The stock analysts at Goldman Sachs have been busy. The bank – one of the world’s largest and most influential investment and financial services organizations, with alumni in government positions throughout the major Western nations – maintains a cadre of Wall Street experts, who keep close tabs on the constant shiftings of the stock markets. The result is a wealth of expert opinion, backed by data, on the current go-to investments.

All of this is bread and butter for TipRanks, a platform that makes financial recommendations accountable, and expensive institutional datasets available, to all investors. We’ve pulled up three of Goldman’s recent tech sector stock picks, and run them through TipRanks’ Stock Screener tool to confirm that Goldman is in the majority on Wall Street in recommending these equities.

So, here are the results. Three tech stocks that usually fly under the radar – but Goldman sees them all with more than 15% upside potential in the coming year.

GSX Techedu, Inc. (GSX)

First on our list is an education-related tech stock from China. GSX is a software company, providing educational packages for after-school tutoring. The company is a leader in the K-12, large-class, after-school market in China, an important segment in a culture that puts a premium on education.

A combination of factors worked to push GSX shares sharply upward in December – as much as 24%. While’s China’s overall economic growth has been slowing in recent years, and the trade tensions with the US have put pressures on most sectors of the Chinese economy, Chinese parents still put a premium on giving their kids the best possible education. That cultural imperative helped insulate GSX, and the company showed a tremendous 460% year-over-year revenue gain in Q3, posting 557 million yuan in sales – approximately $80 million in US currency. Total student enrollment rose by 240%, to 820,000.

When news broke of the Phase 1 trade agreement between the US and Chinese governments last month, however, Chinese markets experienced a broad rally – and that included GSX. Investors were suddenly bullish after the trade agreement was announced and the signing was scheduled, and more willing to invest – and a company with GSX’s proven recent growth was sure to attract plenty of investor attention.

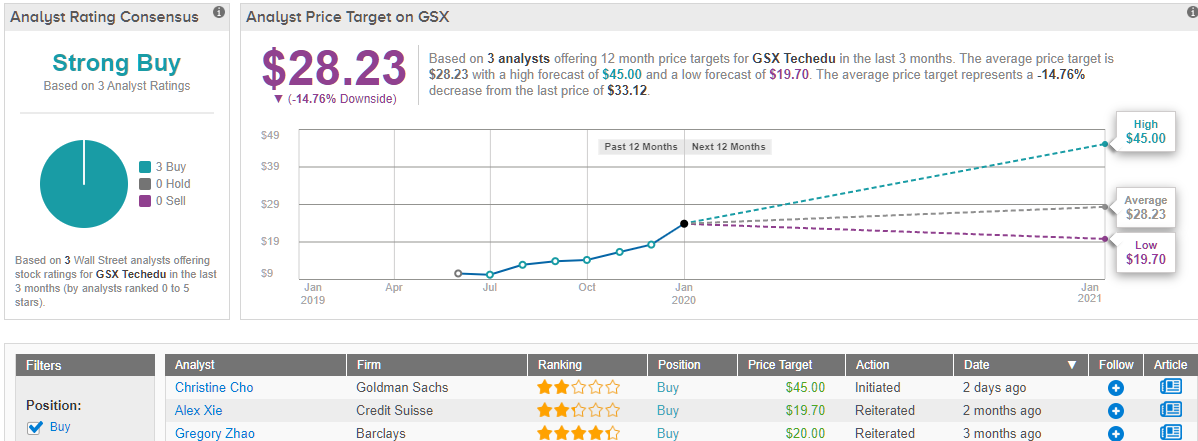

Goldman’s Christine Cho reviewed GSX, and outlined the major advantages of the stock for investors. First, regarding the educational market generally in China, she wrote, “We expect online AST penetration will grow from 15% of the total AST market to 41% over the same period, as we believe online AST courses have a wider reach given their scalability, lack of physical constraints and better affordability…” And, looking at GSX specifically, Cho laid out her firm’s line: “We believe its competitive moat lies in its technology DNA and ROI mindset, scalable business model via well-managed star teachers, and best-in-class operating efficiency…”

