Which strategy is a favorite of billionaires like Warren Buffet and Benjamin Graham? Value investing. This tactic, which involves looking for stocks that appear cheap when compared to their competitors on a price-to-earnings basis, hasn’t exactly been a fan-favorite among investors in the last decade. However, during a period riddled with uncertainty as a result of the COVID-19 pandemic, Wall Street pros are seeing merit in this approach.

The analysts from research firm RBC Capital are among those employing this strategy. The firm is one of TipRanks’ Top Performing Research Firms, landing within the top 10 out of 50 total firms, and it’s known for housing some pretty talented stock pickers.

With this in mind, we wanted to take a closer look at two stocks RBC’s analysts believe represent strong value plays, with each scoring upgrades from the firm in recent days. Running the names through TipRanks’ database, we learned that both have other bulls in their corners, based on all of the ratings received in the last three months. Let’s dive right in.

Clearwater Paper Corporation (CLW)

With manufacturing facilities located throughout the U.S., Clearwater produces consumer tissue, away-from-home tissue, parent roll tissue, bleached paperboard and pulp. Even though RBC hasn’t always been a fan of the company, the firm believes the tide is turning.

Representing the firm, five-star analyst Paul Quinn notes that CLW could finally be approaching an inflection point, citing its solid performance in its last two quarters as well as positive trends in its end-markets to support this claim.

Looking specifically at the most recent quarter, better-than-expected consumer products results drove CLW’s strong showing, with adjusted EBITDA of $55.4 million flying past Quinn’s $37.9 million call and the $42.1 million consensus estimate. During the quarter, demand was particularly strong, with shipments up 19% compared to historical averages. Management stated demand ticked up at the end of the quarter, and U.S. retail sales gained 90% year-over-year in March. The solid demand is also expected to persist for at least the next few months, even though it might have less of a material impact.

Expounding on this, Quinn said, “Under normal conditions, about a third of tissue is consumed away-from-home, which we expect has at least partially shifted to at-home consumption. In our view, this increased demand is supportive of increased tissue pricing, especially given that input costs are trending upwards (both recycled and virgin). Higher tissue prices would be positive for Clearwater revenue growth and margins.”

Adding to the good news, the paperboard segment also did well in Q1 as consumers stockpiled food, pharmaceuticals and other consumer packaged goods. It doesn’t hurt that two thirds of demand in the industry is fueled by “recession resistant” market segments, according to CLW. Despite the fact that WestRock is expecting to see some demand weakness in certain segments, Quinn argues that CLW has limited exposure in these areas.

Going forward, management believes it can continue this strong execution in the second quarter, guiding for adjusted EBITDA of $45-55 million, which is higher than Quinn’s original forecast. The analyst added, “Although there remains uncertainty due to COVID-19, management expects to see continued elevated demand in tissue as current production rates can surpass volume levels achieved in Q1. Higher volumes are likely to result in cost benefits for the segment as well.”

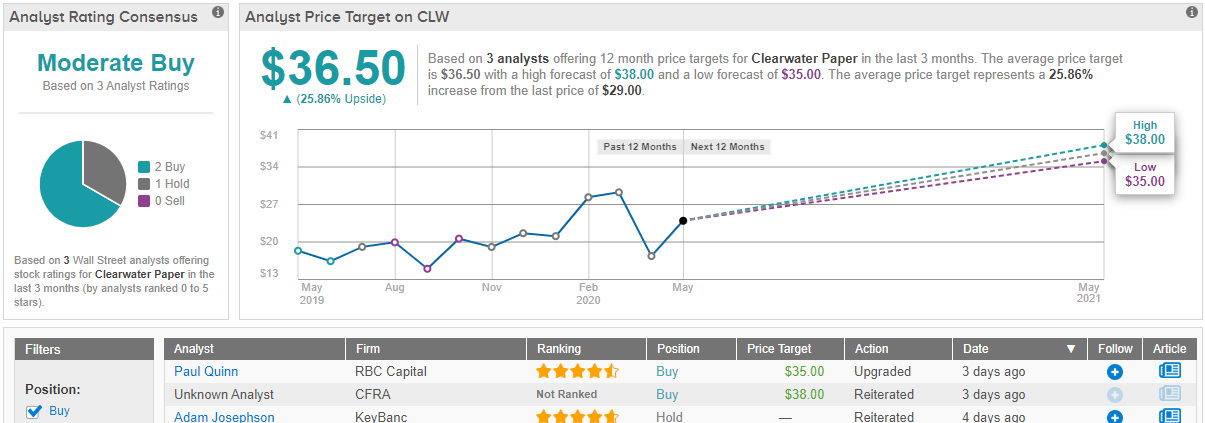

To this end, Quinn is joining the bulls. In addition to upgrading his rating to Outperform, he also lifted the price target from $20 to $35, implying 21% upside potential. (To watch Quinn’s track record, click here)

Turning now to the rest of the Street, CLW’s Moderate Buy consensus rating breaks down into 2 Buys and a single Hold. Not to mention the $36.50 average price target brings the upside potential to 26%. (See Clearwater stock analysis on TipRanks)

Adient PLC (ADNT)

Spinning off from Johnson Controls, Adient is one of the largest vehicle seating suppliers in the world, producing over 23 million seat systems every year. While there has been somewhat of a dark cloud looming over the company, RBC has been impressed by its ability to hold up during the storm.

Weighing in on ADNT for the firm, analyst Joseph Spak points out that liquidity, on a pro-forma basis for post quarter actions, comes in at around $2.26 billion. In addition, the company is planning on receiving an extra $575 million by full year-end from asset sales that were announced at an earlier date and about $200 million in JV dividends. “So with monthly cash burn down to just $175 million in a production environment similar to April, liquidity profile seems more than sufficient. Post crisis, cash on balance sheet only needs to be $500-$600 million,” the analyst explained.

On top of this, Spak cited CEO Del Grosso’s leadership as inspiring confidence. “Prior to COVID-19, we had seen sequential improvement in margins as signs that ADNT was improving performance through efficiencies, cost reductions, VAVE, and exiting non-profitable programs. Company was on track to beat FY20 targets pre-COVID,” he stated.

Spak doesn’t dispute the fact that managing complexity hasn’t always been one of ADNT’s strengths, but he argues that should manufacturers push back mid-cycle refreshes to save capital, it could result in lower volumes and some program specific delays. This is a good thing for the company as it would decrease system complexity. It could also give management a chance to assess and reduce SG&A even more.

With Spak also telling investors that ADNT will be able to reduce its debt when free cash flow generation resumes, the deal is sealed. Not only does the stock get an upgrade, from Sector Perform to Outperform, but the price target also gets a boost. The new $20 target implies shares could surge 13% in the next year. (To watch Spak’s track record, click here)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.