Airlines witnessed strong traffic following the reopening of the economy and easing of restrictions, thanks to pent-up travel demand. However, rise in fuel costs and severe staffing shortages impacted the pace of recovery. Staffing issues have caused massive cancellations, delays, and capacity cuts over recent months. While airlines have hiked fares to capitalize on the strong travel demand, elevated fuel costs and higher wages are expected to be drag on near-term earnings. With major airlines set to announce their third-quarter results soon, we will discuss here the prospects of three stocks – United Airlines (NASDAQ:UAL), Delta Air Lines (NYSE:DAL), and American Airlines (NASDAQ:AAL). Using TipRanks’ Stock Comparison Tool, let’s pick the airline stock that Wall Street favors the most.

United Airlines (UAL) Stock

After being crushed by COVID-related travel disruptions, United Airlines returned to profitability in the second quarter of 2022. Revenue grew 6.2% to $12.1 billion compared to 2019 levels and helped the company post adjusted earnings per share (EPS) of $1.43. However, Q2 earnings were still below the comparable period of 2019 and also lagged analysts’ expectations by a big margin.

Last month, much to the delight of investors, United slightly raised its Q3 estimates, citing continued strong demand following a robust summer and better-than-anticipated capacity trends. The carrier expects its operating revenue to grow 12% compared to 2019 levels, up from its previous estimate of 11%. Also, it anticipates adjusted operating margin to come in at 10.5% in Q3, compared to the prior forecast of 10%.

Is UAL a Good Stock to Buy?

Ahead of the Q3 earnings season, Raymond James analyst Savanthi Syth revised her forecasts to reflect lower estimates for fuel price, solid demand, increased pilot costs, the effect of Hurricane Ian, and some easing of capacity constraints.

Syth feels that the rebound in the travel demand from large companies and the Northeast region, as well as the gradual reopening of long-haul international routes puts United and Delta in “relatively stronger position” when it comes to top line recovery compared to their peers. Syth reiterated a Buy rating and a price target of $48 for UAL stock.

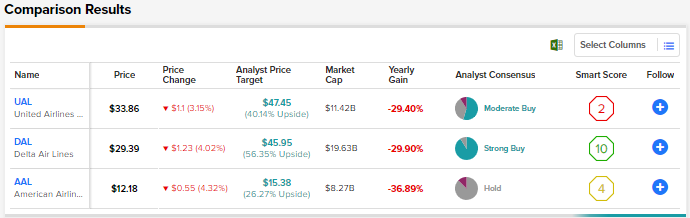

All in all, United scores a Moderate Buy consensus rating based on six Buys, four Holds, and one Sell. The average United Airlines stock price target of $47.45 implies 40.1% upside potential from current levels.

Delta Air Lines (DAL)

Strong demand fueled Q2 revenue growth of 10% to $13.8 billion for Delta. While the top line exceeded expectations, the company’s adjusted EPS of $1.44 significantly lagged the Street’s consensus estimate and was 39% below 2019 levels. The Q2 bottom line was hit by staff-related operational disruptions and increased costs.

Delta expects its Q3 revenue growth in the range of 1% to 5% compared to pre-pandemic levels, although it guided for a capacity that is 15% to 17% below 2019 levels. Moreover, the company reassured investors that it expects “meaningful profitability in 2022.”

Is Delta a Good Investment?

We previously mentioned Raymond James analyst Syth’s optimism about Delta. The analyst highlighted Delta’s key strengths relative to its rivals, including comparatively lower debt levels, lack of a massive aircraft order book, and its solid track record of capital deployment. In line with her investment thesis, Syth raised the price target for Delta stock to $52 from $50 and maintained a Buy rating.

Overall, the Street’s Strong Buy rating for Delta Airlines stock is based on 10 Buys and one Hold. The average DAL stock price target of $45.95 implies 56.4% upside potential.

American Airlines (AAL)

American Airlines is currently in the news due to an antitrust trial, alleging that the carrier’s Northeast alliance with JetBlue hinders competition and allows them to charge higher prices.

Meanwhile, back in July, the company stated that it expects to continue to be profitable in the third quarter, driven by revenue growth in the range of 10% to 12% compared to 2019 levels. American Airlines guided for higher Q3 revenue despite lower capacity, thus reflecting the impact of increased fares. The company’s Q2 revenue increased 12.2% (compared to Q2 2019) to $13.4 billion and was ahead of expectations. Meanwhile, Q2 adjusted EPS of $0.76 was in line with expectations, and marked the carrier’s return to profitability.

Is American Airlines a Buy or Sell?

Bank of America analyst Andrew Didora trimmed his price target for AAL stock to $7 from $8 and reiterated a Sell rating as part of his Q3 earnings preview for the airlines sector.

Earlier this week, Bank of America had highlighted its top ten ideas for the fourth quarter, which included nine Buys across various sectors and one Sell recommendation for American Airlines stock. As per the investment bank, American Airlines’ profitability is under pressure due to rising interest rates. Moreover, the analyst noted that AAL stock trades at a 34% premium to the airlines group and a 26% premium to rivals United and Delta, which exposes it to earnings multiple risk.

All in all, Wall Street is sidelined on American Airlines stock with seven Holds and one Sell. At $15.38, the average AAL stock price prediction implies 26.3% upside potential from current levels.

Conclusion

Airlines are already under pressure due to staffing challenges and high fuel costs. A potential recession might impact the recovery in travel demand and airlines’ ability to bring down debt, which mounted due to the pandemic. For now, Q3 outlook reflects strong demand and higher fares. Currently, Wall Street analysts are very bullish on Delta Air Lines and also project a higher upside in DAL stock compared to United Airlines and American Airlines.

At the Morgan Stanley 10th Annual Laguna Conference held in September, Delta sounded optimistic about achieving its 2024 target of more than $7 of EPS, mid-teen margins, mid-teens return on capital.

As per TipRanks Smart Score System, Delta scores a “Perfect 10”, implying the stock could outperform the market averages over the long term.