Another retailer bit the dust last Friday when J.C. Penney filed for bankruptcy after 118 years in business. They join J.Crew, J.Hilburn, Stage Stores and Neiman Marcus which have all filed in the previous few weeks. Now analysts are wondering who will be next, with Macy’s, Nordstrom and Gap high on the list of mentions. All this comes as the worst monthly retail sales figure in history is recorded (April tanked 16.4%), and as Q1 retail earnings get ready to report.

Retail earnings season kicked off with a handful of names last week including Under Armour, Dillard’s and Farfetch, with only the latter surprising to the upside. Under Armour and Dillard’s each posted triple digit declines in YoY profits for the first quarter, an ominous foreshadowing for the slew of apparel companies and department stores reporting this week.

Worst Earnings Growth Estimates on Record

The downfall of many of these retailers can’t all be blamed on COVID-19, of course. Department stores have been bad off for a decade as mall traffic has continually slowed and the propensity towards ecommerce has increased. Tomorrow we get results from those still hanging in there: Macy’s and Nordstrom, as well as Kohl’s which reported this morning.

Kohl’s reported a triple digit decline in Q1 profit growth year-over-year (YoY), and Macy’s and Nordstrom are expected to follow suit tomorrow. This is historically significant. For Macy’s, earnings per share (EPS) is expected to drop over 300% (data from Zacks) from last year, which would be the worst showing since Q1 2009 when YoY EPS fell 900%. For Nordstrom and Kohl’s it gets even worse than that, even lows from the great recession will not rival what Kohl’s has already reported, and what Nordstrom is anticipated to post for Q1 2020, this will be the worst quarter for growth since either started trading on the NYSE. For Kohl’s this was in 1992 when it IPO’d and for Nordstrom in 1999 when they joined NYSE from NASDAQ under the ticker JWN (I don’t have access to data from when they traded on the NASDAQ so this trend could be much more pronounced).

Off-price Expected to Make a Comeback

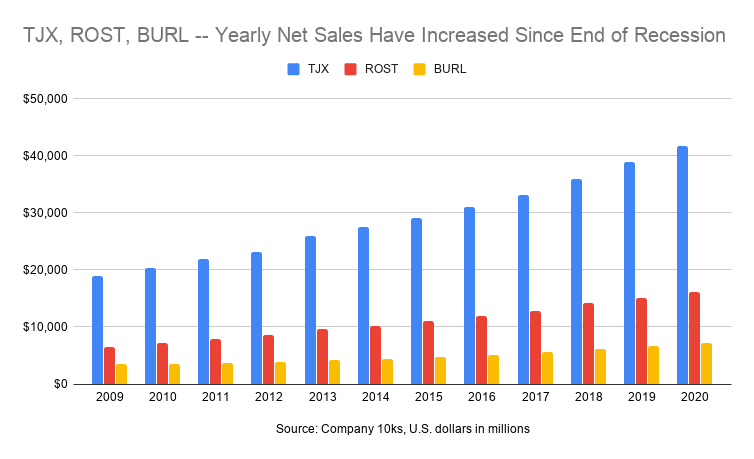

In addition to department stores we get results from the discounters this week: TJMaxx, Burlington Coat Factory and Ross Stores have been stealing market share from department stores for the better part of a decade. Since the great recession these three names have seen steady increases in net sales (see below). Now they’re in a tough position as they don’t have an ecommerce presence, but once things open back up could they be poised for a strong comeback? Some of the top sell side analysts think so.

One thing discounters have going for them versus department stores and other apparel names is their strong fundamentals. While profits and revenues continue to sink for the department stores, discounters are posting some of their best numbers. Brands have begun to view the discounters as more reliable and consistent when it comes to inventory purchases. Although the off-price retailers tend to order less product at a time, department stores are canceling orders in an attempt to stay solvent.

Add to that the fact that 36M Americans have filed for unemployment, and you’re starting to see a setup similar to 2008 – 2009 which favored discounters. American consumers will be looking for value more than ever, with bargain hunting trends expected to make a huge comeback.

The three biggest names in the space, BURL, ROST and TJX continue to hold onto “strong buy” recommendations from the best analysts on TipRanks, but all have seen their 12-mo price targets drop since coronavirus-related lockdowns went into effect. Michael Baker, the four star analyst from Nomura Instinet, believes there is enough evidence to suggest that “April was the peak month for virus-related sales pressure and the low point of the recovery for retailers.” A key catalyst that many retail analysts will be looking for this earnings season is confirmation that April was the bottom for retailers.

T.J.Maxx

T.J.Maxx reports on Tuesday. Currently the sell side is looking for EPS of $-0.02, a YoY decline of 104%. Revenues are set to drop 38% YoY. All 8 of the best analysts covering this stock (that have issued ratings in the last 3 months) have a “buy” rating. Nomura Instinet and Credit Suisse have even raised price targets. The consensus PT stands at $63.13, that’s 25% upside from current prices.

