Saying ‘insider trading’ conjures up images of smoky back rooms and shady deals, but that’s only for the movies. In real life, insiders refer to corporate officers, such as CEOs, CFOs, COOs, and directors, who are responsible for running their companies profitably. They don’t take trading their own companies’ stocks lightly. While they may sell for various reasons, they only buy when they anticipate a rise in the share price.

That makes the insiders’ trading moves one of the surest signs that investors can look for to predict a stock’s near- to mid-term movements. The insiders, by virtue of their positions, have advance information on the factors that will impact the shares, and regulatory authorities level the playing field by requiring insiders to publish their trades. Investors can watch for these publications, and stocks with strong insider buying are always worth a closer look.

You can give the positive insider signals a boost by combining them with other factors closely linked to strong returns – like high dividend yields. Passive income is always a boon for investors, and when that passive income is yielding 8% or better, and the insiders are buying big, it’s a combination that demands attention.

So let’s give these double-barreled stocks some of the attention they deserve. Using the Insiders Hot Stocks tool on TipRanks, we’ve found two stocks that are showing strong insider buying in recent days, along with dividend yields starting at 8% and going up from there. If that’s not enough, both stocks have also received support from Wall Street analysts. Let’s take a closer look.

Owl Rock Capital (ORCC)

We’ll start in the world of Business Development Companies, or BDCs. These financial firms offer their customers access to credit and capital. Their customer base consists of small- and medium-sized enterprises that have long been the drivers of the US economy. These firms don’t always have access to major banks, but Owl Rock and its peers provide the capital, credit, and loan facilities that these businesses need for growth, acquisitions, and market or product expansions.

There are 187 of these mid-market firms in Owl Rock Capital’s investment portfolio, with a total fair market value in excess of $13 billion. Of Owl Rock’s investments in these firms, 98% are floating rate, and 85% are senior secured investments.

It’s a quality portfolio that has contributed to ORCC’s rising earnings over the past year. In fact, the company’s latest quarter, 1Q23, showcased strong income that exceeded the Street’s forecasts by a wide margin. ORCC’s total investment income reached $377.6 million, representing a 42% increase compared to the year-ago quarter. Even better, the total investment income came in $12 million more than had been expected.

At the bottom line, the net investment income (NII) came in at $177.8 million, or 45 cents per share. This was 14 cents per share higher than the 1Q22 figure – and it was 2 cents more than the analysts had predicted.

The strong investment income supported a generous dividend. For the second quarter, the company has declared a regular dividend of 33 cents per common share, which is scheduled for payment on July 14. This regular dividend, when annualized, amounts to $1.32 and provides an impressive yield of 9.8%.

On the insider trades, we find that company President and CEO Craig Packer, bought 75,600 shares of the company in May, paying about $1 million.

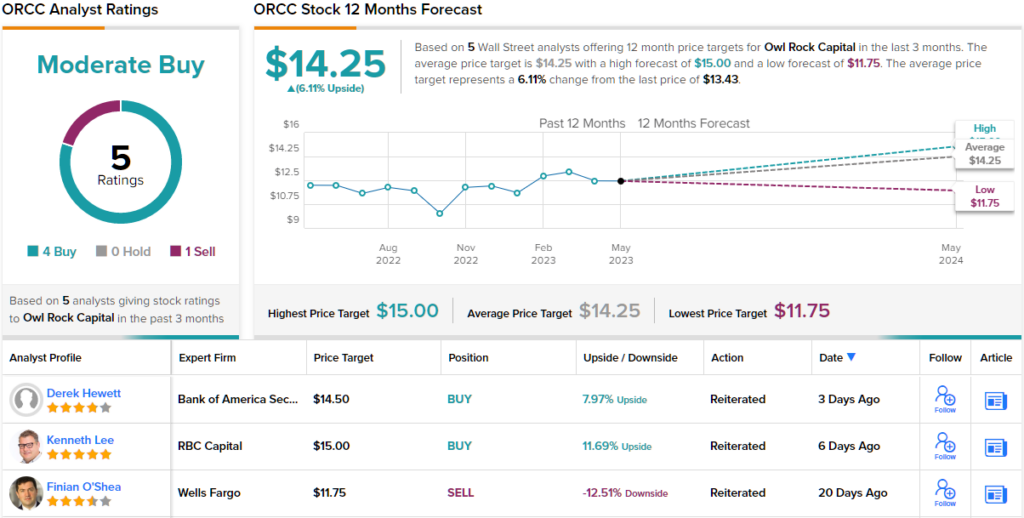

The company’s top officer is hardly the only bull here; RBC Capital’s 5-star analyst Kenneth Lee writes of this stock: “ORCC could be on track to delivering 12%+ ROE this year. Credit performance in portfolio is still solid, in our view. We expect to gain further insight into ORCC’s investment approach and potential return profile through cycles at the upcoming investor day. We continue to favor ORCC as one of the few atscale BDCs, with an attractive valuation (0.85x NAV) and dividend yield (~10%).”

