If you’ve read the news, you’ve most likely heard of ChatGPT. The newly released chatbot, based on artificial intelligence, machine learnings, and interactive human training, has made waves for its ability to engage in conversation, and for its mistakes along the way. The jury is still out on whether or not it’s a resounding success, but one thing is clear: it has kickstarted a conversation about the role of artificial intelligence (AI) in the world.

AI stocks have been in the public market for several years now, as the tech has made inroads into all sorts of niches – interactive chat bots, of course, but also autonomous vehicles, robotics, warehousing… even online content writing. There’s no doubt that AI is here to stay, nor any doubt that, long term, it’s going to bring some radical changes with it.

But for now, are AI stocks really worth all the hype that everyone is talking about?

Looking into the TipRanks data, and the commentaries from the Street’s analysts, it would seem for now that the answer is ‘No.’ The stocks don’t rate highly with Wall Street’s stock pros, who note that the tech is young, the success of its applications remains shaky, and the investments are still highly speculative.

With this in mind, let’s look under the hood of a couple of high profile AI stocks, check out their analyst ratings and their latest data readouts, and see if we can’t get a feel for where AI is headed.

C3.ai, Inc. (AI)

We’ll start with C3ai, an enterprise AI company integrating artificial intelligence into software applications. The company offers a family of products, including its C3 AI Application Platform, an end-to-end development and deployment platform, along with a portfolio of SaaS AI apps for digital transformation. C3ai’s apps and software have found use in customer engagement, fraud detection, predictive maintenance, and supply chain optimization.

Since going public just over two years ago, C3ai saw its share price drop sharply – not uncommon for firms working with highly speculative technology. In recent days, however, the stock has seen a sharp spike, and has nearly doubled in price since January 5. These strong gains came after the company released a new product suite, C3 Generate AI, a product based on natural language used to locate, retrieve, and present data from across a full range of information systems. In addition, C3 announced at the end of January that will be integrating ChatGPT into its product line.

In its most recent financial release, for Q2 of fiscal year 2023, made public in December, C3ai showed a modest year-over-year revenue gain of 7%, with the top line expanding from $58.3 million to $62.4 million. The company’s subscription revenue led the way, growing by 26% y/y to $59.5 million. C3ai operates at a loss, but the non-GAAP net EPS loss of 11 cents was less than half of the 23-cent EPS loss recorded in the prior year quarter.

Watching C3ai for Deutsche Bank, 5-star analyst Brad Zelnick acknowledges the hopes of the AI sector, while coming down hard against immediate investment: “We remain concerned by a transition story with few tangible guideposts to measure progress along the way… There is no doubt C3 offers valuable predictive analytics applications to its customers, but the market for its model driven architecture is difficult to ascertain amidst the tenuous macro backdrop and business model transition. We await more evidence that the changes happening at C3 will serve to accelerate adoption/monetization…”

To this end, Zelnick puts a Sell rating on AI shares, with an $11 price target that implies a one-year downside of ~47%. (To watch Zelnick’s track record, click here)

This is hardly the only gloomy assessment of C3ai’s prospects. Of the 6 recent analyst reviews on file, 3 are to Sell and 2 to Hold, against just 1 to Buy, and the stock’s average price target of $13.80 suggests that we’ll see a 33% downside in the next 12 months. (See C3ai stock forecast)

BuzzFeed, Inc. (BZFD)

The next stock we’ll look at, BuzzFeed, was founded back in 2006 to track viral content – and today has become somewhat ubiquitous online. In addition to tracking viral content, the company also generates and promotes content, including online quizzes, pop culture article, and new-style content of ‘fluff’ topics. BuzzFeed is closely aligned with the Huffington Post – Kenneth Lerer, chairman of BuzzFeed, was a co-founder of HuffPo – and has made forays into serious journalism.

Shares in BuzzFeed fell sharply all last year, and into this past January – but showed a massive jump just last week, on the announcement that BuzzFeed will work with OpenAI, the creator of ChatGPT, to develop AI-inspired content in the near-term. In short, BuzzFeed will attempt to integrate AI into its content creation; the chatbot will become the chat creator. The idea is both risky and innovative, and the news sent BZFD shares skyrocketing.

The possible integrate of AI into BuzzFeed’s content creation does bring a promise of reduced costs and stronger margins, which can support the company’s moderate revenue growth. In its last reported quarter – 3Q22 – BuzzFeed showed a top line of $104 million, up 15% y/y. The increase was driven by content revenue, which at $38.4 million, was up 45% y/y. Ad revenue came in at $50.4 million, flat year-over-year. The company’s net loss deepened significantly, from $3.6 million in 3Q21 to $27 million in 3Q22.

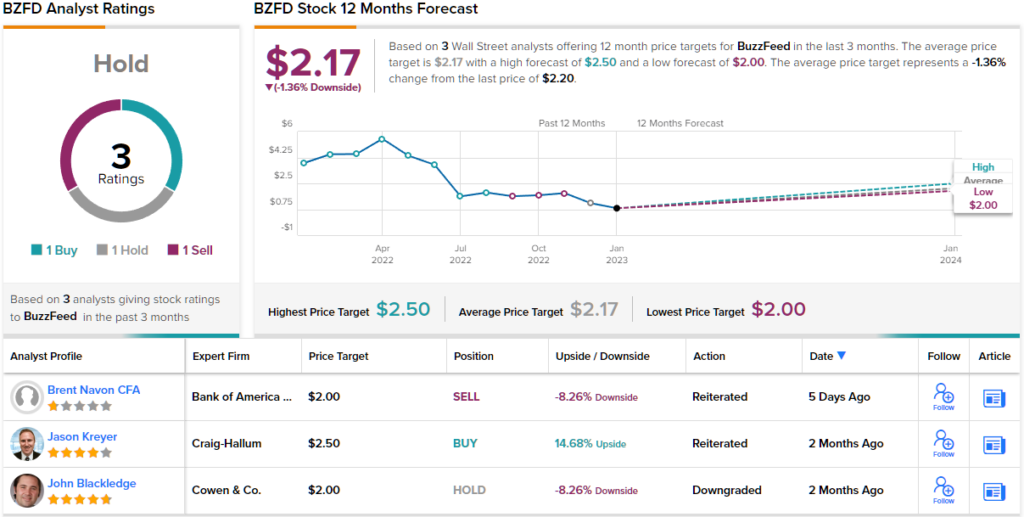

This stock has caught the attention of Cowen 5-star analyst John Blackledge, who has noted BuzzFeed’s uncertainty regarding monetization of its short-form video content and its vulnerability to reduced digital ad spending in a weak consumer spending environment.

Of the company’s recent moves to bring AI tech onboard, Blackledge writes: “While we think AI could eventually help BZFD generate more content at a lower cost (and drive higher engagement and advertising), timing and impact of their growing adoption of AI is unclear at this point.”

Overall, Blackledge is comfortable giving BZFD a Market Perform (i.e. Neutral) rating, with a price target of $2 that indicates potential for a 13% decline over the coming months. (To watch Blackledge’s track record, click here.)

The round-up of the analyst reviews on BuzzFeed shares comes out to an even split – 3 reviews, 1 each to Buy, Hold, Sell, adding up to a consensus rating of Hold. The average price target is $2.17, and current trading price is $220, suggesting shares will stay range-bound for the foreseeable future. (See BuzzFeed stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.