Have the markets turned the corner? Four of the past five trading sessions have seen net gains. The S&P 500 is up 17% from the March 23 trough. The question now is, are markets truly trending back up, or are traders simply taking advantage of low prices after the recent heavy losses?

That’s the question for the long term. For the moment, traders are taking some comfort in the gains, which have clawed back some one third of the value lost in the bearish run.

With that in mind, Goldman Sachs analysts have been coming the markets for buy-side options, and in a series of reports on tech-related stocks have highlighted three under-the-radar choices. These are interesting picks, tapped by Goldman for their combination of low point of entry and high upside. We’ve used the TipRanks database to flesh out the details – these stocks have at least a 20% upside potential. Let’s see what else makes them such compelling buys.

Tenable Holdings (TENB)

We’ll start with Tenable, a cyber-security company offering tech expertise and SaaS platforms to assess and manage data vulnerability. Tenable’s subsidiaries provide cloud solutions for businesses worldwide, in the education, energy, finance, healthcare, and retail sectors.

Tenable, like many small-cap tech companies, operates at a net loss. The company reported a loss of 24 cents per share in the last quarter, beating the forecast by 4 cents. That beat highlights another feature of the company’s quarterly reports: it has beaten the estimates consistently for the last six quarters. Revenues are growing, at the $97 million reported in Q4 represented 29% year-over-year growth.

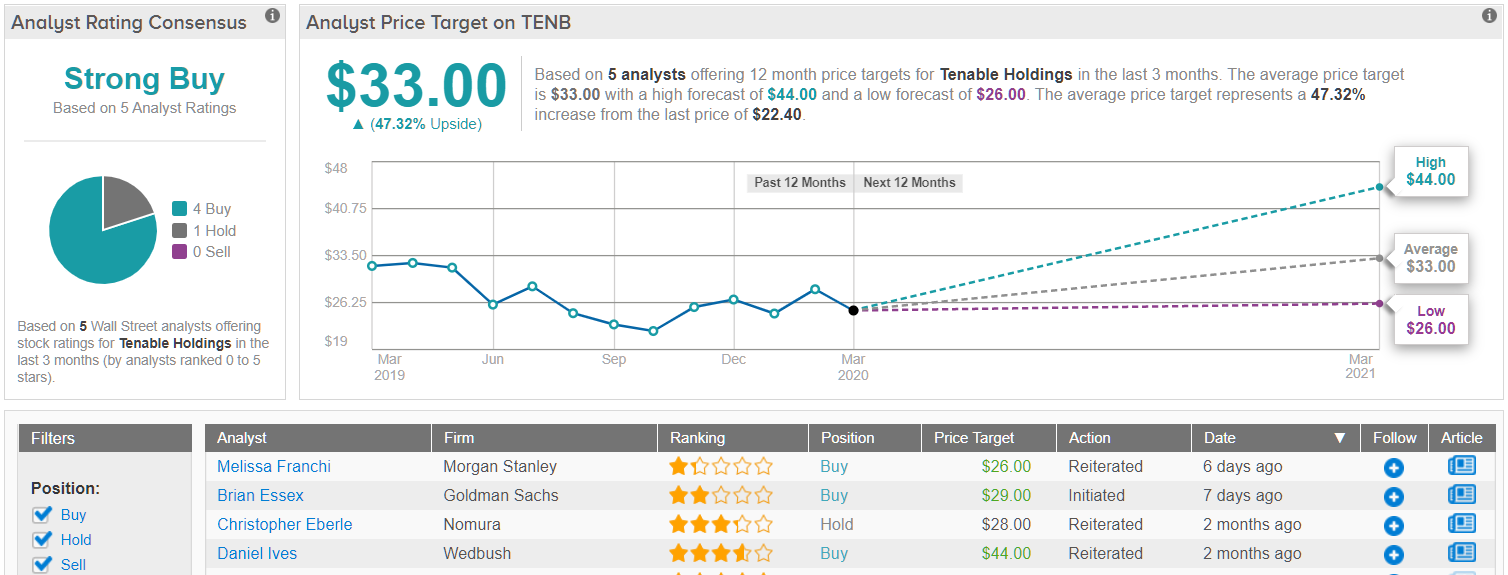

Brian Essex, tech sector expert for Goldman Sachs, reviewed this company and was impressed enough to initiate his coverage with a Buy rating. His $29 price target indicates a 29% upside potential, backing the bullish outlook. (To watch Essex’s track record, click here)

In his comments, Essex says, “We believe Tenable is well-positioned to leverage its best-of-breed reputation in vulnerability assessment to gain further traction among enterprises looking to evaluate their risk exposure and adopt a formal vulnerability assessment program. Tenable has been growing rapidly over the past several years, is among the fastest-growing companies in our coverage universe, and remains a critical provider for continuous monitoring, which is an important compliance-related focal point. While the company has yet to turn profitable, it has made meaningful progress, and we expect this to continue as we believe that the company has demonstrated discipline with regard to meeting profitability targets […] With continued execution and demonstrated progress on profitability, we see meaningful upside opportunity for the stock.”

