Hedge fund giant Izzy Englander managed a rare feat in life, when he turned his youthful interest in financial markets into a billion-dollar career. He started trading stocks as high school student, and opened his first brokerage in 1977 when he was 30. Eleven years later, in 1988, he raised $35 million in seed money and hung out the shingle of Millennium Management. He continues to serve as CEO of Millennium, which now holds more than $224 billion in assets under management.

Through his years of stock trading, Englander has held fast to a set of simple, basic rules in in all of his investments: Keep a lid on the risk, stick to non-directional trading strategies, and maintain the tight discipline required to stay with the first two rules. This combination of common-sense market savvy and discipline has guided Englander as he built his own fortune up to $6.6 billion.

Englander’s most recent 13F filing showed several new positions for his firm, and some of them share a few important attributes. Looked at through the lens of the TipRanks Stock Screener tool, these new positions hold Buy ratings among Wall Street’s analyst corps, and all show a dividend yield above 5%. Let’s take a closer look, to find out what else drew Englander to these investments.

Simon Property Group, Inc. (SPG)

First up is a real estate investment trust. Simon Property Group inhabits the retail segment of the REIT business, owning, developing, and managing a variety of regional malls, outlet centers, and other high-end retail spaces. The company is based in Indiana, and has operations across the United States and Canada. SPG is the largest mall operator in the US, with over 325 properties totaling more than 240,000,000 square feet.

SPG keeps up a generous dividend. The quarterly payment is $2.10, large in absolute terms as dividend payments go, and annualizes to $8.40 per share. The yield is an impressive 6.7%, far higher than the near-2% average among SPG’s S&P peers. The payout ratio is high, at 70%, but shows that there is still some slack available and that the company can maintain the dividend payment at current income levels.

With this in mind, Englander’s firm picked up 118,259 shares of SPG in Q4 2019, making the fund’s first position in this stock. The market value of the holding, at current prices, is over $14.4 million.

Wall Street is also bullish on SPG. Weighing in from Barclays, 5-star analyst Ross Smotrich places a Buy rating on the stock, with a price target of $191, suggesting an upside of 55%. (To watch Smotrich’s track record, click here)

Backing his view, Smotrich noted: “We continue to view SPG as the strongest positioned retail REIT to withstand industry challenges given its best-in-class properties, financial flexibility, solid balance sheet and liquidity position ($7.1 bln); in addition, management has demonstrated its focus on operations, cost structure, active portfolio management to achieve outstanding results for the company. SPG currently trades at a 28.7% NAV discount and 11.8x forw ard P/CAD multiple, a 9.8 turn discount to the broader REIT average (21.6x). In the interim, it is difficult to find a stock yielding 6.1% with a single A corporate debt rating.”

All in all, SPG’s Moderate Buy consensus rating is based on 4 Buys and 5 Holds set in recent weeks. The stock’s $158.33 average price target implies a premium of 29% from the current share price of $123.16. (See Simon Property stock analysis at TipRanks)

Medical Properties Trust (MPW)

As its name suggests, Medical Properties Trust is an REIT that focuses on hospitals and other health care facilities. The company has properties in the US, the UK and mainland Europe, and Australia. In addition to health care facility real property, the company also owns interest in several health care providers. MPT saw $854.2 million in revenue for 2019.

Investors can trust MPW’s dividend; the company has an 11-year history of keeping up reliable payments, and the March increase is the third in the past three years. The dividend annualizes at $1.08, for a yield of 5.01%. This is almost 2.5x the average among S&P listed companies, and almost 4x the yield of Treasury notes.

The attraction for Izzy Englander is clear, and it’s no wonder why he bought up 536,840 shares in MPW, which are now worth $11.9 million. Since the end of Q4, the value of this purchase has appreciated by over $600,000.

