For the first time ever, investment firm RBC Capital released its Small-Cap Growth Idea list, made up of stocks with market caps below $5 billion at the time of publishing, and average daily trading volumes of $10 million. Each name scored one of the coveted spots on the list because the firm’s analysts believe it has “either an attractive normalized growth story or strong durable growth characteristics.”

After using TipRanks’ database to get the lowdown on RBC’s top picks, we were able to pinpoint two stocks that have earned support from other analysts as well, enough so to be given a “Strong Buy” consensus rating. Not to mention both names could see substantial gains in the twelve months ahead. Here’s the full scoop.

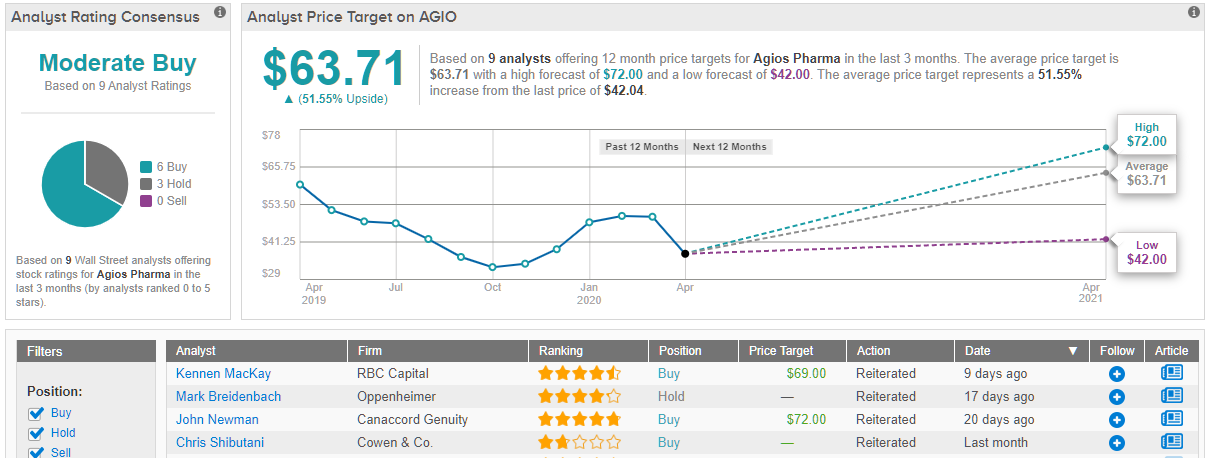

Agios Pharmaceuticals (AGIO)

Leveraging its expertise in cellular metabolism and precision medicine, Agios has developed an impressive product pipeline that includes therapies to target cancer and other rare genetic diseases. So far, April has been kind to this healthcare name, with it up 18% since the first of the month. RBC’s take? More gains are on the horizon.

Weighing in on AGIO for RBC, 5-star analyst Kennen MacKay argues that while somewhat “controversial,” the company’s pyruvate kinase deficiency (PKD) program could be the key to its success. Currently, there aren’t any available treatment options for PKD, which is a rare and severe hemolytic anemia. MacKay doesn’t dispute that AGIO’s mitapivat (AG-348) therapy is a known aromatase inhibitor, which could cause hormonal imbalances, but he points out that during the Phase 2 study, hormones stayed at relatively normal levels.

MacKay added, “We view completion of enrollment for two Phase 3 trials (ACTIVATE and ACTIVATE-T) positively with topline expected by YE:20 and see a high 70% probability of success given limited alternatives for these patients. The Phase 3 responses to mitapivat could be superior to Phase 2 response rates as the Phase 3 study excludes patients with 2 non-missense mutations in PKD. We see the potential for de-risking of mitapivat in other hemolytic anemias such as sickle cell disease and thalassemia with mid-2020 updates at the EHA conference.” As a result, peak global PKD sales could reach $880 million in 2020.

If that wasn’t enough, MacKay believes its Tibsovo drug represents a key point of strength for the company. While Tibsovo’s IDH1mut acute myeloid leukemia (AML) market is smaller than its Idhifa drug’s IDH2mut market, the analyst thinks AGIO’s full ownership of Tibsovo makes it the more valuable asset as Idhifa was developed with Celgene.

“We view Tibsovo’s approval in 1L AML ineligible for intensive therapy as positive and combination with Aza in 1L AML as practice-changing. We see use in cholangiocarcinoma helping drive Tibsovo value beyond AML,” MacKay commented.

