Nearly four months after the coronavirus sent Mickey Mouse and Co. home, Disney’s (DIS) Disney World re-opened for business on Saturday. While not operating at full capacity and working under strict social distancing guidelines, it remains to be seen whether the move pays off, as Florida is still nowhere near flattening the curve of COVID-19 cases.

For the past 3 months, Disney shares have roughly followed the overall market’s trajectory, as shares are up by 15%, nearly the same as the S&P 500’s gain in the period. Goldman Sachs analyst Brett Feldman expects Disney to continue the upward trajectory over the next year.

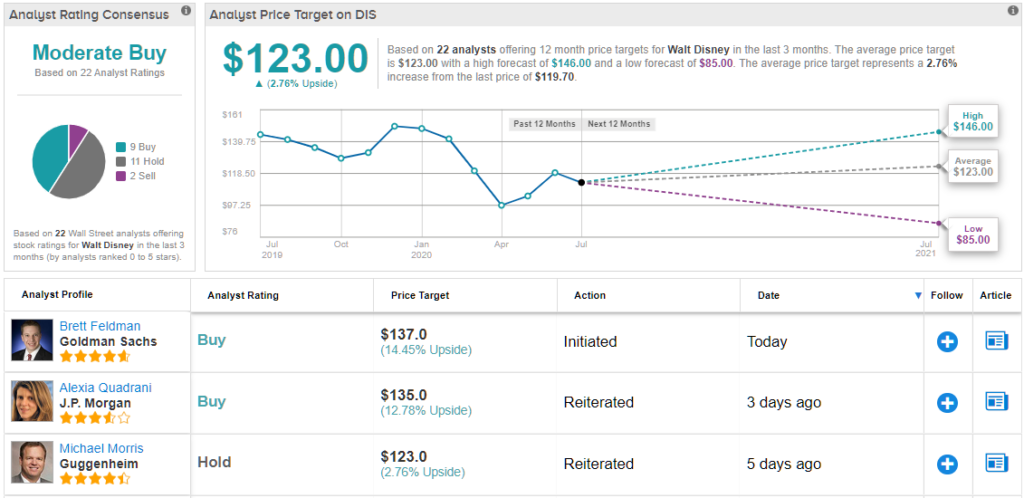

In a research note issued today, Feldman initiated coverage on DIS with a Buy rating and $137 price target, which implies about 15% upside from current levels. (To watch Feldman’s track record, click here)

Driving the majority of Feldman’s thesis is Disney’s pivot toward the DTC (direct to consumer) market. Feldman believes Disney’s “best-in-class brand, global distribution (breadth), production assets (build), sizable content library (backlist) and strong financial profile (balance sheet) position the company to build scaled DTC video platforms in the highly competitive streaming environment.”

The benchmark in this environment is industry leader Netflix. With a current subscriber base of 50 million – the same as Netflix had in 4Q14 – the analyst expects Disney+’s gross margins to improve from 24.6% with operating income losses in C2Q20 (worse than Netflix in 2014) to a gross margin of 46.9% and an operating income margin of 19.7% by C3Q25 (closer to Netflix figures in 1Q19).

This is based on an expectation that by 2025, Disney+ will boast more than 150 million customers. In fact, the analyst believes that figure is a conservative one, given his belief there is a 712 million global market to address.

Long before that, Feldman expects Disney+ to turn a profit. While consensus estimates Disney+ to swing into the green by F2023, Feldman estimates this will happen in F2021, based on the premise that as “Disney+ approaches Netflix-like scale it will approach Netflix-like economics.”

Continuing with the Netflix comparison theme, the analyst maintains the Street is underestimating Disney+’s potential.

Based on implied 2022E subscriber valuations of $374 for Disney+ vs. $878 for Netflix and revenue multiples of 3.5x for Disney+ vs. 6.6x for Netflix, Feldman argues the market is “valuing Disney’s DTC segment at an almost 50-60% discount to Netflix.”

“Based on our outlook for Disney+ to approach Netflix-like scale and economics over the next five years,” the analyst said, “We believe such a material discount to this peer is unwarranted, and expect this valuation gap to close as Disney+ ramps its customer base and achieves profitability.”

So, that’s the Goldman Sachs view. Turning now to the rest of the Street, where Disney’s Moderate Buy consensus rating is based on 9 Buys, 11 Holds and 2 Sells. The average price target hits $123 and implies potential upside of 3% over the next 12 months. (See Disney stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.