We are yet to find out what lies in store for the stock market in 2023. However, we do know that the previous year was one of the worst ever, with the S&P 500 putting in its 7th most abject annual performance since 1929.

Whichever way you look at it, then, most investors did not enjoy the past 12 months’ market action. One positive takeaway, however, is that the overall bearish trend has driven share prices down across the board and that has left some stocks at levels that are now just too cheap to ignore.

That is certainly the view of the analysts at JPMorgan. The banking titan’s analysts have pinpointed an opportunity in two names whose valuations have contracted significantly in recent times – undeservedly so, they believe. Does the rest of the Street agree they are going for cheap? Let’s take a closer look.

Palomar Holdings (PLMR)

We’ll start with Palomar Holdings, an insurance company with a difference. Instead of focusing on traditional insurance coverage, Palomar targets what it terms ‘underserved’ markets, such as earthquake, flood and hurricane insurance. The company offers its clients a range of versatile products and tailored pricing plans using its data analytics and cutting-edge technology platform.

2022 was panning out rather well for the specialty insurance company’s stock, but then Palomar released its Q3 earnings report, and it was not what investors wanted to see.

While revenue climbed 17.2% year-over-year to of $79.3 million, that figure missed the consensus estimate by a significant $14.18 million. Likewise, on the bottom-line, the analysts were expecting adj. EPS of $0.52, but that figure came in at $0.23. The consequence of these soft metrics was a downward spiral for the shares; the stock is now down by 47% from last year’s October highs.

While cognizant of the soft quarterly performance and mindful of the “headwinds that will likely pressure PLMR’s results through 2023,” JPM’s Jimmy Bhullar thinks the stock’s sell-off “seems too steep.”

“We think that the current stock price ignores near-term improvements in business trends that are already materializing (PLMR has signaled a recovery in premium growth in binary lines after a softer 3Q22) and the various steps PLMR is taking to offset the impact of higher reinsurance pricing (albeit with a delayed impact),” the analyst went on to say. “Furthermore, we believe that the above-average growth profile of PLMR remains intact given opportunities in its core earthquake market and in new lines. At its current stock price, PLMR is trading in line with large commercial peers on 2024 earnings already reduced for the above factors without receiving any valuation benefit for its superior margin or growth profile in subsequent years.”

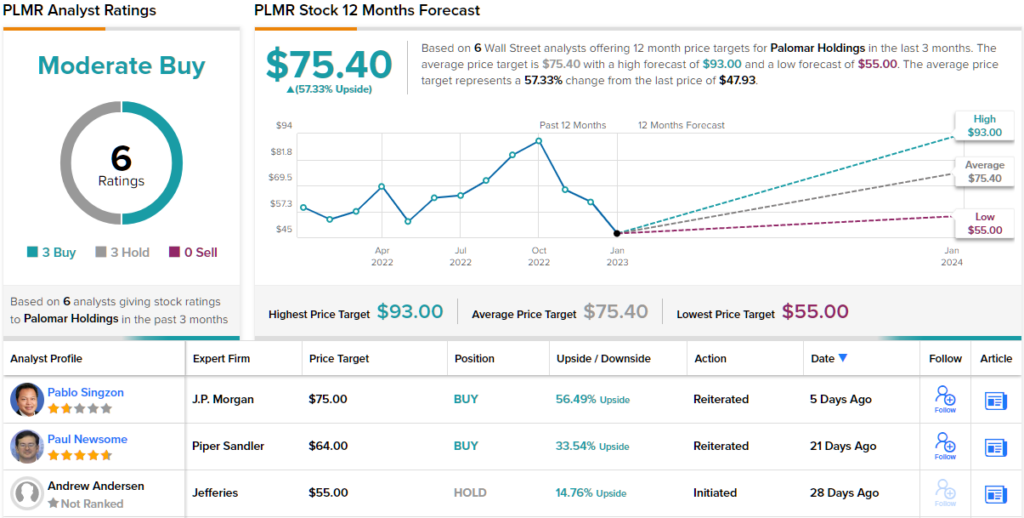

Accordingly, Bhullar rates PLMR shares an Overweight (i.e. Buy) while his $75 price target makes room for 12-month upside of ~56%. (To watch Bhullar’s track record, click here)

The Street’s average target is almost the same; at $75.40, the expectation is that the stock will generate returns of 57% over the coming year. All in all, based on an 3 Buys and Holds, each, the stock claims a Moderate Buy consensus rating. (See PLMR stock forecast on TipRanks)

TransUnion (TRU)

Next up on our list of JPMorgan cheap stocks is TransUnion, a US credit reporting agency. Alongside Experian and Equifax, the company is considered one of the top three credit agencies. Providing services to more than 65,000 clients in over 30 countries, TransUnion gathers and combines data on more than a billion individual consumers, 200 million of which reside in the U.S. Consumer credit reports, risk ratings, analytical services to mitigate risk, and decisioning capabilities to supply information across the consumer credit lifecycle are among the goods and services offered by the company.

In the latest quarterly report – for 3Q22 – revenue increased by 26.2% year-over-year to $938 million, yet that figure fell $7.58 million shy of the analysts’ forecast. However, delivering adj. EPS of $0.93, the company managed to trump the $0.91 consensus estimate. For the fourth quarter, the company expects revenue in the range between $896 million to $916 million, compared to Street expectations for $940.71 million. Adj. EPS is anticipated to be in the $0.80-$0.86 range. Consensus had $0.91.

That, however, was not the reason behind the stock’s lackluster performance in 2022, during which the shares shed 52% of their value. Generally speaking, the backdrop of a softening consumer environment amidst interest rates pushing higher is not great news for credit reporting agencies. But JPMorgan’s Andrew Steinerman credits investors doubts around the acquisition of identity resolution company Neustar (closed December 2021) as the main factor behind the shares’ decline.

Calling TRU his “favorite 2023 idea within Information Services,” the analyst lays out the bull-case for the expanded company.

“We believe that the TRU stock is too cheap to ignore and that its Neustar acquisition will enhance the company’s anti-fraud and digital marketing capabilities in the years ahead,” Steinerman said. “We view Neustar as complementary to TRU’s data analytics portfolio and think Neustar is enhancing TRU’s anti-fraud and digital marketing capabilities. In 2022, TRU had been integrating its data assets onto Neustar’s OneID platform, and in 2023, TRU plans to integrate OneID into the company’s solutions to develop new joint products. We recognize that the first year of integration has encountered some bumps along the road, but we believe TRU will achieve its targets for Neustar to enhance TransUnion’s organic revenue growth and margins.”

All told, Steinerman rates TRU shares an Overweight (i.e. Buy), backed by a $76 price target. The implication for investors? Upside of ~19% from current levels. (To watch Steinerman’s track record, click here)

Looking at the consensus breakdown, based on 8 Buys vs. 7 Holds, the analysts’ view is that this stock is a Moderate Buy. Going by the $72.89 average target, the shares will climb ~14% higher in the year ahead. (See TransUnion stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.