With January about to conclude, we’ve come off last year’s bearish trend, and seen solid gains over the first month of the year – 6% on the S&P 500, 11% on the tech-oriented NASDAQ – but that doesn’t mean we’re out of the woods. Inflation remains high, the Fed is still raising interest rates, and there’s still plenty of uncertainty about the course of the Russian war in Ukraine, and what China will do as it moves away from COVID lockdowns.

So what to do, to find the right stocks for gains? The market headwinds, and sheer volume of data naturally generated by the actions of thousands of traders investing in thousands of equities, has created an information dump that’s just too big to fully understand. The best professional analysts tend to focus on a single sector and develop an expertise – and that takes years. The retail investor hasn’t got that kind of time to spare.

But we live in the digital age, and information technology can encompass what the human mind cannot. TipRanks’ Smart Score algorithm fills this need, for data collection and collation, and goes another step further – it rates every stock by 8 factors known to correlate with future outperformance, and then distills those ratings into a single score, based on the familiar scale of 1 to 10, so that investors can see at a glance the main chance for any equity.

Using the Smart Score tool, we’ve looked up two stocks that show the Perfect 10 score. They make an interesting pair to examine; both feature Strong Buy consensus ratings and show how a stock can earn a perfect 10 Smart Score without perfect scores on every factor. Here are the details, and commentary from the Street’s analysts.

Leonardo DRS (DRS)

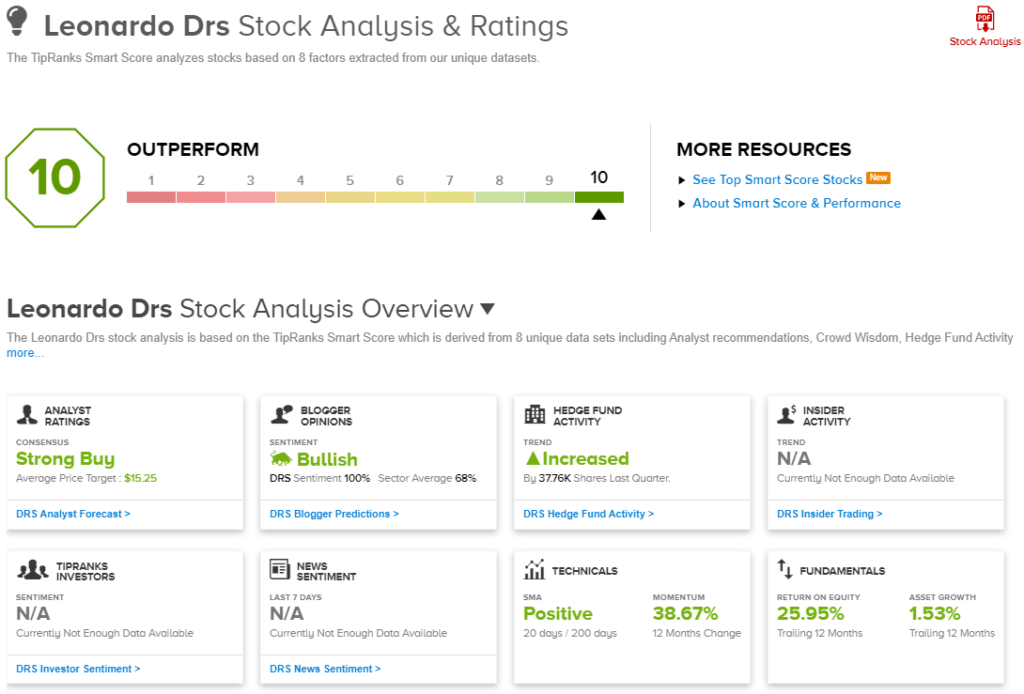

The first ‘Perfect 10’ stock we’re looking at is Leonardo DRS, a company with a 50-year history of success in the defense industry. Leonardo has important contracts with US Army, with a recent $579 million contract win to provide advanced thermal weapon sights and another contract for $39.5 million to provide forward-looking infrared sighting systems, and with the US Navy, for which it is providing propulsion equipment for the new Columbia-class submarines. Other ongoing projects include the Navy’s 76-millimeter shipboard gun, air combat training systems for the Air Force, and target acquisition equipment for the Army’s Apache helicopters.

