1 Sell recommendation.

The stock has an average Canoo price target of $11.50, implying upside of 27.21%. Analyst price targets range from a high of $19 per share to a low of $5 per share.

Bottom Line

There’s an intriguing bull and bear case to make with GOEV stock right now. Indeed, the EV sector is seeing higher levels of competition of late, making this space a more intriguing one to watch. However, picking the winners out of this early-stage pool is rather difficult.

Canoo is an intriguing option with impressive upside, but also holds extremely high risk right now. Accordingly, investors should size their positions accordingly when considering such speculative plays.

Disclosure: At the time of publication, Chris MacDonald did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.