Shoppers everywhere like to find the best value; that’s a given. And investors? Well, investors are just a special case of shoppers – in this case, shopping for stocks. So, how can we define a good value when it comes to stocks? In short, we’re looking for high upside and high dividend yields.

TipRanks, a platform that tracks and measures the performance of analysts, offers a set of tools to search the raw data collected from 5,700 Wall Street financial experts and 6,500 publicly traded companies. The basic tool, the Stock Screener, gives investors a set of filters to screen the data and find the stocks that fit the desired profile.

Setting the filters to show us stocks with a price target upside above 10% and a dividend yield above 2.5% brings the list down to a manageable 46 companies – that will offer investors a true value for their stock purchase. Let’s look at three of them that have a top spot in the S&P 500.

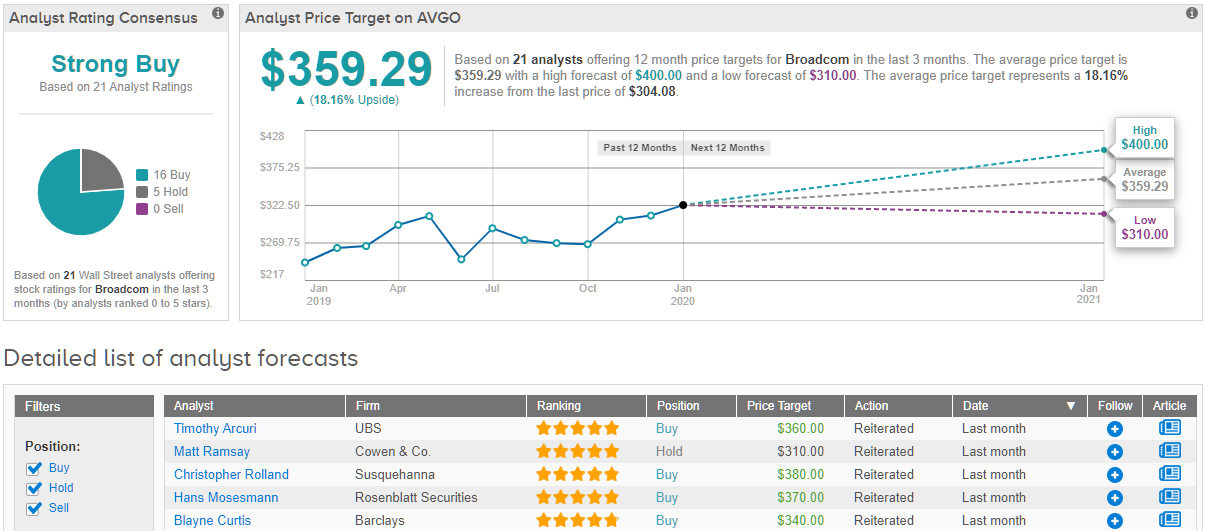

Broadcom, Inc. (AVGO)

We’ll start with Broadcom, a stand-by of the semiconductor chip industry. Broadcom’s 2019 sales numbers are not in yet, but it finished 2018 as the sixth largest chip maker by revenues, bringing in $18.46 billion. Riding high from that sales figure, Broadcom stock gained 28% in 2019, matching the broader stock market figures.

In December’s fiscal Q4 earnings report, AVGO showed revenue and earnings both above the forecasts. The top-line sales figure was $5.78 billion, up 6.25% year-over-year and up 5% sequentially from Q3. Earnings showed a less impressive gain, but the annual EPS of $5.39 beat the expectation by a half-percent.

AVGO shares are well positioned for price appreciation; they are also one of the market’s true dividend champions. The company raised the December dividend payment, to $3.25 per quarter, making the annual payment $13 and the yield 4.34%. That yield is well above the 2% average among S&P-listed companies, and the December increase caps a three-year run of consistent dividend increases.

Top analysts see AVGO as a healthy investment. Writing from Morgan Stanley, 5-star analyst Craig Hettenbach says, “We think the stock is poised to outperform after meaningfully lagging the past 2 years… If Broadcom is able to execute in software it would add to what we view as a very compelling franchise in semis (66% weighted market share across 60% of revenue in duopoly structures), creating a diversified and highly profitable and cash generative business.”

Hettenbach accordingly rates the stock a Buy, and puts a price target of $367 on the shares, indicating an upside potential of 23%. (To watch Hettenbach’s track record, click here)

Mark Lipacis, the eighth-ranked analyst overall in the TipRanks database, agrees that AVGO is poised for gains. Noting that the “company’s dividend policy is to return 50% of previous year’s FCF to shareholders in the form of a dividend,” he goes on to add, “AVGO expects 6-8% growth in Core Semiconductor business over the next few years. Software business is becoming more predictable and expected to be $7bn in F2020.”