Looking at the consensus breakdown, Wall Street takes a bullish stance on Tenable. 4 Buys and 1 Hold issued over the previous three months make the stock a Strong Buy. It should also be noted that its $33 average price target suggests 47% upside from the current share price. (See Tenable stock analysis on TipRanks)

Rapid7, Inc. (RPD)

The second stock on our list is another cybersecurity company. Rapid7 uses data and analytic solutions to provide customers with the ability to detect and control their exposure to digital threats, using real-time analysis. It’s a vital niche that provides a clear path for RPD’s success.

In Q4, RPD beat the earnings forecast with a 3-cent EPS, a far cry from the year-ago loss of 5 cents. Revenue came in at $91.7 million, not only beating the estimates but also growing 33% year-over-year. The Q4 results were also higher sequentially; EPS grew 2 cents, and revenue was up 10%, from the third quarter. After posting strong share gains in 2019, for 2020 RPD stock is down 21% year-to-date, roughly in-line with the S&P and Dow results. The stock bottomed out on March 16 at $33.40 and has climbed 32% since then.

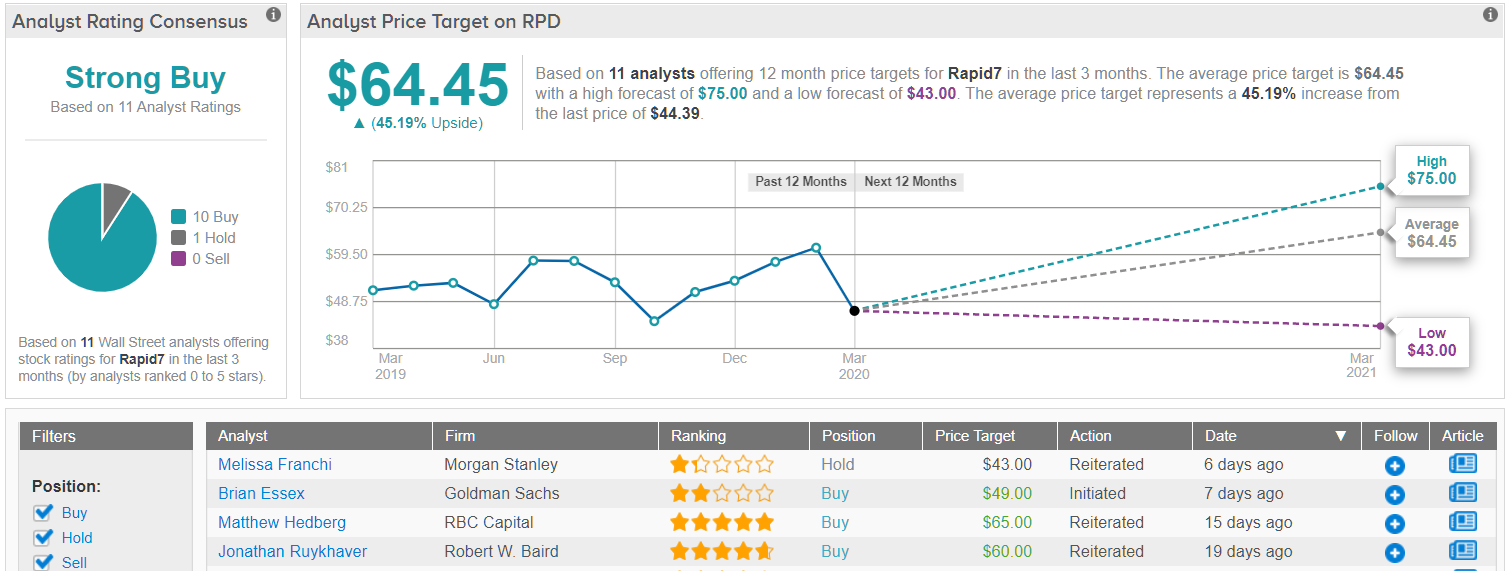

This is another company that impressed analyst Brian Essex enough to initiate a Buy rating. Essex gives RPD a $49 price target, implying an upside potential of 11%. (To watch Essex’s track record, click here)

Essex writes of the stock, “Rapid7 has positioned itself as one of the dominant vendors in the Vulnerability Assessment and Management (VA/VM) market with its InsightVM offering, that provides a comprehensive view of an organization’s asset vulnerability posture and tools for prioritization and remediation of the same […] As organizations turn to analytics and AI/ML based solutions to reduce dependence on manual labor and look to implement platforms for risk assessment and threat remediation, we believe Rapid7 is competitively positioned. With the stock trading at a discount to our coverage group median on an EV/sales/growth (CY21) basis (0.19x EV/sales/growth for RPD vs. 0.28x for coverage group median) and continued margin expansion coupled with strong revenue growth, we see favorable risk/reward.”

