When it comes to the current economic landscape, you can either look at the glass half empty or half full. Driven by positive developments in the re-opening of the global economy, U.S. stock futures pointed to opening gains on Monday, but this follows the market’s first week-to-date decline in three weeks thanks to a historic drop in oil prices.

This same philosophy applies to the narrowing of market breadth, or how many stocks are participating in a given move in an index. According to Goldman Sachs US equity strategist David Kostin, the S&P 500 is 17% below its February record, but the median stock trades 28% lower than at its peak. On top of this, 20% of the index’s market capitalization is made up by the five biggest names, surpassing the 18% mark hit in March 2000. Hammond argues that historically, narrow breadth has signaled a substantial market downturn.

Other Goldman Sachs strategists, however, see this trend in a more positive light. Goldman Sachs’ Ryan Hammond believes that the dispersion of stocks is only going to intensify.

“We expect return dispersion will remain elevated in the near term as investors continue to assess the relative ‘winners’ and ‘losers’ in the current environment. History shows that correlations typically fall and dispersion rises further as the equity market rebounds out of a bear market,” Hammond explained. As a result, investors have been presented with the greatest opportunity to find outperformers in over ten years, in Hammond’s opinion.

With this in mind, we wanted to take a closer look at two stocks Goldman Sachs recently added to its coverage universe. Using TipRanks’ database, we discovered that both Buy-rated tickers boast over 60% upside potential, which could be reason enough to look at the glass half full. Let’s jump right in.

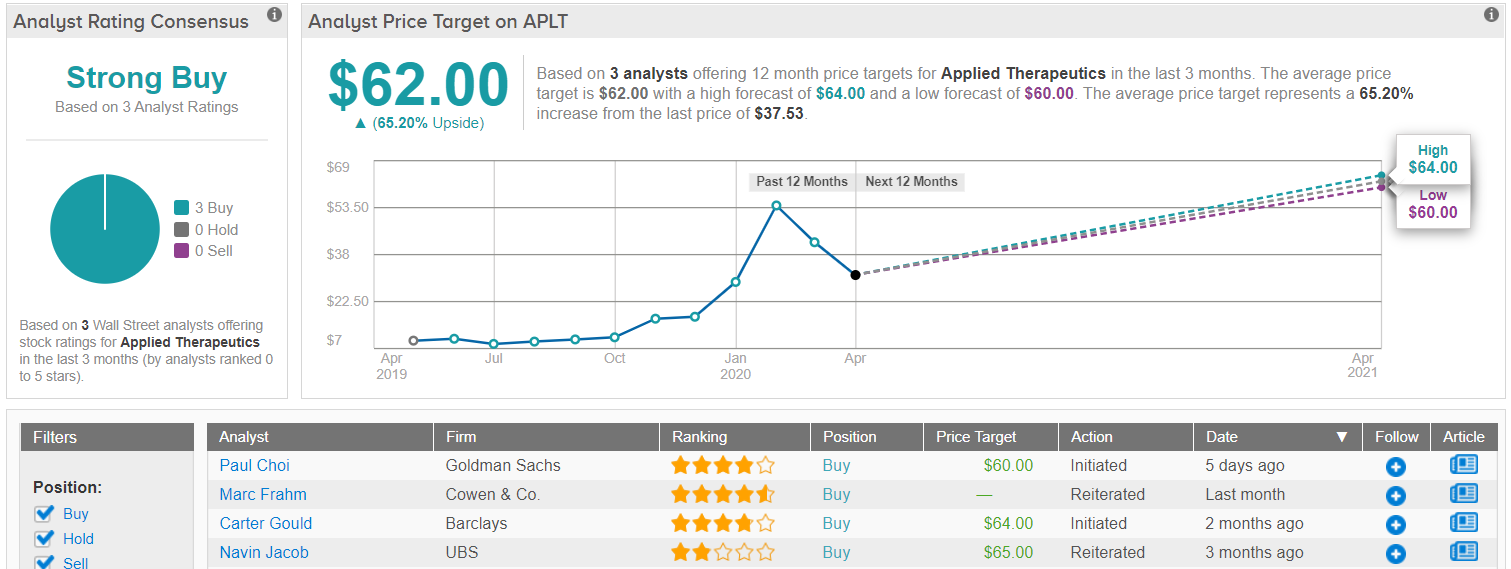

Applied Therapeutics (APLT)

First up we have Applied Therapeutics, which focuses on cutting down the drug development process by developing assets with increased selectivity and potency, and by utilizing previous research that validates the targeted molecules and pathways. With several promising candidates capable of driving some serious growth, Goldman Sachs believes its long-term growth narrative is strong.

Writing for Goldman Sachs, analyst Paul Choi highlights the company’s lead candidate, AT-007, whose NDA should be submitted in the second half of 2020, as being a significant component of his bullish thesis. The candidate was designed for use in galactosemia, a rare inherited disorder with 2,800 patients in the U.S., and could see peak sales hit $315 million in the U.S. and $320 million in the EU. “… we think upcoming clinical and regulatory catalysts will further de-risk the asset in 2020 with a likely launch by 2021,” Choi commented.

Having said that, Choi thinks investor focus will shift to its AT-001 candidate in diabetic cardiomyopathy (DbCM) with the acceleration of the Phase 3 registrational trial, the results of which are expected to be published in 2021, given the large market opportunity and limited competition. As AT-001 achieved robust efficacy results in the Phase 1/2 trial in type 2 diabetic patients (T2DM), Choi believes there’s a high likelihood of approval, with his estimates putting peak sales at $700 million in the U.S. and $440 million in the EU.

