In this piece, we used TipRanks’ Comparison Tool to evaluate two real estate investment trusts that address different corners of the market. I believe that these REITs might perform well in a rising interest rate environment.

With inflation skyrocketing and the prospects for a recession rising, investors are scrambling for recession-resistant investments. Real estate is one sector that offers protection against inflation, but the lack of liquidity and challenges in purchasing property will put some investors off.

As a result, real estate investment trusts (REITs) may offer a way for investors to tap into the real estate market with ease. They offer the benefits of investing in real estate without many of the headaches that go along with it.

A deep analysis reveals reasons to be bullish on both Prologis (PLD) and Digital Realty Trust (DLR). Investing in both can offer diversity through exposure to both warehouses and data centers — two areas that are both thriving right now.

The Bull Thesis for REITs

Many investors hurry to dump their REIT stocks during periods of rising interest rates, but contrary to popular opinion, history shows that rising rates aren’t necessarily bad for real estate investment trusts. According to NAREIT, REITs have averaged a 15% yearly return over the last two decades. The organization also reported that REIT dividends had outpaced inflation as measured by the consumer price index in all but two of the previous 20 years.

S&P Global Market Intelligence also reported more recently that REITs had been slightly outperforming the S&P 500 during the rising-rate period that began in late 2020. The Dow Jones Equity All REIT Index has generated an annualized return of 11.7% since August 4, 2020, compared to the S&P’s 10% total annualized return as of July 1, 2022.

Before that period, REITs had outpaced the index in four of seven previous rising-rate periods since 2000. In addition, even when they underperformed the S&P 500, they still generated positive total returns in each period of rising rates.

Investing in REITs also makes sense during inflationary periods because they can benefit from their ability to increase their rents, offering protection from inflation. Of course, not all REITs are created equal, but warehouses and data centers are two parts of the market that look promising in the near term.

Another reason to invest in REITs is the fact that they generally make excellent dividend stocks. In order to continue enjoying their tax benefits as real estate investment trusts, they must pay at least 90% of their net earnings to shareholders in the form of dividends.

Prologis

Like many other stocks, Prologis is down about 21% year-to-date, although it is up more than 11% over the last month. The company is the largest industrial REIT by far, with holdings in almost 4,700 buildings and almost 1 billion square feet of space leased to around 5,800 tenants as of the end of 2021. Prologis has some very high-profile customers leasing its space, including e-commerce giant Amazon.

The company also benefits from some critical nationwide trends, such as the warehouse shortage. Commercial real estate services firm JLL estimates that about 1 billion worth of new industrial space is needed by 2025 to keep up with current levels of demand. Growing e-commerce activity and faster delivery rates are boosting demand across the country, making Prologis an attractive play.

Beyond the national trends, the company also enjoys robust fundamentals. Prologis reported $1.33 billion in revenue during Q2, a year-over-year increase of about 9%, and $0.82 per share in diluted earnings, an increase of about 1%. Prologis also beat the consensus estimates for earnings per share and revenue.

In its latest analysis on the industrial sector, the company reported that the average national vacancy rate has declined to a national record low of 3.1%. Prologis also noted that this low vacancy rate enabled it to raise its rents by about 7% during the second quarter.

Reports have suggested that Amazon and other big names are returning industrial space to the market, but Prologis management dismissed those concerns. On their recent earnings call, they said the retention rate for space leased to Amazon was 95%, 20 percentage points higher than the company average.

Prologis management also said the industrial market could soften this year, but only against periods of unprecedented records in demand, leasing, and rent growth across the sector. Additionally, shortages of materials and open land are presenting barriers to entry for anyone who would build new warehouses to compete with Prologis.

Finally, Prologis has a unique quality that many investors overlook. The company has taken advantage of its numerous buildings by placing solar panels on their expansive roofs, making it the nation’s third-largest private solar provider. On the negative side, however, Prologis stock has dived since its April highs, primarily due to its planned acquisition of logistics REIT Duke Realty, which most shareholders opposed.

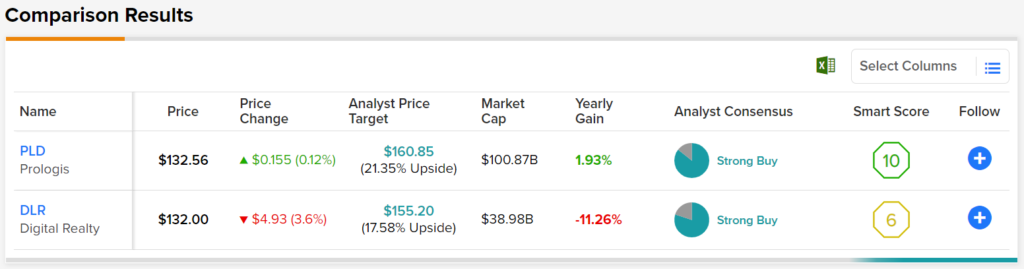

Prologis has a Strong Buy consensus rating based on 12 Buys and two Holds assigned in the last three months. At $161.77, the average Prologis price target implies upside potential of 28.64%.

Digital Realty Trust

Digital Realty Trust shares are down 20% year-to-date but up 3% over the past month. One of the biggest concerns for Digital Realty and other data center REITs right now is a recent short report put out by well-known short-seller Jim Chanos. He sees the big problem for these properties as “technical obsolescence.” In his view, the three biggest customers are becoming these companies’ biggest competitors.

Chanos believes that while the cloud is growing, the cloud is also “their enemy, not their business.” He argued that hyperscalers like cloud giant Amazon Web Services will build their own data centers and stop using those owned by REITs such as Digital Realty.

However, in an interview with CNBC, Digital Realty management said that demand in their space has “never been stronger” and that they’ve had record bookings in the last two quarters. They also said they’ve been raising their rental rates, which makes sense and demonstrates that the company is resistant to inflation because it can pass its higher costs onto customers.

Wells Fargo analysts also refuted Chanos’ short report, saying that hyperscalers are finding it difficult to build their own data centers due to tight supply and long delivery times for equipment and power. They described Chanos’ thesis as “unoriginal” because they had been hearing the same one for over five years, and it hasn’t come to pass.

Digital Realty Trust has a Moderate Buy consensus rating based on nine Buys and four Holds assigned in the last three months. At $156.85, the average Digital Realty Trust price target implies upside potential of 22.52%.

Final Thoughts: REITs Perform Well in Rising Rate Environments

Despite the knee-jerk reaction many investors have with REITs when interest rates are rising, history shows that they perform well in rising-rate environments. As with most REITs, the two mentioned in this piece are also strong dividend plays with a dividend yield of 2.23% for Prologis and a dividend yield of 3.74% for Digital Realty.

Clearly, there is much to like about both companies, although for investors who have to pick just one, Prologis may be slightly better due to its solar exposure, a unique revenue stream that sets it apart. The company doesn’t even pay to install the solar panels, but charges rent to those that install solar panels on its roofs.