In Lee’s view, this adds up to an Outperform (i.e. Buy) rating, and he sets a price target of $15 to imply a one-year upside potential of ~12%. Based on the current dividend yield and the expected price appreciation, the stock has 22% potential total return profile. (To watch Lee’s track record, click here)

As far as Wall Street generally is concerned, ORCC gets a Moderate Buy consensus rating, based on 5 recent reviews that include 4 Buys and 1 Sell. (See ORCC stock forecast)

Boston Properties (BXP)

From BDCs we’ll shift gears and look at a company from another sector which is known for high dividends, a real estate investment trust. The REIT at hand is Boston Properties, a major player in the US workplace real estate segment. Boston Properties is the largest publicly traded developer, owner, and manager of such properties in the US.

A look at some numbers will give the scale. Boston Properties counts 177 office properties in its portfolio, totaling 50 million square feet of leasable space. These properties are located in six urban regions, well known as some of the most desirable real estate in the US. BXP has holdings in its eponymous city of Boston, along with New York City, Washington DC, Seattle, San Francisco, and Los Angeles. The company’s largest presence, with 49 locations and 15.9 million square feet, is in Boston; Washington and New York are next, with 42 properties and 22.6 million square feet between them.

Commercial real estate, especially in urban areas, is feeling pressure post-COVID. With many workers still commuting remotely, companies are trying to downsize their office spaces. But even in that difficult environment, BXP has kept up its revenues and earnings. The company’s top line in the most recent quarter, 1Q23, came to $803.2 million, capping nearly two years of consistent quarter-over-quarter revenue growth. The Q1 total was also up 6.5% year-over-year, and beat expectations by $24.4 million.

At the bottom line, there are several metrics to consider. BXP’s GAAP earnings of 50 cents missed the forecast by 4 cents and were 45% lower than the year-ago quarter’s EPS of 91 cents. Of more interest to dividend investors, however, BXP reported funds from operations (FFO) in 1Q23 of $1.73 per share, derived from a total of $272 million. While down from the year-ago quarter’s results ($1.82 per share and a total of $286.1 million), the current FFO was more than enough to fully fund the company’s dividend.

The dividend was paid out near the end of April, for 98 cents per common share. BXP has held the dividend at this level since late 2019; the annualized rate of $3.92 per common share gives a strong yield of 8%.

Taking a closer look at this firm’s insider trades, we discover that Carol Einiger, a member of the Board of Directors, recently acquired 10,000 shares, paying $474,100.

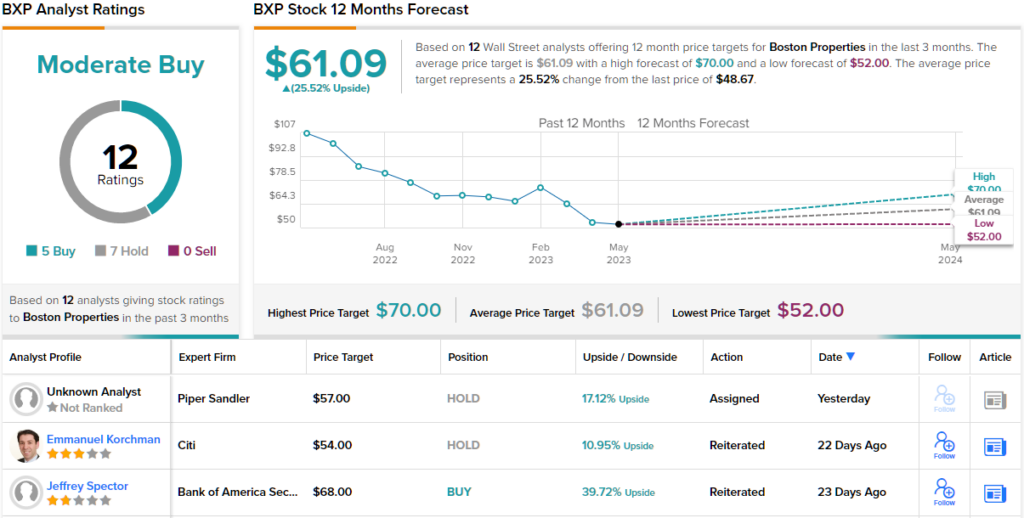

Also bullish on the stock is Evercore ISI analyst Steve Sakwa, who focuses on the company’s ability to generate funds.

“After a couple of tweaks to our model, our ‘23 FFO est increases from $7.15 to $7.18 driven by slightly higher base rent and lower op expenses which compares to our new FY24 estimate of $7.58 which reflects slightly more conservative operating expenses… We maintain our Outperform rating given the company’s quality portfolio, healthy balance sheet and robust development pipeline to drive long-term value in an otherwise challenged office sector,” Sakwa opined.

That Outperform (i.e. Buy) rating comes with a $67 price target that implies growth of ~38% for the year ahead. (To watch Sakwa’s track record, click here.)

Overall, of the 12 most recent analyst reviews on record here, 5 are to Buy and 7 to Hold – giving the stock its Moderate Buy consensus rating. (See BXP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.