Commenting on both assets, Choi stated, “APLT is positioned well to capture share in both therapeutic areas given there are currently no approved therapies for either disease and patients face a high unmet need. Positive data for AT-001 in DbCM could also validate the company’s earlier stage research to address large populations of high unmet need with this asset.”

If that’s not enough, Choi cites the AT-003 Phase 1 initiation for diabetic retinopathy in 2020 and the AT-004 Phase 1 initiation for lymphomas in 2020 as being other potential catalysts.

To this end, Choi initiated his coverage of this biotech with a Buy rating and $60 price target. Should this target be met, a twelve-month gain of 60% could be in store. (To watch Choi’s track record, click here)

Turning now to the rest of the Street, other analysts also take a bullish stance. With 100% Street support, or 4 Buy ratings to be exact, the message is clear: APLT is a Strong Buy. At $63, the average price target is a bit more aggressive than Choi’s and implies 68% upside potential. (See APLT stock analysis on TipRanks)

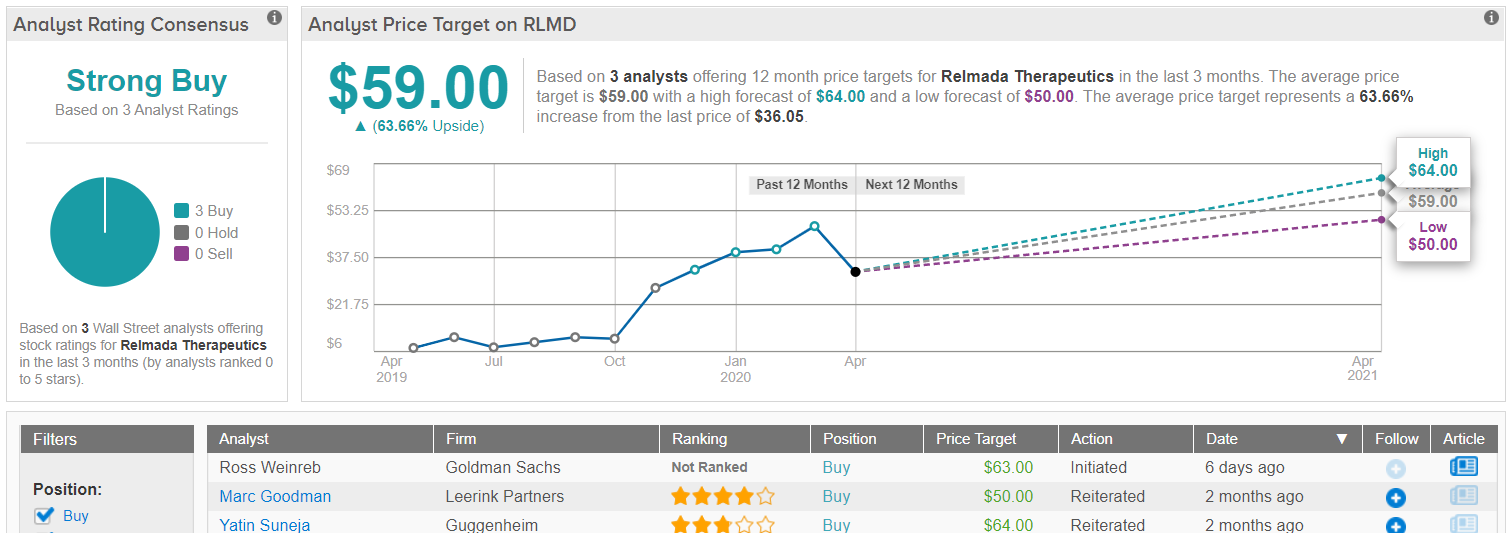

Relmada Therapeutics (RLMD)

Another biotech name, Relmada Therapeutics is primarily focused on developing REL-1017, an oral N-methyl-D-aspartate (NMDA) receptor antagonist, for the treatment of major depressive disorder (MDD). Following a positive Phase 2a data readout, Goldman Sachs is onboard.

Representing the firm, analyst Ross Weinreb points out that the candidate demonstrated strong efficacy results, with it producing a Montgomery-Asberg Depression Rating Scale (MADRS) delta (placebo-subtracted difference) at Day 14 of -9.4/-10.4, which surpasses what’s witnessed in approved atypical anti-psychotics in adjunct MDD. Additionally, REL-1017 was found to be safe and well tolerated, and didn’t exhibit opioid activity or ketamine-like toxicities that have been seen at the therapeutic doses.

As half of depression patients don’t respond to initial anti-depressant therapy, Weinreb sees a large market opportunity, with his estimate for 2032 unadjusted peak sales landing at $2 billion in MDD. “Thus, we see a significant opportunity for a novel therapy with an enhanced clinical profile, such a REL-1017, to enter the market. While we are cognizant of the many players developing therapies in depression, we do not view this as a winner takes all market and note various opportunities exist for multiple therapies across different lines of treatment and settings (i.e monotherapy/acute MDD, TRD),” he explained.

To top it all off, the company’s product pipeline includes several other strong assets and REL-1017 could also be used to treat other conditions later down the line. As a result,

Weinreb kicked off his RLMD coverage by putting a Buy rating and $63 price target on the stock. This conveys his confidence in RLMD’s ability to climb 75% higher in the next year.

Over the past 3 months, only two other analysts have thrown the hat in with a view on the promising drug maker. The two additional Buy ratings provide Relmada with a Strong Buy consensus rating. With an average price target of $59, investors stand to take home a 64% gain, should the target be met over the next 12 months. (See Relmada stock analysis on TipRanks)

To find good ideas for biotech stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.