In line with his optimism and Buy rating, Lipacis bumped his price target here up by 8%, to $350, implying a 17%. (To watch Lipacis’ track record, click here)

Broadcom’s Strong Buy consensus rating is based on 21 analyst reviews, including 16 Buys and 5 Holds. Shares are not cheap, at $299.22, but the average price target suggests room for a 18% upside growth potential this year. (See Broadcom stock analysis at TipRanks)

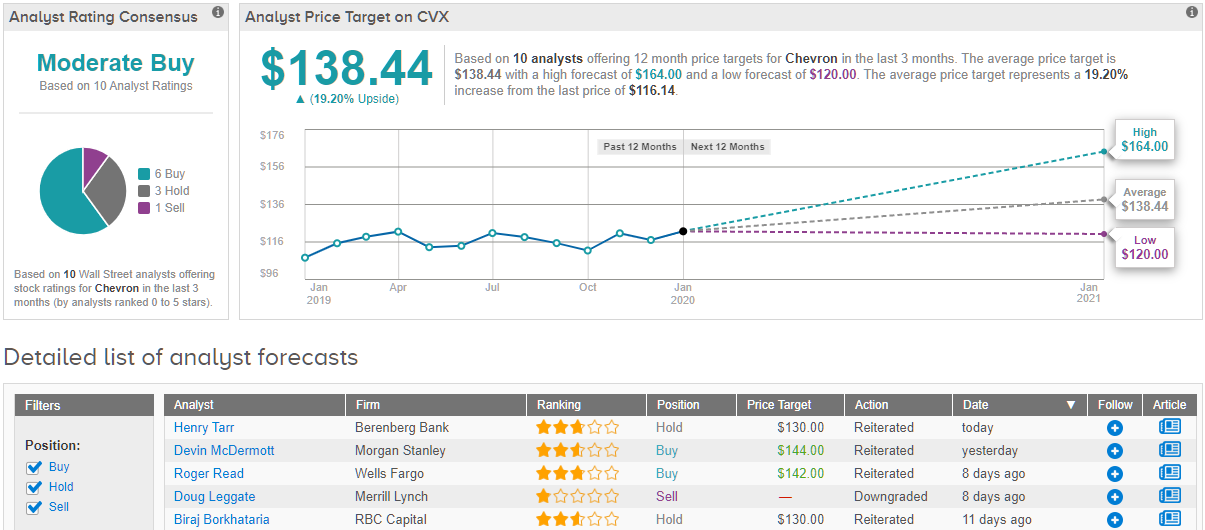

Chevron Corporation (CVX)

Chevron, one of the world’s largest oil producers, with a market cap of $220 billion, is facing rough market conditions. Prices in the oil markets are low – 2H19 saw market bottoms near $52 for WTI – while overhead costs remain high. The combination pushed revenue down from ~$14 billion in 2018 to ~$12 billion in 2019.

In CVX’s most recent earnings report, for Q3 2019, the company showed a 6% miss on EPS, with the bottom-line number at $1.36 for the quarter. Revenues were down by 4%, at $36.12 billion. During the quarter, the price of crude oil and natural gas liquids fell 24%, from $62 one year ago to $47 per barrel equivalent. A 3% increase in total production helped mitigate the losses.

Even though revenues and EPS are down, CVX has been able to maintain its high dividend payout. Oil is an essential commodity, so there will always be a market for it, and cash flow for the oil companies. CVX uses those facts to back up a 4.09% dividend yield, with an annualized payment of $4.76. This yield is approximately double the S&P’s average dividend yield, and well over double the yield of the 2-year and 10-year US Treasury bonds.

Piper Sandler analyst Ryan Todd sees the bottom line on CVX supporting a Buy rating. He writes, “Despite the well-telegraphed headwinds, we continue to see CVX’s peer-leading portfolio breakeven and attractive FCF outlook as supporting leading growth in dividends/shareholder returns amongst its peers.”

Todd’s $143 price target on CVX shares implies room for a 23% upside. (To watch Todd’s track record, click here.)

Roger Read, reviewing CVX for Well Fargo, lays out an upbeat track for the company in 2020: “Driven by its unconventional plays, deepwater assets and LNG projects, [we see CVX bringing in] modest, returns-focused production growth expectations, expanding margins from high-grading and cost controls, dividend growth, potential share repurchases and solid balance sheet.”