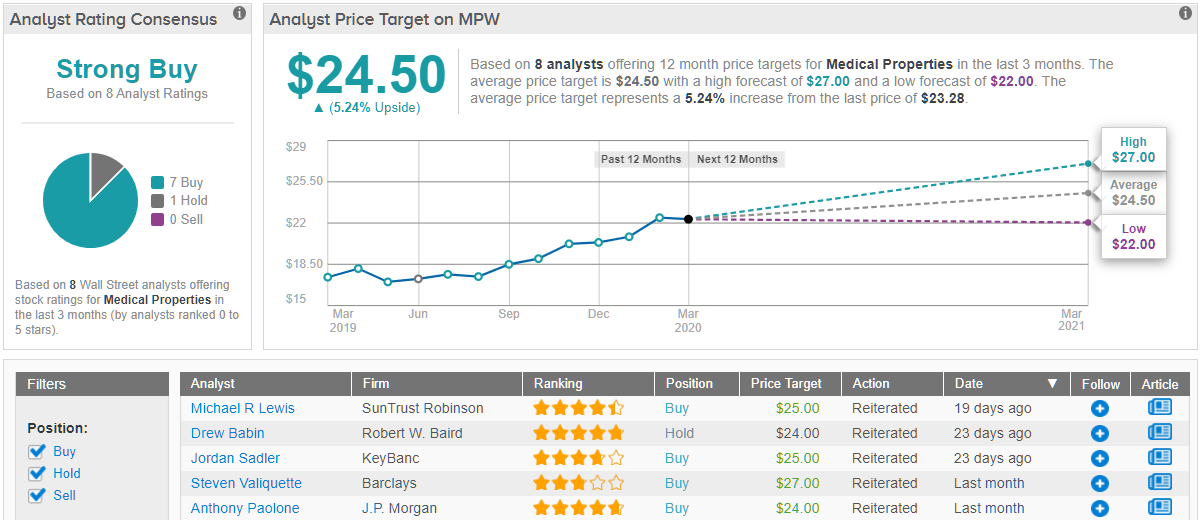

Barclays analyst Steven Valiquette likes what he sees in this company, saying bluntly, “MPW is on track to generate the highest FFO growth of any company in the HC REIT sector in 2020 and 2021, driven by a recent wave of investment activity.”

Valiquette puts a $27 price target on this stock, backing his Buy rating and suggesting an upside of 17%. (To watch Valiquette’s track record, click here)

Also bullish is Jonathan Petersen, 5-star analyst with Jefferies. He says of MPW, “We continue to expect MPW’s stock performance to depend on its ability to execute on its acquisition pipeline. With MPW’s strong balance sheet and continued appetite for further acquisitions, we see MPW continuing to grow into a healthy FFO/sh run rate throughout 2020, with further upside potential given somewhat conservative estimates on acquisitions beyond 2020.”

Petersen rates MPW a Buy, and gives it another $27 price target. (To watch Petersen’s track record, click here)

All in all, Medical Properties gets a Strong Buy from the analyst consensus, based on 7 Buys and just a single Hold. The stock is selling for $23.28, and the average price target of $24.50 suggests room for a 5% upside. (See Medical Properties stock analysis at TipRanks)

Weyerhaeuser Company (WY)

Last on our list is a major player in the North American timber industry. Weyerhaeuser owns some 12.4 million acres of timberland in the US, along with 14 million acres in Canada. The company produces a wide variety of timber, lumber, and other wood products. WY is incorporated as an REIT, deriving its income from royalties and production leases on the lands it owns.

WY has showed net growth over the last year, even accounting for the recent downturn. Shares are up a modest 11% in the last 12 months, and yoy the company shifted from a net loss in Q4 2018 to a positive EPS of 2 cents in Q4 2019. Net income for the quarter was $14 million on $1.5 billion in revenues.

The solid quarter supported the dividend payment, of 34 cents. Annualized, this comes to $1.36 per share, or a yield of 5.1%. As with the other stocks on this list, the yield is significantly higher than investors will find in other S&P assets or in the bond market. WY has a 9-year history of keeping up reliable dividends.

Growing profitability and a steady income stream likely attracted Englander to this stock, and his firm snapped up 656,956 shares, the largest buy among the stocks on this list. Millennium’s WT holding, another new position for the firm, is currently worth $17.56 million.

Stephens analyst Mark Connelly writes of WY, “Timberlands and wood products were stronger, and RE was slightly weaker than we expected… Management appears to have dropped its “dividend growth” story in favor of a “sustainable dividend”, which makes more sense given the business. We see no serious risk to the dividend.”

Connelly’s $32 price target implies an upside here of 17%, supporting his Buy rating. (To watch Connelly’s track record, click here)

5-star RBC Capital Analyst Paul Quinn gives an even more bullish $35 target to WY stock, suggesting a 28% upside to go along with his Buy rating.

In his comments, Quinn says simply, “Weyerhaeuser reported Q419 results that were in line with our forecast, with continued efficiency in its Wood Products segment… We think Weyerhaeuser is well positioned to benefit from lower interest rates and a stronger building season.” (To watch Quinn’s track record, click here)

Net net, Weyerhaeuser’s Strong Buy analyst consensus is unanimous, based on 3 Buy ratings. Shares are priced at $27.38, and the average price target of $33 indicates room for a 20% upside potential. (See Weyerhaeuser’s stock analysis at TipRanks)