Onward and upward the market goes, with December providing further cheer as new record highs for the S&P 500 were notched in the last week. Giddy from 2019’s riches and ready to bring in the New Year, the optimism on the Street, following a brief slump, has been renewed.

While analysts are divided as to whether the next year can follow this one’s record breaking run, one thing looks certain; investors will still be on the lookout for the right addition to their portfolio.

TipRanks – a company that tracks and measures the performance of analysts – has an instrument that comes in handy here. The Daily Stock Ratings tool allows a user to see what stocks are hot and, yes, what stocks are not. Analysts’ ratings and their performances are displayed, too, further helping the intrepid investor make the right decision.

Let’s have a look, then, at 3 Buy-rated stocks a number of the Street’s leading analysts recently pulled the trigger on.

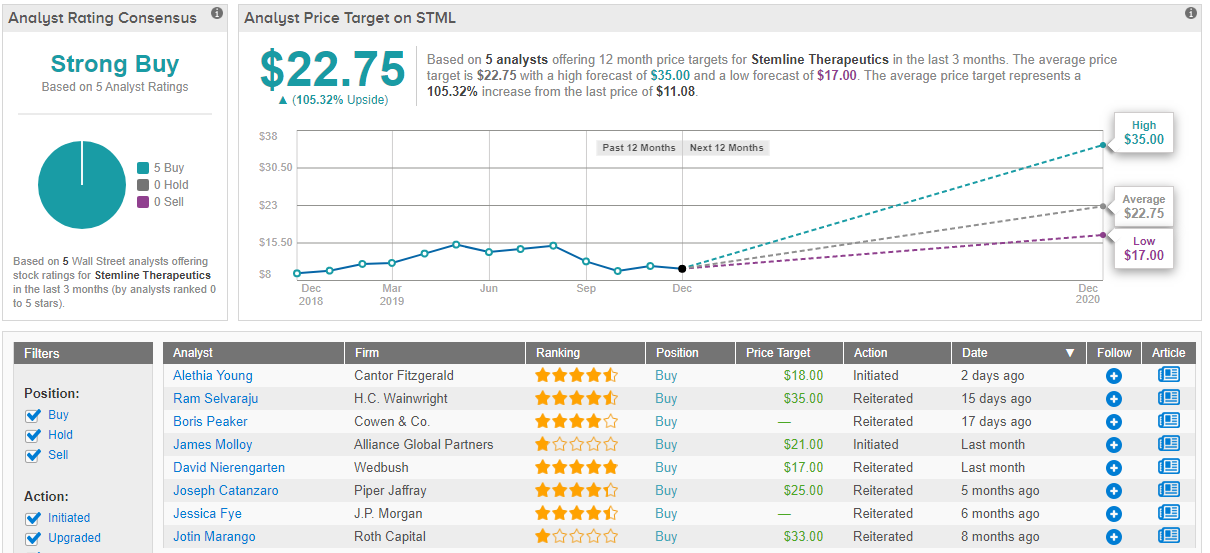

Stemline Therapeutics Inc (STML)

With a focus on developing and bringing to market novel oncology therapies, Stemline Therapeutics has recently been turning heads on the Street.

The New York based biotech has several therapies in the pipeline, but already has one on the market. Elzonris is used to treat a rare blood cancer called blastic plasmacytoid dendritic cell neoplasm (BPDCN), and was approved by the FDA in December 2018 for the treatment of adults and pediatric patients over 2 years old. The drug is currently in clinical trials to assess further indications.

Cantor Fitzgerald’s Alethia Young calls Elzonris a “pipeline in a product” and believes the biotech is undervalued. Stemline’s market cap is currently $555.4 million, and Young expects sales from Elzonris for BPDCN (sans maintenance therapy) to be in the region of $150 million by 2025. We’re talking about just the US here. Furthermore, the 5-star analyst thinks the possible expansion of Elzonris into the BPDCN maintenance setting in 2021 could, by 2029, result in US sales of $223M. Young maintains that as “as investors take notice of progress in the label expansion opportunities”, the next 12 months should see Stemline’s share price take off.

