Will ServiceNow (NYSE:NOW) beat expectations in its upcoming earnings event? No guarantees can be made, of course, but I am bullish on ServiceNow stock as the company’s past results have demonstrated all-weather fiscal strength. Besides, ServiceNow stock is trading at a favorable price point – though some investors might observe some seemingly inflated valuation metrics.

Headquartered in California, ServiceNow provides cloud-based, artificial intelligence (AI) powered workflow automation software. To put it simply, it’s a well-respected company that helps businesses get work done more efficiently.

Yet, like so many tech stocks, NOW stock floundered in 2022. That’s not necessarily a problem, though, as an imminent quarterly report expected on January 25 could set ServiceNow stock back on its upward trajectory.

ServiceNow Suffered Tech-Wreck Collateral Damage

It’s certainly not ServiceNow’s fault that elevated inflation caused businesses to scale back their software upgrades. Nevertheless, NOW stock investors sustained collateral damage as the share price declined from $566 to less than $430 last year.

As we’ll discuss momentarily, ServiceNow continued to deliver outstanding bottom-line results throughout 2022 despite macroeconomic headwinds. First things first, though: did the share-price drawdown create an irresistible bargain for value hunters?

If you rely exclusively on traditional valuation multiples and ignore everything else, you might be dissuaded from investing in ServiceNow. I’ll be the first to admit that ServiceNow’s 432.9x P/E ratio, 20x P/B ratio (I generally prefer 3x or less), and 12.9x P/S ratio (I would rather see 5x or less) are higher than some financial traders would want to see.

If those numbers are a deal-breaker for you, that’s understandable. Just bear in mind that modern technology companies can sometimes defy traditional metrics, and their stocks can march relentlessly higher despite elevated valuations. So, open-minded investors might be willing to overlook or forgive ServiceNow’s high multiples, especially after delving into the company’s impressive earnings history.

ServiceNow Has a Stellar Earnings Track Record

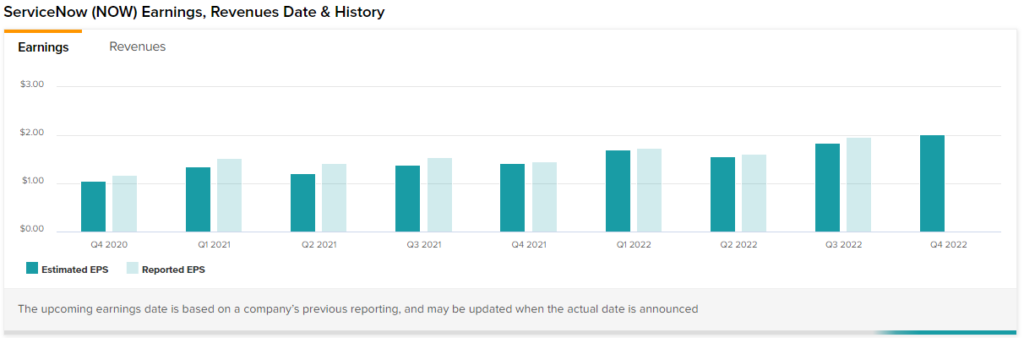

So, did you mark your calendar for January 25 yet? That’s when ServiceNow plans to release its fourth-quarter earnings data. Analysts have high hopes, and based on the company’s amazing track record, ServiceNow should be able to meet or beat Wall Street’s expectations.

Here’s something you can’t say about every exchange-listed company: believe it or not, ServiceNow has managed to exceed analysts’ consensus EPS estimate in every quarter since early 2018. Plus, ServiceNow’s EPS has grown substantially over the past several years.

For Q4 2022, analysts expect ServiceNow to report EPS of $2.02, and that’s the highest expected EPS figure in recent memory for this company. Yet, ServiceNow should be up to the task. During Q3 2022, the company grew its subscription revenue by 22% year-over-year while also increasing its big-ticket customers (the ones paying over $10 million in annual contract value) by an eye-popping 60%.

In other words, ServiceNow maintained a powerful growth trajectory even when the economy was shaky and NOW stock was in decline. This divergence between share price and operational results might convince investors to buy ServiceNow stock even if the company’s valuation multiples are elevated.

It’s also worth noting that ServiceNow’s non-GAAP subscription gross margin has been quite high. In fact, that margin has stayed at 85% or 86% since Q3 2021. Moreover, the company’s non-GAAP total gross margin was 81% to 83% during that time. This is significant, as it indicates that ServiceNow can turn a sizable profit on its products.

Is NOW Stock a Buy, According to Analysts?

Turning to Wall Street, NOW stock comes in as a Strong Buy based on 18 Buys and two Hold ratings. The average ServiceNow stock price target is $504.05, implying 14.1% upside potential.

Conclusion: Should You Consider ServiceNow Stock?

Clearly, Wall Street has high expectations for ServiceNow. There are plenty of Buy ratings, and analysts envision another impressive EPS print from ServiceNow. Admittedly, some folks might scrutinize the company’s metrics and choose to stay on the sidelines. Yet, that decision could lead to regret and a missed opportunity.

Investors ought to consider NOW stock now before the company unleashes what’s likely to be another set of expectation-beating earnings results. For a high-growth, high-margin, and high-conviction software specialist, you likely won’t find many better earnings-blowout candidates than ServiceNow.

Join our Webinar to learn how TipRanks promotes Wall Street transparency