Nokia announced on Monday that Thai mobile operator, dtac, part of Telenor Group, has selected the Finnish telecom network company as its first 5G RAN partner to supply coverage of the North and North Eastern regions of the country.

As part of the three-year deal, Nokia (NOK) will provide large-scale deployment of 5G on low-band spectrum (700-900Mhz) and high-capacity mmWave technology (26GHz). The telecom network operator will also be responsible for upgrading existing networks for faster data speeds to subscribers. The deployment is expected to begin later this year, with completion expected in 2022.

Specifically, Nokia will use its AirScale radio access solutions for 4G and 5G networks to improve overall network performance while allowing dtac to deliver 5G experience with ultra-low latency and strong capacity. AirScale radio access is an industry-first commercial 5G solution enabling operators to capitalize early on 5G. The deal includes digital deployment as well as optimization services.

“We are delighted to be the first vendor to partner with the operator in the 5G era,” Tommi Uitto, Nokia President of Mobile Networks, said. “Our AirScale portfolio offers a clear migration path to 5G and we look forward to supporting dtac with its efforts to deliver compelling 5G experiences to subscribers.”

Nokia has been a network provider in Thailand for over 30 years with the deployment of 2G, 3G and 4G networks.

Additionally, dtac will also deploy Nokia’s NetAct cloud network management system, which delivers cloud-agnostic tools for troubleshooting, administration, software management and configuration management.

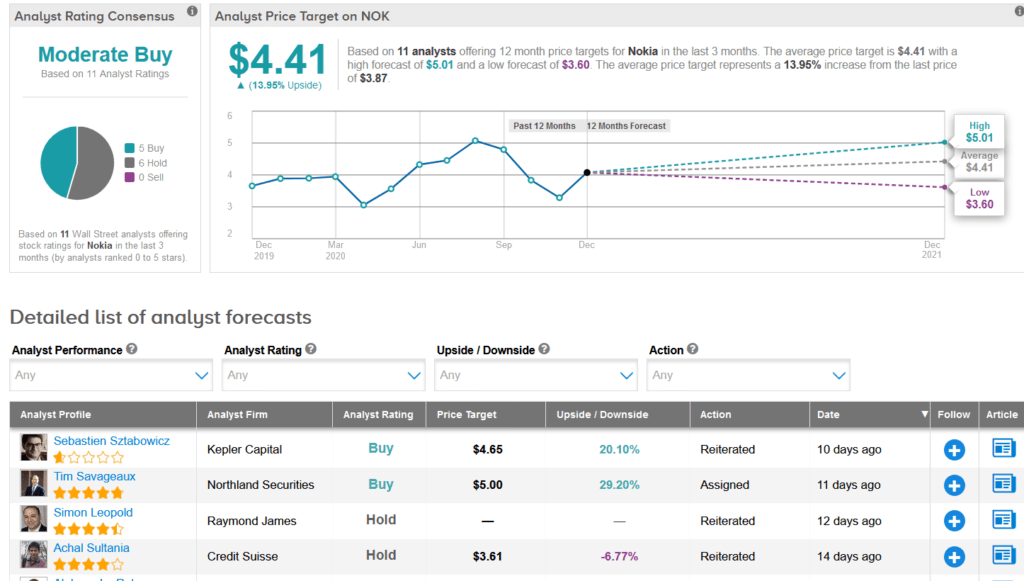

Shares in the Finnish telecom firm have lost 13% over the past six months after Verizon replaced the company as its 5G supplier in the US and chose Samsung as one of its main suppliers of radio equipment. On a year-to-date basis, the stock is now up 4.6%. Looking ahead, the average analyst price target of $4.45 implies upside potential of another 14% over the next 12 months.

Northland analyst Tim Savageaux, who recently reiterated a Buy rating on the stock with a $5 price target (29% upside potential), said he remains confident that NOK’s portfolio of assets is worth substantially more than $4 in both a break up scenario, the focus of the analyst’s March coverage initiation, and likely on a stand alone or turnaround basis as well.

“We assume significant declines in mobile revenues driving overall revenues down 6% in euro terms compared to a flat consensus top line for CY21, with R&D increases in mobile driving operating margins to the low end of a 7-10% guidance range,” Savageaux wrote in a note to investors. “While we applaud moves such as pushing 14K employees out from corporate functions and into business units and decentralizing decision making to business units, we would expect positive impacts from these moves in something under 3 years.”

The rest of the Street is cautiously optimistic on the stock. The Moderate Buy analyst consensus is split between 5 Buys and 6 Holds. (See Nokia stock analysis on TipRanks)

Related News:

Dish Plans To Sell $2B In Convertible Notes; Shares Drop 4.7% Pre-Market

Mastercard Sees Shift in Online Spending as U.S. Retail Sales Grow 3%

Nike or Under Armour: Which Stock Is A Better Retail Play?