One small step for man, one giant leap for… investors looking into aerospace stocks heading to the moon?

Talk of a looming recession has been a theme among investors this year. Whether a recession hits or not, Goldman Sachs notes that one sector in particular usually performs well as the market enters into such unpredictable territory, namely Aerospace and Defense.

The space has plenty of good stocks, but naturally investors are looking for the right ones to put their hard-earned cash into. Using TipRanks’ Stock Screener tool, we locked in our focus on 3 aerospace stocks the analysts think are ready for lift off heading into 2020.

AeroVironment, Inc. (AVAV)

Our first aerospace pick is the aptly named, AeroVironment. The company makes unmanned aircraft systems and is the Pentagon’s top supplier of small drones — including the Raven, Wasp, and Puma models. The Raven holds the lofty title of “the most widely used military unmanned aircraft system in the world”.

The drone manufacturer has been keeping busy. AeroVironment recently secured a $12 million contract from an unnamed Middle Eastern country to supply logistics, parts, and services for an existing fleet of Puma and Raven aircrafts, alongside a $55 million U.S. army contract to begin radio frequency modifications on its Raven fleet.

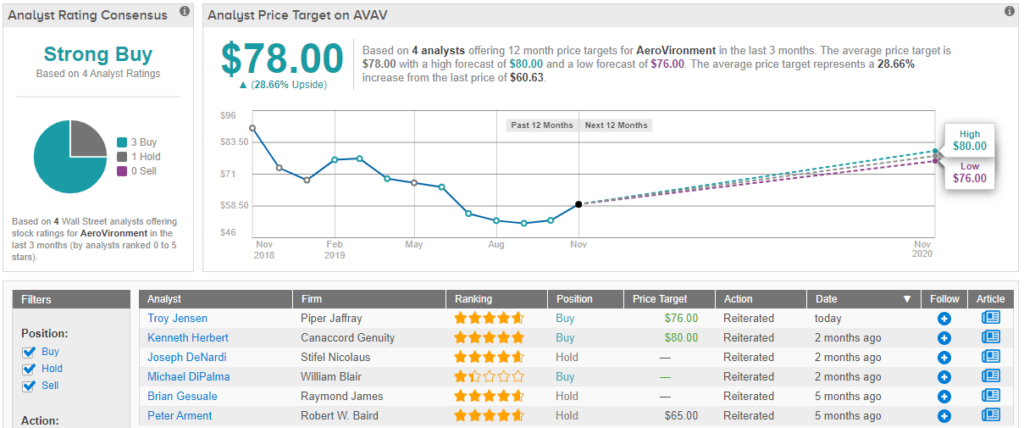

The company is profitable, has cash in the coffers, and Piper Jaffray’s Troy Jensen thinks now is the time for investors to take note. The 5-star analyst said, “We believe the recent pullback in AVAV shares has created a more compelling entry point and we continue to believe the company will execute on a variety of growth initiatives throughout FY20 and beyond. We continue to believe AVAV will benefit as U.S. defense budgets shift more toward unmanned aircraft and international defense sales should grow even faster than domestic sales, given its recent focus on international expansion”.

Putting his money where his mouth is, Jensen upgraded his rating on AVAV from Hold to Buy and increased his price target to $76 (from $66). (To watch Jensen’s track record, click here)

The Street is set to join Jensen on the launch pad, as AVAV currently has a Strong Buy consensus rating, which breaks down into 3 Buys and 1 Hold. The average price target is $78, implying 29% upside from its current price of $60.63. (See AeroVironment stock analysis on TipRanks)

Aerojet Rocketdyne Holdings (AJRD)

It is hard to sound more impressive than a company that essentially designs spacecrafts, but then Aerojet Rocketdyne does what it says on the tin. It supplies aerospace and defense products to the U.S government’s major space and defense contractors.

The company recently notched a world’s first when it showcased an Advanced Electric Propulsion System (AEPS) thruster at full power which will be used for NASA’s Gateway, an orbiting lunar outpost for robotic and human exploration operations in deep space. Woah.

Back down on earth though, Aerojet recently posted a disappointing 3Q19 report. Revenues fell 3.4% year-over-year to $481.8M, below the Street’s estimate of $505.4M. EPS of $0.35 was also lower than the Street’s estimate of $0.44.

However, SunTrust Robinson’s 5-star analyst Michael Ciarmoli believes the company’s lighter bookings and revenue weakness were more to do with timing than specific problems. Citing Aerojet’s ability to build and generate cash at a strong pace as well as the excess of $650M on its balance sheet, he argues that investors should feel reassured.

Ciarmoli said, “In our view, AJRD remains an underfollowed SMID-cap defense contractor poised to benefit from favorable defense spending and space-based trends… We believe ongoing operational improvement efforts, recent leadership changes, and the potential to reengage with Wall Street, all will positively influence shares in the near-term.” To this end, the analyst reiterated his buy rating alongside a price target of $55.00 implying upside potential of 26%. (To watch Ciarmoli’s track record, click here)

Canaccord Genuity’s Kenneth Herbert is another analyst predicting lift off for the rocket designer. After recently meeting the company’s management, the 5-star analyst came away impressed, noting, “The 2020-2021 MSD top-line growth is expected to be driven by defense sales (THAAD, Standard Missile, GMLRS, Hypersonics), while space sales re-set at a higher run rate after strong 2019 growth (NASA up ~15% YTD). While much of the margin improvement is reflected in results, we believe top-line growth and capital allocation will be positive catalysts.” (To watch Herbert’s track record, click here)

The Street is relatively quiet right now regarding Aerojet. With 2 Buys and 1 Hold, AJRD currently ranks as a Moderate Buy. The aerospace specialist, though, has an average price target of $53.00, which implies an increase of 22% from its current price of $43.60. (See Aerojet stock analysis on TipRanks)

Textron (TXT)

Textron was founded in 1923 as a textile company but through its expansion and metamorphosis, a century later it is a multinational company with over 35,000 employees worldwide and several big-name subsidiaries under its umbrella, including Bell, Cessna, Beechcraft, E-Z-GO, and Arctic Cat.

The company experienced a bit of a sell-off following its recent Q3 report, due to what investors saw as underwhelming performance – the company reported a beat on earnings but missed on revenue. Sector wise, aviation saw notable growth, along with the industrial division. On the other hand, TXT Systems underperformed.

Jeffries’ Sheila Kahyaoglu recently met up with company management and following the meeting had some key takeaways, noting, “The tone of the meeting was subdued on the business jet demand environment, with the upside in the portfolio from defense programs including FARA, FLRAA, Navy Trainer, and AT-6.”

Highlighting the multinational’s diverse holdings, the 5-star analyst added,” We believe TXT has the potential for significant organic growth given its new product pipeline. Improved market dynamics and some investment holiday should lead to higher earnings in 2019/20. We think this growth outlook is not reflected in the current ~25% valuation discount to peers on an EV/EBITDA basis.”

The 5-star analyst reiterated her buy rating on TXT. Her price target remains a bullish $65.00, implying handsome upside potential of 38%. (To watch Kahyaoglu’s track record, click here)

Overall, the Street’s sentiment on TXT stock is mixed, giving the multinational a Moderate Buy rating alongside an average price target of $54.40. This implies upside of almost 17% from its current price of $46.37. (See Textron stock analysis on TipRanks)