With several other possible catalysts fast approaching, it’s no wonder MacKay stayed with the bulls. Along with an Outperform rating, the top analyst kept a $69 price target on the stock, implying 73% upside potential. (To watch MacKay’s track record, click here)

In general, the rest of the Street is on the same page. 6 Buys and 2 Hold ratings received in the last three months add up to a Strong Buy consensus rating. At $63.71, the average price target suggests 52% upside potential. (See Agios stock analysis on TipRanks)

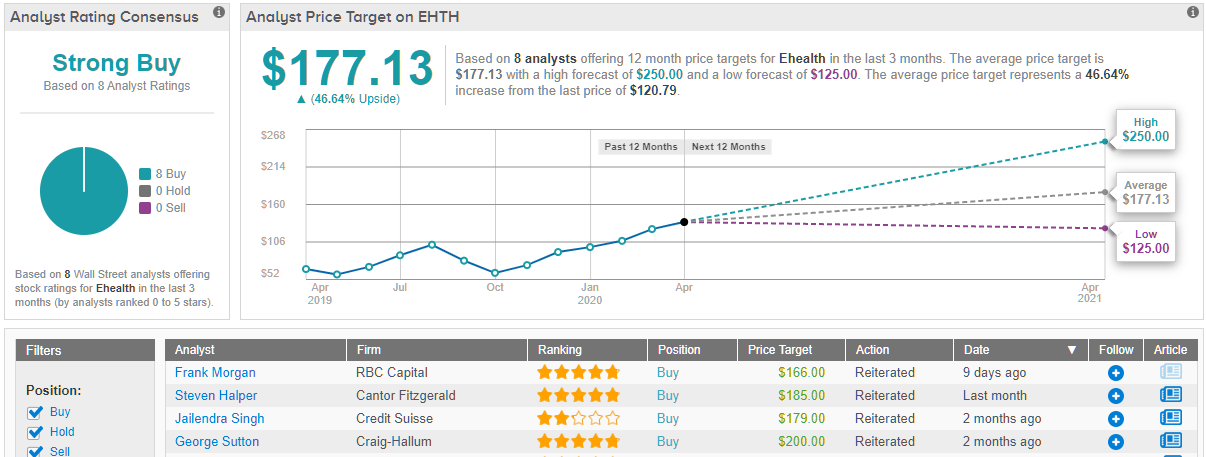

eHealth, Inc. (EHTH)

Switching gears now, eHealth is the largest private health insurance marketplace in the U.S. According to RBC, the stock, which is already up 26% year-to-date, could see its share price grow even more as it’s the only name in the firm’s coverage universe that should escape COVID-19’s impact.

5-star analyst Frank Morgan believes that because people will continue to reach age 65, EHTH’s addressable market stands to grow. He added, “As these newly-Medicare eligible continue to choose Medicare Advantage over traditional FFS Medicare, eHealth’s growth potential should accelerate. And importantly, as a multi-carrier Medicare Advantage broker, eHealth has no medical underwriting risk.”

Every day, almost 10,000 senior citizens age into the Medicare program, with Medicare Advantage penetration slated to increase from 33% currently to about 50% at some point. As a result, Morgan thinks the opportunity for EHTH will expand and rapid changes in plan design and increasing complexity will make its tools more valuable to customers. Additionally, the company’s product enables complete transparency, which could help it compete with other insurance carriers, healthcare.gov and third-party aggregators/call centers.

“In addition to opportunities for further membership growth, we believe eHealth is positioned to drive further improvement in per-member economics, including increased lifetime value through better retention, reduced marketing costs through increased use of direct marketing channels vs. third-party lead generation, and lower customer care costs through increased usage of online enrollment vs. its traditional call center approach,” Morgan stated.

Even though EHTH has to predict the life time value (LTV) of its commission revenue streams earned from Medicare Advantage and other carriers, Morgan calls its expectations “conservative”. To this end, the analyst tells investors he remains optimistic, maintaining an Outperform call and $166 price target. This target brings the upside potential to 44%. (To watch Morgan’s track record, click here)

Similarly, other analysts have high hopes when it comes to EHTH’s long-term growth prospects. With 100% Street support, or 8 Buy ratings to be exact, the message is clear: EHTH is a Strong Buy. Should the $177.13 average price target be met, shares could be in for a 47% twelve-month gain. (See eHealth stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.