Ross Stores

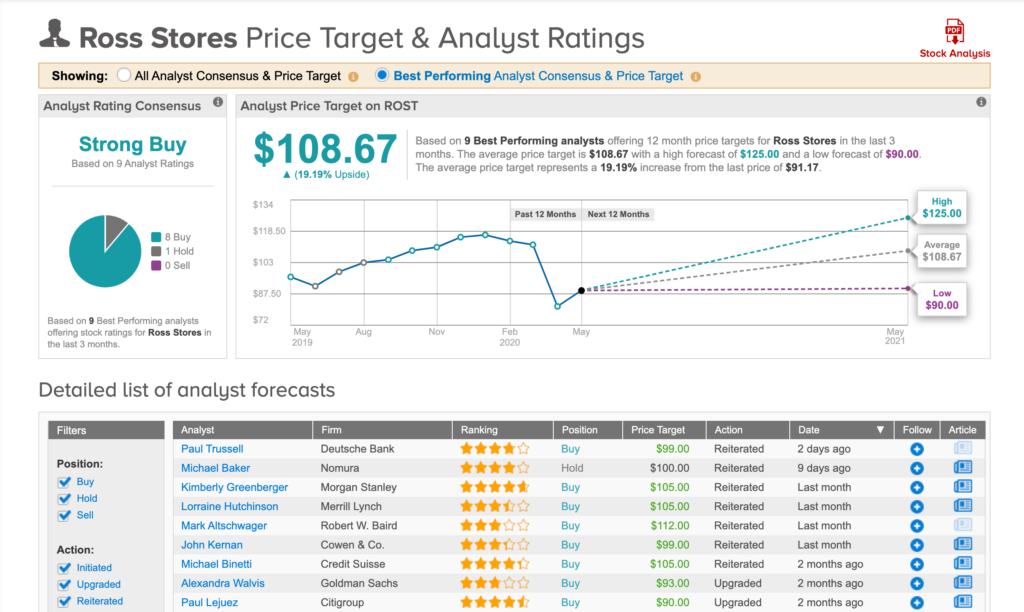

Of the 9 top analysts that cover ROST, all have reiterated buy ratings in the last 3 months, with the exception of one hold by Michael Baker at Nomura, although he did increase his price target to $100 from $80. Bank of America Merrill Lynch analyst, Lorraine Hutchinson, believes ROST will have a strong post-COVID recovery driven by better inventory purchases. “ROST has strengthened its balance sheet to maximize flexibility to excel when conditions return to normal. ROST issued four bonds, ranging in maturities from five to thirty years, to raise an additional $2B in capital. ROST ended 4Q with a cash balance of $1.35B and we estimate that it has sufficient liquidity to sustain no sales for 65 weeks.”

Burlington Stores

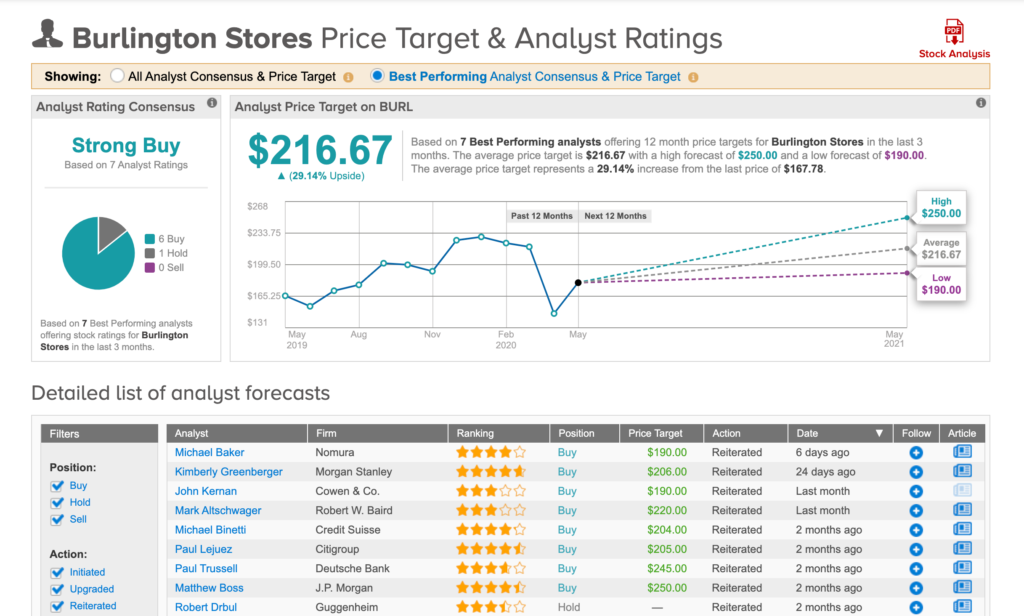

In the last three months, all of our top analysts have reiterated BURL as a buy, with the exception of Robert Drbul of Guggenheim who has a hold. Price targets have been lowered across the board, except from analyst Michael Baker at Nomura Instinet who raised his PT to $190 from $170. The consensus price target is $216.67, an upside of 29% from current prices. BURL is anticipated to report EPS of $-1.14 (190% decline YoY) and revs of $1.03B (38% decline YoY) when they report next week.

It all goes down tomorrow when TJX reports Q1 results before the bell and ROST reports after the bell. BURL results come out next Thursday, May 28.