Cho initiated coverage of this stock for Goldman, giving it a Buy rating and setting an aggressive price target of $45. Her target indicates confidence in an upside potential of 28% for the next 12 months. (To watch Cho’s track record, click here)

Overall, investors and analysts are bullish on this stock. The price run-up in December pushed the share price to $35.25, well above the consensus price target. However, Cho’s new coverage, with her higher target, indicate the potential available in GSX shares. (See GSX stock analysis at TipRanks)

Avaya Holdings Corporation (AVYA)

The next two stock on our list are related, operating in the same sector and, more importantly, having just entered a strategic partnership. First up is Avaya Holdings, a holding company whose main subsidiary, Avaya, Inc., provides software in the business communication and collaboration niche. Avaya’s products offer services to unify communications, contact centers, and real-time video systems.

Business communications is an essential niche; no company can do without an efficient system for managing its analog, digital, and online communications. Avaya has ridden that need, and put up strong revenue numbers from filling it. In Q4 of fiscal 2019, reported in November, the company showed $723 million in quarterly revenues, and $2.89 billion in annual revenues. These numbers reflect GAAP figures, and the annual total shows a 1.4% year-over-year gain. The company’s cash on hand has shown steady increases in the past year, and stands at $752 million.

During the quarter, Avaya announced a partnership with RingCentral (more below), through which Ring will become Avaya’s sole provider of UCaaS solutions. In addition, Ring committed to paying $500 million to Avaya in return for stock shares and licensing rights. The move brings Avaya’s services and migration capabilities into combination with Ring’s UCaaS platform, for both companies’ benefit.

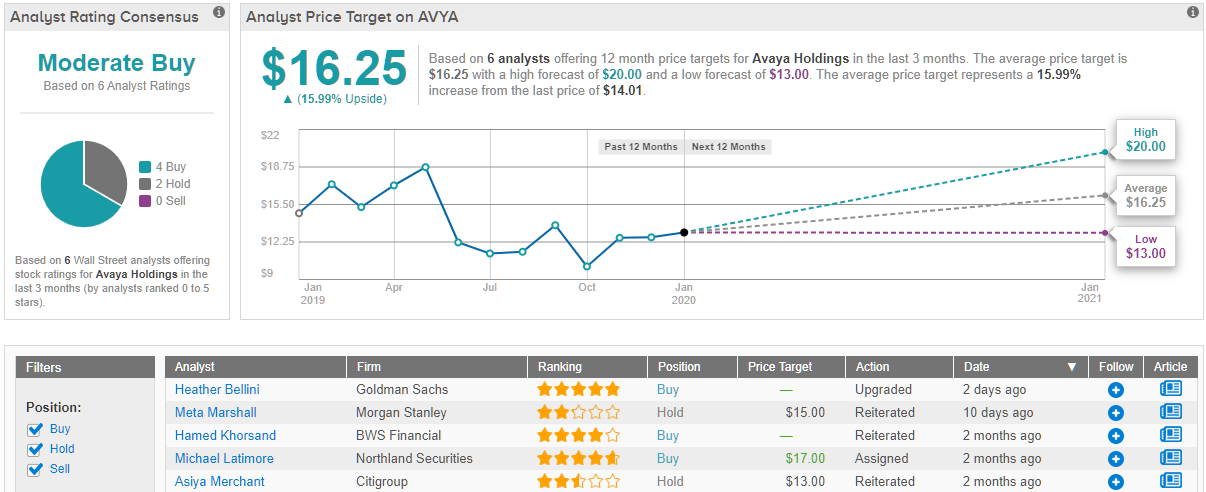

Goldman Sachs sees plenty of reason for optimism in Avaya’s current situation. Writing for the firm, 4-star analyst Rod Hall says, “We believe the economics of the announced RingCentral deal are likely to drive Avaya’s revenue and profitability above consensus expectations… In our central case, we estimate that ACO conversions could add ~$28m in revenue to Avaya in the first full year of its availability…”

Hall puts a Buy rating on AVYA shares and his price target of $18 suggests an upside of 28% for stock. (To watch Hall’s track record, click here)