Accordingly, Young initiated coverage on Stemline with an Overweight rating and set a price target of $18. This implies upside potential of 62% over the next 12 months. (To watch Young’s track record, click here)

The Cantor analyst’s bullish thesis is mirrored by that of the Street’s. All 5 analysts tracked over the last three months rate the stock a Buy, and therefore, Stemline has a Strong Buy consensus rating. An average price target of $22.75 outstrips Young’s target and indicates gains of 105% could be in the cards. (See Stemline stock analysis on TipRanks)

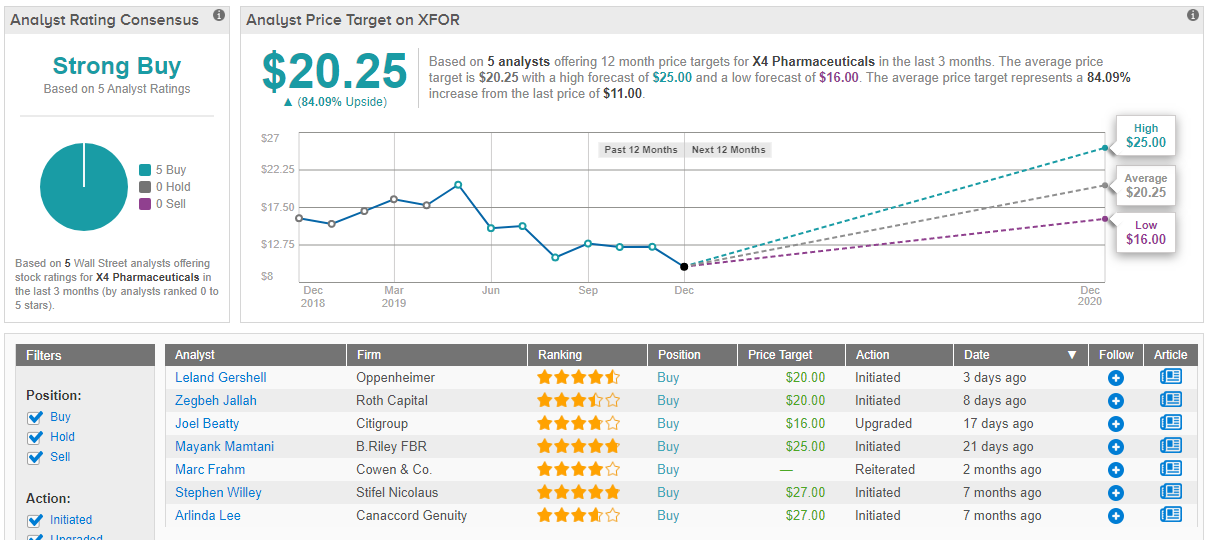

X4 Pharmaceuticals Inc (XFOR)

The biotech sector’s recent upturn in the market hasn’t, unfortunately, had any effect on X4 Pharmaceuticals. The rare disease focused biotech has had a rough year in the market, and its share price is down by 21% year-to-date. The word on the Street, though, is that this is all about to change.

The company has several drugs in the pipeline, but its lead candidate is mavorixafor (X4P-001), currently in Phase 3 development for the treatment of WHIM syndrome. The rare, inherited condition is an immunodeficiency disease caused by genetic mutations in the CXCR4 receptor gene. Designated orphan status by the FDA in 2018, the drug is also in development for several other conditions, including Waldenström’s macroglobulinemia (WM).

Roth Capital’s Zegbeh Jallah highlights XFOR’s “well experienced team” which includes Dr. Renato Skerlj, who developed the first CXCR4 antagonist (plerixafor), as making it a stand-out. Jallah also bases his bullish thesis on a “strong conviction around the clinical and commercial outlook” of mavorixafor, and “a robust pipeline of optimized CXCR4 modulators that could offer improved benefits across a broader range of diseases.” As a result, the analyst initiated coverage of X4 with a Buy rating and a price target of $20, indicating handsome upside potential of 82%. (To watch Jallah’s track record, click here)

A fellow analyst praising XFOR is Oppenheimer’s Leland Gershell. The 5-star analyst expects the drug to gain approval for WHIM syndrome and remains “cautiously optimistic” about its part to play in Waldenstrom’s macroglobulinemia. Leland initiated coverage with an Outperform rating and a price target of $20, too. (To watch Gershell’s track record, click here)