Leonardo DRS is a subsidiary of an Italian firm, Leonardo S.p.A., which acquired the military contractor DRS in 2008. Last year, the company entered into an all-stock merger agreement with RADA Electronic Industries, another defense contractor firm, under which the two companies formed a combined entity to trade as DRS on the NASDAQ exchange. The merger was closed this past November, with RADA shareholders owning 19.5% of the combined company and Leonardo’s parent company owning the remaining 80.5%.

The combined firm will report its first quarterly results in the next few weeks. We should note that for 2021, the last full year before the merger, Leonardo DRS and RADA had combined full-year revenues of $2.7 billion.

On this defense contractor’s Smart Score, most of the factors are positive. Hedge fund holdings increased modestly, and the bloggers were 100% positive on the stock. The technical factors show a 39% positive momentum for the 12-month period, and the trailing 12-month return on equity, a fundamental factor, is nearly 26%. It adds up to a Perfect 10 for the stock.

This stock has caught the attention of Baird analyst Peter Arment, who writes of it, “Investors are likely taking a ‘wait-and-see’ approach over the next few quarters to assess the business model, organic growth outlook, as well as margin expansion and FCF prospects…. DRS is trading at a deep discount relative to peers on both an EV/EBITDA and FCF yield basis. We believe the discount should narrow over time, assuming DRS is able to execute on key programs and management effectively allocate capital towards niche M&A. The lack of institutional investor base should be resolved if the Italian parent company, Leonardo S.p.A decides to partially monetize their ownership stake which will allow the public free float and liquidity to improve.”

Arment, who holds a 5-star rating from TipRanks, gives DRS shares an Outperform rating, with a $19 price target implying a 41% upside on the one-year horizon. (To watch Arment’s track record, click here)

With 3 recent positive analyst reviews on file, DRS shares have a unanimous Strong Buy consensus rating. The stock is trading for $13.48 and has an average price target of $15.24, a combination that gives a 13% potential upside from current levels. (See DRS stock analysis on TipRanks)

Ovintiv Inc. (OVV)

Next up is an energy stock, Ovintiv. This company operates in the oil and gas exploration and production sphere, where it has principal assets in the Permian and Anadarko basins of Texas and Oklahoma, major oil and gas plays in some of North America’s richest hydrocarbon regions, and in the Montney formation of the Alberta-British Columbia border area. In addition, the company has smaller assets in the Bakken and Uinta plays of Montana and Utah. Ovintiv focuses its operations on generating high-return liquids production, both oil and gas, and producing solid free cash flow to provide a return to shareholders.

Ovintiv will release its 2022 full year results at the end of February, but in the last quarterly report, 3Q22, the company raised its 2022 production guidance to the range of 505 MBOE/d to 515 MBOE/d, an increase of 5,000 barrels per day. Production in Q3 came in at 516 MBOE/d, at the high end of the quarterly guidance.

On the financial side, Ovintiv saw Q3 net earnings of $1.19 billion, up from a $72 million net loss in 3Q21. The company had a non-GAAP free cash flow of $437 million, and returned $387 million to shareholders through a combination of buybacks and dividend payments.

Turning to the Smart Score, we find that Ovintiv has benefited from strongly bullish sentiment from the financial bloggers, along with a 71% return on equity over the trailing 12-month period. But a major boost came from the hedge funds tracked by TipRanks, which last quarter increased their holdings of OVV by 4.2 million shares. These positives outweigh other factors that showed negative results; a Perfect 10 Smart Score does not require every factor to register strongly positive.

in his assessment of Ovintiv, Mizuho’s 5-star analyst Nitin Kumar lays to rest some investor concerns. He writes, “Although the company began its cash return program earlier than expected in 2022, missed earnings and raised capital guidance have led many investors to question inventory depth, strategic commitment and execution track-record. We believe the company is better positioned to maintain FCF generation despite backwardated commodity prices in 2023 than peers, which coupled with an increase in cash returns could provide tailwinds to the stock.”

Along with a Buy rating, Kumar puts a $68 price target on the stock, suggesting an upside of 32% for the next 12 months. (To watch Kumar’s track record, click here)

This oil and gas player has picked up 11 recent analyst reviews, with a breakdown of 9 Buys and 2 Holds for a Strong Buy consensus rating. The stock is selling for $51.32, and its average price target of $65 implies a 27% one-year gain. (See Ovintiv stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.