Shares in AVYA are priced at $14, and the average target of $16.25 suggests room for 16% growth in the coming year. The Moderate Buy analyst consensus rating is based on 6 reviews, including 4 Buys and 2 Holds. (See Avaya stock analysis at TipRanks)

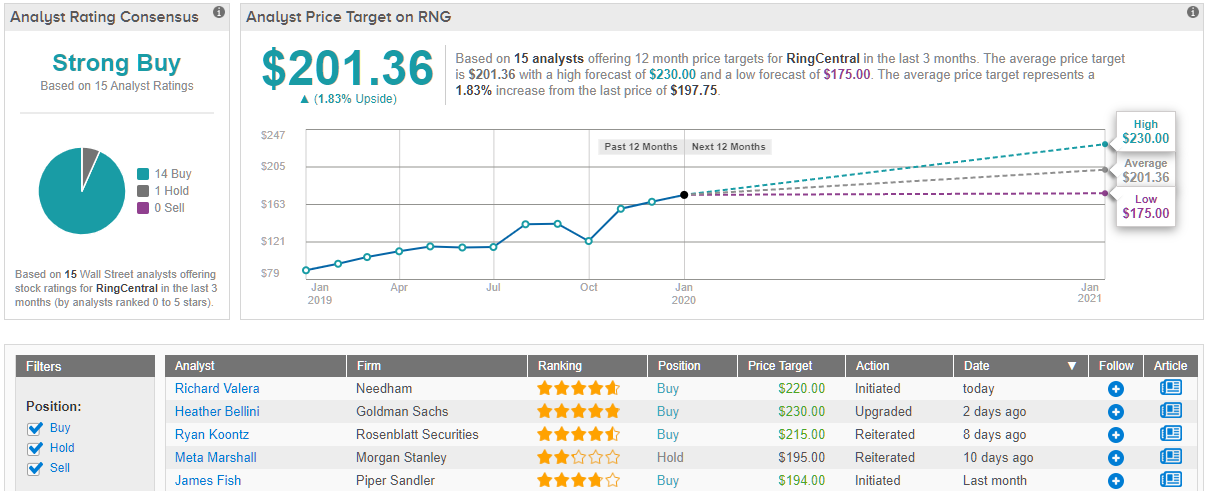

RingCentral, Inc. (RNG)

Third on our list is Avaya’s new partner, RingCentral. RNG brings cloud computing to the realm of business communications, with software packages combining two staples of the modern office: telephone and computer systems. RingCentral Office, the company’s flagship product, is sync-compatible with popular business applications like Salesforce, Outlook, Google Docs, and DropBox, plus it provides RNG’s unique features in call forwarding, multiple telephone extensions, video conferencing, and screen sharing.

RingCentral’s strong product, solving real problems and improving business efficiencies, has brought the company equally strong profits. Revenues and earnings were both up in Q3 2019, the most recent reported. EPS, at 22 cents, was up 15% year-over-year, and beat the forecast by 15%. Revenues came in at $222 million, showing an impressive 34% year-over-year growth. Strong profits and earnings, in turn, powered RNG’s share appreciation – the stock gained 108% in 2019.

Heather Bellini, 5-star analyst with Goldman, was impressed enough by RNG’s performance to upgrade the stock from Neutral to Buy, while setting a $230 price target. Her target suggests a about 15% upside to the stock.

In her comments, Bellini noted RNG’s fast-paced growth, and recent AVYA partnership’s potential to drive further growth. She writes, “We see continued runway for outperformance driven by secular growth from UCaaS adoption, enterprise traction, and continued evolution in the companies go-to-market strategy, most notably RingCentral’s recently announced partnership with Avaya.” (To watch Bellini’s track record, click here)

RNG holds a Strong Buy rating from the analyst consensus, with 14 Buy ratings and just a single Hold. Shares are priced high, at $197.75, reflecting the stock’s recent gains. The average price target is $201.36, implying a 2% upside for the stock – but as cited above, Goldman analyst sees a 15% upside ahead for RingCentral. (See RingCentral stock analysis at TipRanks)