3 other analysts have chipped in with a take on X4 over the last three months and all have reached the same conclusion: Buy. Therefore, the rare disease specialist has a Strong Buy consensus rating. The average price target of $20.25 could provide investors with gains of 84% over the next 12 months. (See X4 Pharmaceuticals stock analysis on TipRanks)

See also: 3 “Strong Buy” Energy Stocks with Electric Upside Potential

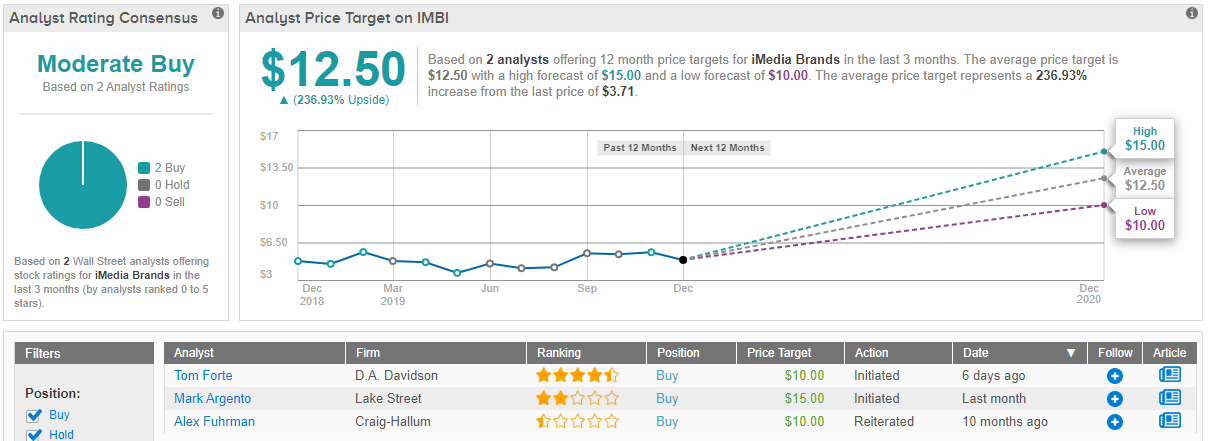

iMedia Brands Inc (IMBI)

Moving on from the biotech industry, we encounter a fellow struggler. Although in a completely different industry, multiplatform commerce company iMedia Brands hasn’t had much joy in 2019, either. Languishing in the doldrums, the company has a year-to-date loss of 7%.

That being said, iMedia has an expanding portfolio of shopping television networks and new media businesses including ShopHQ and iMedia Web Services. November saw new additions to the list, too. The first, Float Left Interactive, an OTT (over the top) and TVE (TV everywhere) service provider, has launched a string of OTT apps and counts NBC, Comcast and CBS among its clients. The second, J.W. Hulme, is a maker of leather bags and accessories, and will get its own programming on ShopHQ’s cable channel.

So, with the new developments in place, is now the right time to get in on iMedia? It is according to D.A. Davidson’s Tom Forte. The 5-star analyst forecasts iMedia revenue to grow by 3% per year over the next three years and projects that by 2022, the company’s EBITDA margin will expand by almost 500 basis points to 3.1%.

Furthermore, with LaVenta, the company’s new omni-channel, Spanish language, television shopping network launching in Q1 2020, Forte acknowledges iMedia’s potential for expansion outside the US.

To this end, Forte initiated coverage on the interactive media company with a Buy rating, alongside a price target of $10. The bullish target indicates upside potential of a whopping 170%. (To watch Forte’s track record, click here)

iMedia currently has only 1 other analyst assessing the company’s 12-month potential, but he happens to be a vocal fan, too. Lake Street’s Mark Argento reckons the next year could see iMedia’s share price reach $15, which lends itself to a massive 305% increase from the current price. (To watch Argento’s track record, click here)

Put together, the media company has a Moderate Buy consensus rating and an average price target of $12.50. Potentially, then, investors could be lining their pockets with a 237% gain next year. (See iMedia price targets and analyst ratings on TipRanks)