There are new hopes for the revival of the Chinese economy. With the easing of the zero-COVID policy as well as relaxed Beijing’s tech crackdown, I believe the top Chinese technology and entertainment conglomerate Tencent Holdings (OTC:TCEHY) is all set for its long-due turnaround. Plus, its cheap valuation makes it a compelling stock, in my opinion.

With the sight of the rebound of the Chinese economy around the corner, let’s take a deeper look at Tencent Holdings.

The Issues Put to Rest

Last month, Chinese stocks got a fresh lease of life, witnessing their biggest rally in the last two decades. A volley of positive news buoyed most Chinese stocks. Talks between U.S. President Joe Biden and Chinese President Xi Jinping have given signs of easing tension between the two nations. With that, the ever-growing concern of the delisting of Chinese stocks from the U.S. stock markets is also put to rest.

At the same time, China is becoming more lenient on its travel restrictions and its zero-COVID policy to help revive the ailing economy and return to normalcy. The much-awaited reopening of the Chinese economy and the final exit from its zero-Covid policy bodes well for all the Chinese stocks listed overseas.

Since last year, Chinese regulators suspended gaming licenses and imposed acrimonious restrictions on the gaming sector. For instance, minors’ game times were capped at three hours a week. The good news is that the regulators have relaxed their tough stance on the sector. In November, 70 domestic titles were approved, bringing new hope to the gaming industry overall and especially the Chinese gaming giant Tencent.

Tencent’s Mixed Q3 Results

On November 16, Tencent reported mixed Q3 results, with revenues continuing to decline for the second straight quarter but earnings showing some signs of growth. Revenues declined 2% year-over-year to 140.1 billion yuan, or $19.7 billion, and lagged Street estimates of 141.6 billion yuan. On the positive side, net profit grew 1% year-over-year to 39.9 billion yuan, or approximately $5.6 billion.

Tencent’s videogame business continued to struggle, declining 4% year-over-year to around 42.9 billion yuan due to China’s gaming restrictions.

However, that number will potentially see a revival as Tencent won approval for its first new major game, “Metal Slug: Awakening,” last month. There are clear signs of Chinese regulators easing restrictions on the mobile entertainment industry with the resumed grant of gaming licenses. This restores confidence in the gaming giant Tencent to launch more games, which should benefit Tencent’s video games business segment in the upcoming quarters.

Another major highlight of the Q3 results was the announcement a special dividend worth $20 billion. Interestingly, the special dividend comes in the form of shares of online food delivery and travel firm Meituan Dianping (OTC:MPNGF).

Tencent has a ~17% stake in the company. With the payment of the special dividend, Tencent will exit almost its entire stake in the company. 1 Meituan share will be paid for every 10 Tencent shares held. This equates to a special dividend of HK$13.60, which will be paid to shareholders in March 2023.

This is a clear sign that Tencent is serious about its business re-organization initiatives. It aims to enhance its focus on acquiring synergistic gaming companies outside China, shut down non-core businesses, and enable cost-cutting measures.

Tencent and Its Competitive Advantage

While Tencent stock has taken a massive hit in recent years due to numerous issues, I continue to like the stock for various reasons. Tencent has a big competitive advantage in the gaming industry as it is vertically integrated. Its gaming operations span across the value chain with game development, game publishing, and game distribution verticals.

It has a strong advantage from its ability to direct traffic to its games through WeChat and Yingyongbao. WeChat is an instant messaging, social media, and mobile payment app and is also Tencent’s most powerful tool. It has a large, engaged, and sticky user base, making it a valuable customer acquisition tool.

Tencent has a sturdy balance sheet with a stable cash position as well as impressive stakes in leading global tech companies, including Tesla (NASDAQ:TSLA), JD.com (NASDAQ:JD), etc.

TCEHY has an extremely strong moat which is driven by two key sources: 1) the Network effect from its massive user base and 2) high-quality user data.

In terms of its valuation, too, Tencent is extremely cheap. Currently, it’s trading at an attractive P/E ratio of 15x compared to much higher multiples of its peer group. Chinese internet search company Baidu (NASDAQ:BIDU) is trading at a P/E of 71x, while China-based technology-driven e-commerce company JD.com is trading at over 300x.

In addition, its current valuation reflects a huge discount from its five-year average of 40x. These are attractive discount levels and present a great buying opportunity given the strong growth potential for the market leader.

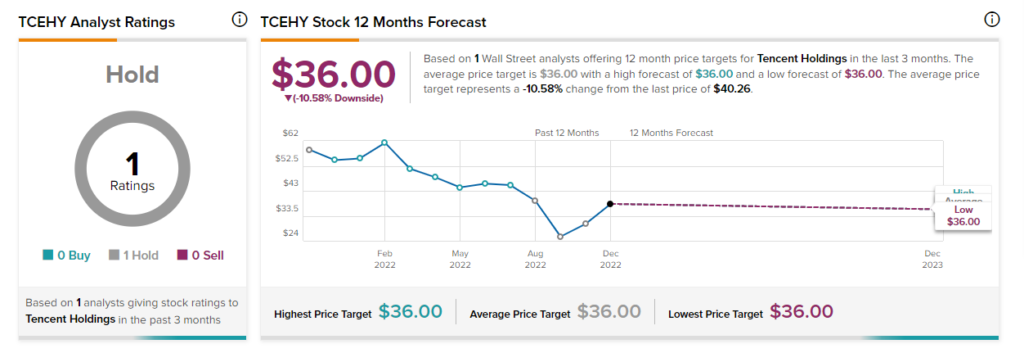

Is TCEHY a Buy or Sell, According to Analysts?

As per TipRanks, Tencent Holdings stock has received one rating over the past three months. Barclays analyst Jiong Shao assigns a Hold rating on Tencent Holdings with a price target of $36 (10.6% downside potential).

Concluding Thoughts: Tencent Looks Attractive

Like most Chinese stocks, Tencent Holdings has been out of favor due to many reasons like strict government regulations for the Chinese technology sector, the crackdown on monopolistic practices, and the possible delisting from the U.S., to name a few.

Tencent stock is down 30% over the past year despite its recent rally of 30% over the past month.

There are clear signs of a revival for Tencent as well as the Chinese economy in 2023. The stock could show a sharp recovery and reach or perhaps even cross its historical highs. I am bullish on TCEHY and will buy at current levels.