Read gives CVX a Buy rating with a $142 price target, showing his confidence in 22% forward growth. (To watch Read’s track record, click here)

The difficulties of the oil market can be seen in Chevron’s analyst consensus, a Moderate Buy rating based on 6 Buys, 3 Holds, and 1 Sell. The average price target of $137 implies an upside of 18% from the $116 current trading price. (See Chevron’s stock analysis at TipRanks)

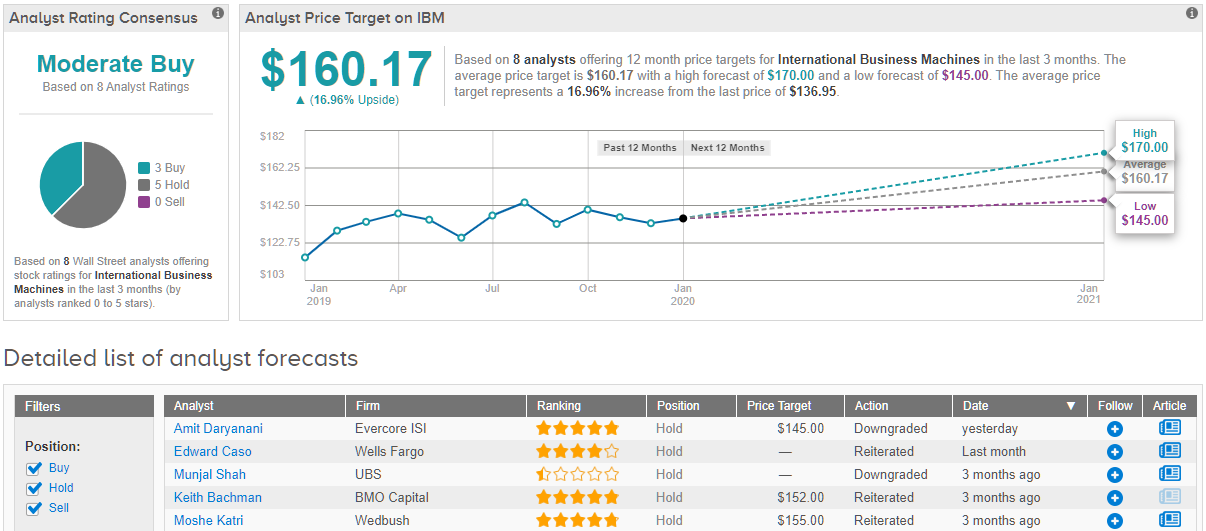

International Business Machines (IBM)

The last stock on our list is an old-name blue-chip standard of the markets, and a long-time component of the Dow Jones index, IBM. It’s a name that everyone knows – IBM got its start in business tech when that meant gear-driven mechanical calculators and card-punch time clocks. After WWII, IBM was at the forefront of the electronic computer revolution, evolving from punch card machines to magnetic tape drives to the early floppy disks. The ubiquitous PC got its start with an IBM operating system. Today, business tech is moving toward the cloud, and IBM acquired cloud innovator Red Hat last year, to get a foothold in the cloud market. With a market cap of $121 billion and annual revenues in the neighborhood of $80 billion, IBM has plenty of resources to change direction.

Staying at the top isn’t cheap, though. IBM had to spend $34 billion on the Red Had acquisition, and saw a major bookkeeping loss in its most recent reported quarter, Q3 of 2019. The quarterly revenue hit was heavy – the top line was down $190 million to, to $18.03 billion. On the positive side, Red Hat, in its first quarter as a subsidiary, saw revenues rise 20%, and EPS was in line with the forecasts, at $2.68.

While closing the Red Hat deal, IBM management announced that it would freeze the dividend at current levels for at least the next year. While this forestalls growth, the actual payment remains high – $1.62 per quarter. Annually, this translates to $6.48 and a yield of 4.74%. IBM has, since 2011, committed to maintaining the dividend payment, as a boon to investors.

Matthew Cabral, 4-star analyst with Credit Suisse, is upbeat on IBM. He notes the “solid start” of Red Hat as part of the IBM parent company, and then adds, “[W]e think that inflection starts in 4Q, with an early boost from mainframe before passing the baton to Red Hat and the related pull-through of “core” IBM in CY20. Indeed, early progress on Red Hat is encouraging and we continue to believe the acquisition significantly improves IBM’s standing in the rapid push toward hybrid cloud.”

Cabral backs his outlook with a Buy rating and a $173 price target. His target suggests room for 26% share appreciation in 2020. (To watch Cabral’s track record, click here)

IBM’s Moderate Buy consensus rating reflects the company’s recent mixed results on revenues, and debt from the Red Hat purchase. The stock has an even split – 4 Buy ratings and 4 Holds. Shares sell for $136, and the average price target of $162.67 implies an upside potential of 19%. (See IBM stock analysis at TipRanks)