Overall, Rapid7 has 11 recent analyst reviews, breaking down as 10 Buys and 1 Hold and giving the stock a Strong Buy consensus rating. Shares are currently trading at $44.39, and have a 45% upside potential based on an average price target of $64.45. (See Rapid7’s stock analysis on TipRanks)

Huya, Inc. (HUYA)

With the last stock on our list, we take a turn to the gaming sector. Huya is a live streaming game platform, with interactive video services supporting e-sports, music, reality programming, talent shows, anime, and outdoor activities. The Huya platform is available in China – the Chinese government policy of restricting international internet access makes it easy for Western audiences to sometimes forget that China’s domestic web audience numbers of 800 million strong.

China’s huge domestic audience gives its home-grown internet companies a market comparable to anything in the West. Huya’s fiscal results reflect that. The company consistently operates at a profit, and has beaten forecasts in the last three quarters. Q4 revenues grew 64% yoy to reach 2.468 billion CNY ($348 million US, at current exchange rates), and EPS came in at 10 cents US, up 3 cents sequentially.

As an online gaming company, Huya is a natural choice to show gains during the lockdowns and quarantines implemented to fight the coronavirus spread. The first quarter is the company’s seasonal weakest, and declines during the Chinese Lunar New Year holiday are usually expected – but this year, the nationwide lockdowns have boosted demand for online entertainment.

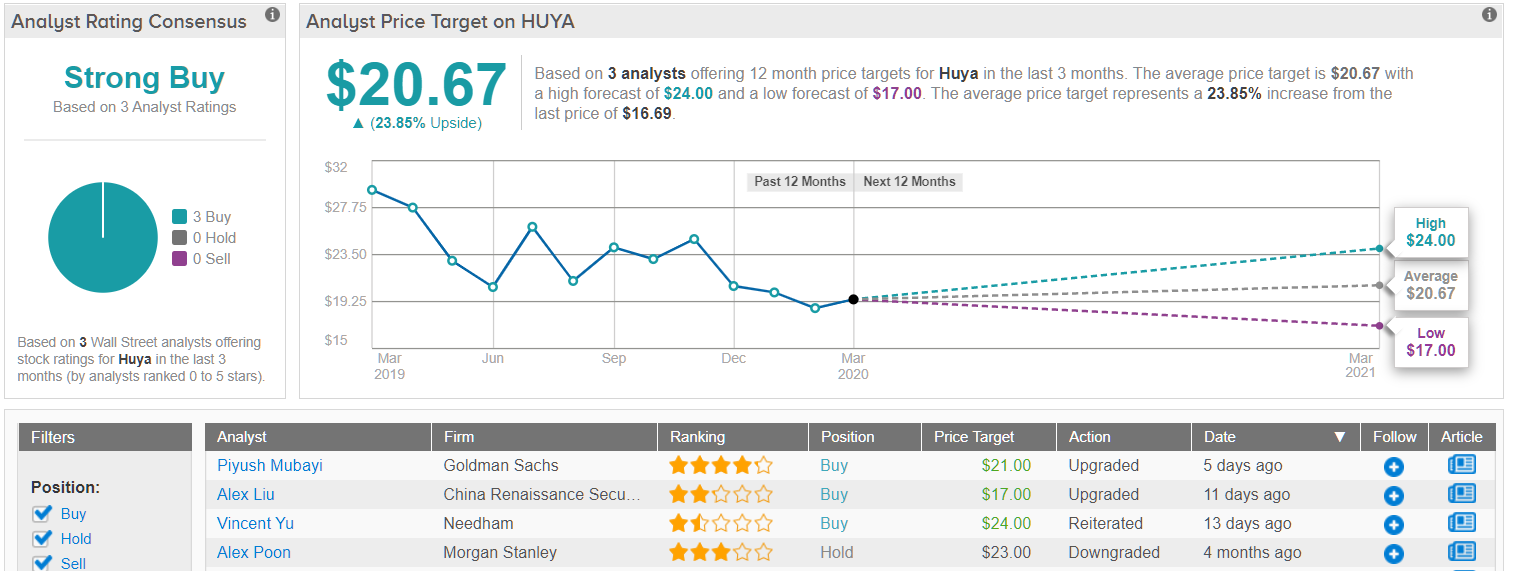

Writing on HUYA for Goldman Sachs, 4-star analyst Piyush Mubayi notes of the platform, “…surged traffic has been converted to better monetization, as Huya’s paying users have also reached a record high of 5.5mn according to management […] Huya’s live streaming revenue increased by 64% yoy to Rmb2.5bn, driven by robust MAU growth momentum…”

Mubayi’s $21 price target suggests a 24% upside potential for the stock. In line with his upbeat outlook, he has upgraded his stance on HUYA shares from Neutral to Buy. (To watch Mubayi’s track record, click here)

“We upgrade Huya to Buy from Neutral as we see attractive risk/reward for a fast growing company with a 21% EPADS CAGR in 2021E-2023E,” Mubayi concluded.

All in all, HUYA shares have three recent reviews and they are all on the Buy-side, making the Strong Buy analyst consensus view unanimous. The stock is bargain priced, at just $16.90, and the $20.67 average price target implies a solid upside of 24%. (See Huya’s stock analysis at TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.